CYBG PLC

CYB Details

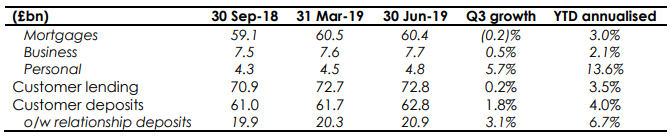

Disclosure of Transactions:CYBG PLC (ASX: CYB) provides banking products and services and has a market capitalisation of A$2.82 Bn as on 11th October 2019. The company, through a release dated 2nd October 2019, announced public disclosure of transactions. It stated that Ian Smith and Fraser Ingram had purchased 129 and 130 shares, respectively, at a price of £1.16 per share on 1st October 2019, under the CYBG PLC Share Incentive Plan. In another update, CYB notified the market participants that the total number of voting rights of the company stood at 1,434,485,689 as of 30th September 2019. It added that the total ordinary shares and CHESS Depositary Interests stood at 538,259,895 and 896,225,794, respectively, as at the close of business on 30th September 2019. The following picture provides an idea of pioneering growth in the company’s key metrics:

Pioneering Growth (Source: Company Reports)

What to Expect: The company continues to progress for its target for around £200 Mn of net cost savings by FY22 and as at Q3, it realised approximately £45 Mn of annual run-rate savings. The company remains on track to deliver FY19 underlying costs of less than £950 Mn. The company anticipates that net interest margin to be at the lower end of the 165-170bps guidance range for FY19.

Stock Recommendation:As per the Q3 FY19 trading update, Common Equity Tier 1 ratio stood at 14.6% and, thus, suggesting bank’s well capitalised position. The company reported a growth of 5.7% to £4.8bn in personal lending, mainly driven by strong growth in credit card. On the valuation front, the price to cash flow multiple of the company stood at 4.0x in comparison to the industry median (Financials) of 8.9x on a TTM basis. CYB is trading at a price to book multiple of 0.3x against industry average (Financials) of 1.8x on a TTM basis. Thus, on valuation front, the stock seems undervalued at the current market price of A$2.150 per share. Considering the attractive valuation, well capitalised structure and other parameters, we give a “Buy” recommendation on the stock at the current market price of A$2.150 per share, up 9.415% on 11th October 2019.

CYB Daily Technical Chart (Source: Thomson Reuters)

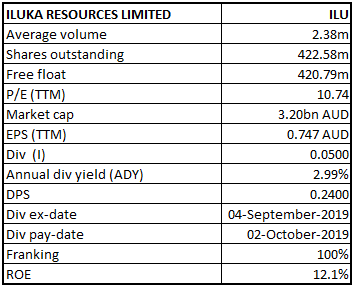

Iluka Resources Limited

ILU Details

Issue of DRP Price:Iluka Resources Limited (ASX: ILU) is involved in exploration, project development, mining operations, processing and the marketing of mineral sands. The market capitalisation of the company stood at A$ 3.2 Bn as on 11th October 2019. The company recently announced that James Hutchison Ranck has made a change to holdings by acquiring 83 ordinary shares at the consideration of $628.58 on 2nd October 2019. Post-change, James Hutchison Ranck holds 12,762 ordinary shares. ILU, through a release, announced that allocation price for the shares to be issued via Dividend Reinvestment Plan (DRP) for 2019 interim dividend is $7.5732.

For 2019 interim dividend, allocation price was calculated as average of the daily volume weighted average price of Iluka Resources Limited shares, on each of 10 consecutive trading days during the span of September 10, 2019 to September 23, 2019.

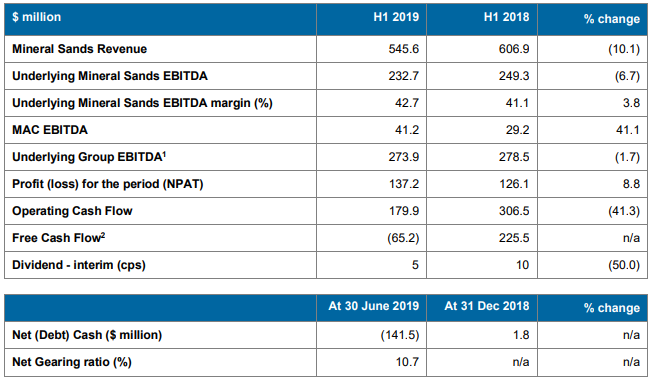

For the half-year ended 30th June 2019, the company reported a profit after tax amounting to $137.2 Mn as compared to $126.1 Mn of 1H FY18. It was stated that the higher profit reflected higher sales prices throughout the product suite, partially offset by lower sales volumes.

Key Financial Metrics (Source: Company Reports)

Future Aspects:The company has stated that depreciation and amortisation are expected to be $155 million from $135 million due to increased depreciation costs post capital improvement works at Sierra Rutile. The company has reduced its guidance for 2019 capital expenditure to $260 million from $330 million, predominantly reflecting the delay of Sembehun early works beyond 2019, and some timing of spend for other projects.The company continues to support customers through its rebating system and a flexible product offering, which would include more Standard Zircon product.

Stock Recommendation:The net margin of the company stood at 22.5% in 1H FY19 as compared to the industry median of 15.9%, which reflects that ILU has better capabilities to convert its top-line into the bottom-line as compared to the broader industry. The return of equity of ILU stood at 12.1% in 1H FY19 against the industry median of 6.2%. This implies that the company is providing decent returns to its shareholders in comparison to the broader industry. The company witnessed a CAGR growth of 14% in total revenue in the time period of FY14 to FY18 and, thus, it can be said that ILU has generated decent revenues during the period. On the valuation front, as per ASX, the stock of ILU is trading at a price to earnings multiple of 10.74x in comparison to the industry average of 11.84x on a TTM basis. The price to cash flow per share multiple stood at 6.69x against the industry median of 6.79x on NTM basis. Hence, considering the above-stated facts and current trading levels, we maintain our “Hold” rating on the stock at the current market price of A$8.020 per share, up 5.805% on 11th October 2019.

ILU Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...