Magellan Global Trust

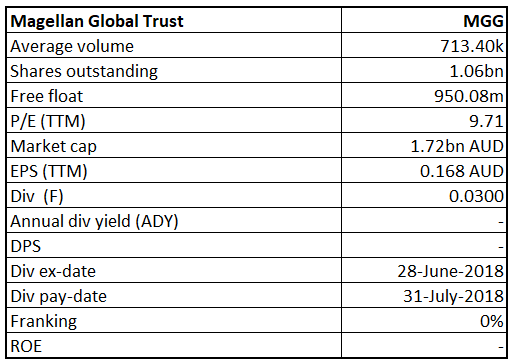

MGG Details

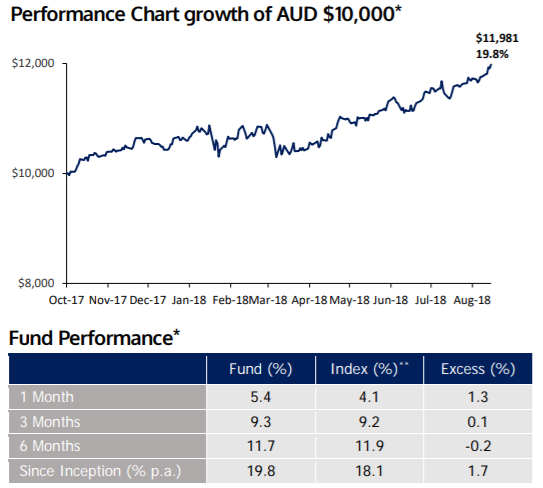

Decent Investment Return Since Inception: Magellan Global Trust (ASX: MGG) is a small-to mid-cap well diversified financial company with the market capitalization of circa $1.72 Bn as of October 12, 2018. Recently, the group disclosed its weekly NAV per unit of Magellan Global Trust and recorded the same at $1.7301 as at October 05, 2018, a decrease of 0.1% in NAV from $1.7316 as on September 28, 2018. Further, MGG reported a strong performance for August month wherein MGG Investment Portfolio delivered a 5.4% return in one month (as of 31 August 2018) as compared to MSCI World Net Total Return Index (AUD) returns of 4.1%, exhibiting growth of 1.3%. For three months’ performance, MGG Investment Portfolio delivered decent returns of 9.3% (as at 31 August 2018) against the benchmark of 9.2%. Since inception, MGG Investment Portfolio generated 19.8% returns per annum against the MSCI World Net Total Return Index returns of 18.1% p.a. As 31 August 2018, the fund size was A$1,827.4 million, displaying 5.6% growth as compared to July month wherein fund size was A$1,730.6 Mn. Further, the company has well diversified portfolio comprising Consumer Defensive (17%), Health Care (8%), Internet & eCommerce (18%), Information Technology (14%), Consumer Discretionary (5%), Payments (9%), Financials (5%), Infrastructure (3%), and Cash (20%) units. Cash is held predominantly in USD as at 31 August 2018.

Moreover, the primary objectives of MGG are to achieve attractive risk-adjusted returns over the medium to long-term, while reducing the risk of permanent capital loss. The company may also manage its foreign currency exposure arising from investments in overseas markets. Hence, we expect that the trust has the potential to grow further at the back of its strategic investment approach in its well-diversified portfolio.

Fund Performance (Source: Company Reports)

Meanwhile, the share price has risen 9.73 % in the past six months as at October 11, 2018 and traded at reasonable PE level of 9.710x. Based on foregoing, we maintain our “Buy” recommendation on the stock at the current market price of $1.645.

Propel Funeral Partners Limited

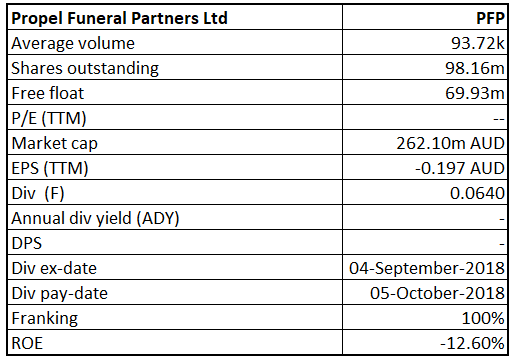

PFP Details

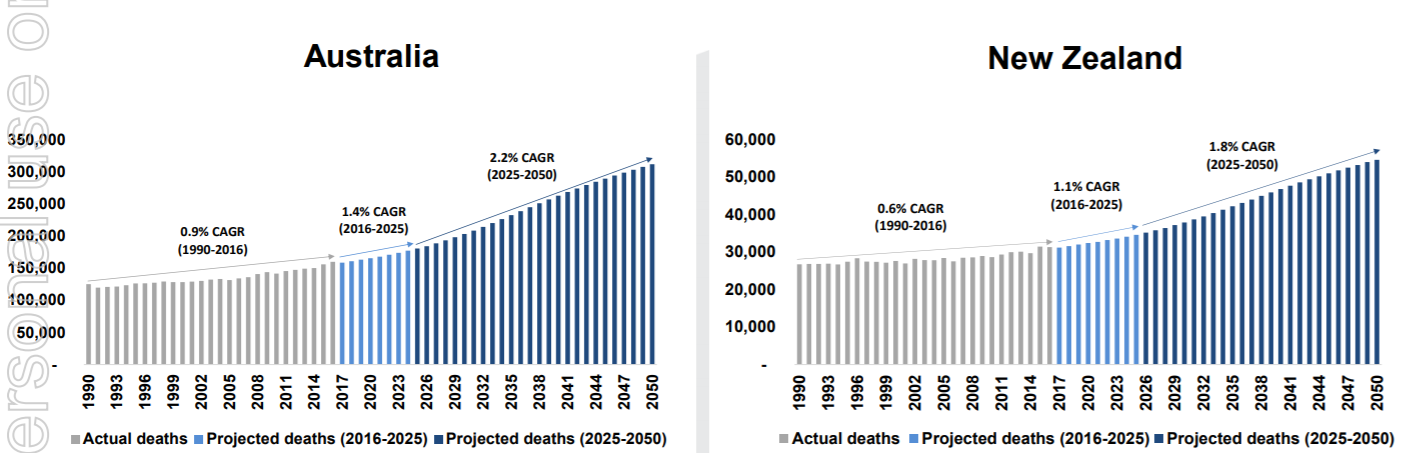

Growth Story To be Continued: Propel Funeral Partners Limited (ASX: PFP) is involved in the operations of providing death care related services in New Zealand and Australia. The company delivered a solid financial performance in FY 2018. Due to the full period impact of six acquisitions completed in FY 2017 and part period impact of Seasons Funerals, Brindley Group and Norwood Park acquisitions in FY 2018, the total revenue of the company substantially increased by 76 percent to $80.9 million in FY 2018 as compared to last year. Due to increased revenue, the operating EBITDA of the company also increased by 75% to $21.5 million. The basic earnings per share of the company increased from 5.6 cents in FY 2017 to 12.7 cents in FY 2018. On CAGR basis, the death volumes in Australia increased by 0.9% between 1990 and 2016 and these death volumes are expected to increase around 1.4% from 2016 to 2025. The death volumes in New Zealand at CAGR basis also grew by 0.6% from 1990 to 2016 and these volumes are expected to increase by 1.1 percent from 2016 to 2025. Increase in the number of deaths is one of the most significant drivers in the death care industry. The company is also expected to get benefited from the acquisitions which are completed during FY 2018. Moreover, the company has a diversified single and multi-site brands portfolio with strong local community awareness. This includes Ross funerals, Gympie Funerals, Virgo Funerals, WT Howard Funerals, Handley Funerals services, Geards Funeral Home, Davis Funerals, etc. We expect that the company will maintain its strong growth trajectory in future on the back of increasing funerals volumes and strategic acquisitions across the regions.

Increasing Number of Deaths (Source: Company Reports)

Meanwhile, the share price declined by 8.87 percent in the past three months as of October 11, 2018. As of now, the stock traded at 25.5% discount to a 12-month high of $3.68 against a 3% premium to a 12-month low of $2.66. Based on foregoing, we maintain our “Speculative Buy” rating on the stock at the current market price of $2.740 (up 2.6% on October 12, 2018).

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...