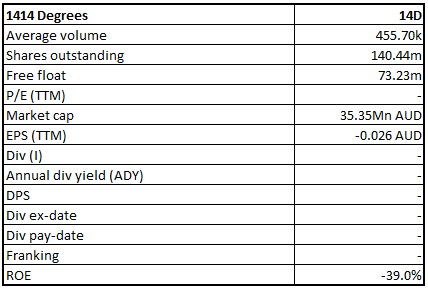

1414 Degrees

14D Details

Acquiring of Aurora Project to Stimulate Revenue Growth:1414 Degrees (ASX: 14D) is engaged in the business of commercialising energy storage technology, thermal energy storage system providing a low-cost solution to intermittent energy supply and recovering electricity through a turbine on demand. The market capitalisation of the company stood at $35.35 million on 5th December 2019.

Business Model (Source: Company Reports)

Acquisition of Aurora Project to Scale Up the Storage Capacity:The company is going to acquire SolarReserve Australia II Pty Ltd, which owns the Aurora Solar Energy Project near Port Augusta in South Australia and two solar sites in New South Wales. The Aurora Project has SA Government’s development approval for a 70 MW of solar PV farm and 150 MW of generation from a concentrated solar thermal plant (CST). The company has planned to use the site to pilot its world leading TESS-GRID technologies.

The company will seek approval from the Government and stakeholders to submit a new development application to provide upto 400 MW solar PV along with the installation of the TESS-GRID technologies. The company could also buy and store electricity generated by other renewable firms with the objective of strengthening firming services and earning from market arbitrage.

The company’s Cash Position Remain Strong: At the end of the quarter, ended on 30th September 2019, the company had a cash balance of $7.7 million, which is expected to be boosted with a substantial R&D rebate in November. The company’s cash balance remains strong mainly because of a decrease in monthly outgoings after the commissioning of the GAS-TESS. Company’s total assets are now more than $17 million.

Key Focus Areas for the Future Growth: As per the company, the global market indicates that there is demand for tens of thousands of GAS-TESS in the near future, to replace the existing engines in Wastewater Treatment Plants. The company expects that GAS-TESS will lead to its first significant revenues for the company.

Stock Recommendation: Over the past five years (FY15 to FY19), the company has registered a CAGR of 39.16% in revenue. As per the ASX, the stock price is trading below the average of 52-week high and low. Company’s price to book value stood at 1.7x on TTM basis, which is below the industry (Industrials) average of 4.9x on a TTM basis. Based on its CAGR growth, strong cash position and current trading levels, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.200, down 2.439% as on 05 December 2019.

14D Daily Technical Chart (Source: Thomson Reuters)

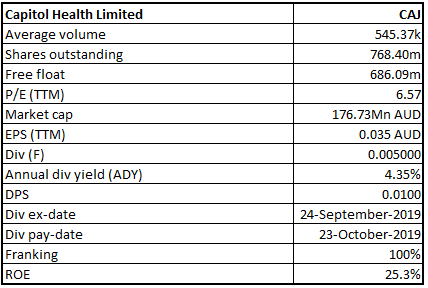

Capitol Health Limited

CAJ Details

Significant Increase in Growth Capex to Drive Sales: Capitol Health Limited (ASX: CAJ) is headquartered in Melbourne and operates clinics throughout Victoria, Tasmania and Western Australia. The company provides diagnostic imaging and related services to the Australian healthcare market. The market capitalisation of the company stood at $176.73 million on 5th December 2019.

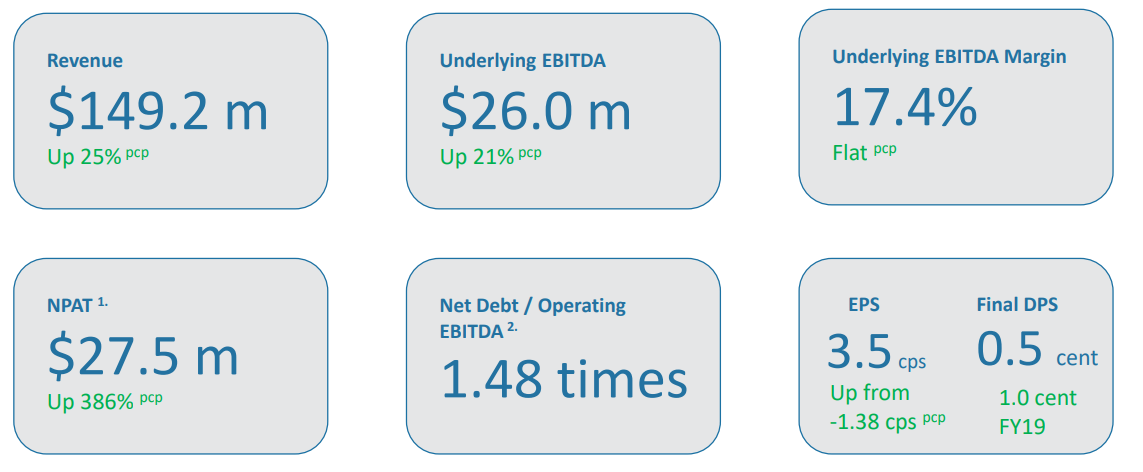

FY19 Result in-line with Guidance: The company’s full-year results were in-line with the guidance provided in February for FY19. CAJ reported revenue of $149.2 million for FY19, up 25% YoY and the company’s underlying EBITDA stood at $26 million, up 21% YoY. There was a slight decline in underlying EBITDA margins on YoY basis, due to an increase in radiologist capacity and subdued demand. During the year, the company generated a free cash flow of $12.4 million, more than 100% on pcp basis. During the year, the company completed the acquisition of 7 clinics, which added 16 clinics and entry into the WA market for Capitol Network.

Financial Summary (Source: Company Reports)

Industry Performance for FY19: In FY19, there was a strong decline in Medicare diagnostic imaging service growth levels from the previous year and were more consistent with the declines seen in 2015-2016 to an average of 3%. The company’s demand is strongly correlated with GP attendance, and more than 80% of the company’s referrals come from GP’s referrals, and more than 75% of services are bulk billed. GP attendance was mainly weak in FY19 and moved down in the second half.

Outlook for FY20: The company will focus on delivering organic growth in underlying EBITDA for FY20.It is ready to deliver stronger growth in FY21 through investment in systems, process and capacity. The Medicare DI indexation, which will be introduced in July 2020, is expected to be CPI for 80% of outlays.

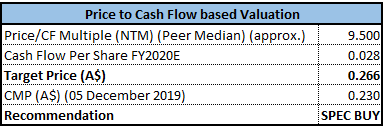

Valuation Methodology: Price to Cash Flow Based Valuation

Price to Cash Flow based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation:The company reported a 7.72% CAGR growth in its revenues over the last five years (FY15 to FY19). Also, the company has improved its EBITDA margins from 13.7% in FY16 to 17.4% in FY19. Looking at consistency in the financial performance of the company and investment projects in pipelines, and other factors, we have valued the stock using Price to Cash Flow multiple approach, which gives an upside of lower double-digit (in percentage terms). We recommend a “Speculative Buy” rating on the stock at the current market price of $0.230 per share on 5th December 2019.

CAJ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...