Rural Funds Group

.png)

RFF Details

Positive Results in 1H FY20: Rural Funds Group (ASX: RFF) is engaged in the leasing of agricultural properties and equipment. The market capitalisation of the company stood at $656.8 Mn as on 30th April 2020. As a responsible entity for RFF, Rural Funds Management Limited (RFM) advised the market that CBRE has been appointed to market the Mooral almond orchard. This decision follows the recent favourable comparable sales. During 1H FY20, the company reported a rise of 22% in property revenue to $37.6 million. Adjusted funds from operations per unit stood at 7.1 cents, reflecting an increase of 11%. This growth was due to JBS transactions, cattle acquisitions, development capital expenditure and lease indexation. The company has also received positive revaluations on macadamia orchards and cattle properties. The following picture gives an idea of taxation components for the total distribution:

.png)

Taxation Components (Source: Company Reports)

Guidance for Year Ahead: For FY20, the company expects adjusted funds from operations of 13.5 cents per unit and distributions per unit of 10.85 cents. RFF anticipates distribution per unit of 11.28 cents for FY21.

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The gearing and loan to value ratio of RFF are well within their respective limits. RFF’s Pro forma gearing and loan to value ratio stood at 29.3% and 41.0%, respectively. Gross margin and EBITDA margin of the company stood at 97.4% and 79.8% in 1H FY20, as compared to the industry median of 73.7% and 63.9%, respectively. Current ratio stood at 2.44x in 1H FY20 against the industry median of 0.64x. This reflects that RFF is in a decent position to address its short-term obligations against the broader industry. The stock of Rural Fund has provided returns of 3.72% and 8.03% within the span of three months and six months, respectively. We have valued the stock using P/E multiple based illustrative relative valuation method and arrived at a target price with an upside of high single-digit (in percentage terms). Therefore, considering the improvement in key margins, decent liquidity position and returns provided in the past months, we give a “Hold” recommendation on the stock at the current market price of $1.940 per share, down by 0.513% on 30th April 2020.

RFF Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Bravura Solutions Limited

.png)

BVS Details

Strong Wealth Management Sales Pipeline: Bravura Solutions Limited (ASX: BVS) provides software products and services to the clients operating in wealth management and funds administration industries. The market capitalisation of the company stood at $ 1.18 Bn as on 30th April 2020. Recently, the company announced that it has appointed Ms. Libby Roy on the role of an independent non-executive director, which became effective on 1st April 2020. During the half-year 2020, the company acquired Midwinter and FinoComp businesses, which are performing as expected with strong sales pipelines. Revenue and EBITDA for the period went up by 6% and 7% to $135.1 million and $25.5 million, respectively. The wealth management sales pipeline of BVS remains solid, with significant opportunities in all key markets. Revenue of the wealth management business rose by 1% to $91.0 million.

.png)

1H FY20 Results (Source: Company Reports)

Pipeline of Significant Opportunities: The strong market credentials of BVS in providing digital solutions and straight through messaging capabilities is generating a pipeline of contracted work from existing clients. It expects a pipeline of significant opportunities to support growth.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

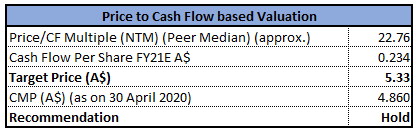

Price to Cash Flow Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company is placed well to take benefit of strong demand for its product portfolio in all its markets. Net margin of the company stood at 14.7% in 1H FY20, reflecting YoY growth of 1.9%. This implies that the company has improved its capability to convert its topline into the bottom line. Current ratio of the company stood at 2.24x in 1H FY20 against the industry median of 1.72x, which means BVS is well positioned to pay its short-term obligations against the broader industry. The stock of BVS has generated returns of 34.07% and 21.00% in the last one month and six months, respectively. We have valued the stock using P/CF multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as Pushpay Holdings Ltd (ASX: PPH), EML Payments Ltd (ASX: EML) and HUB24 Ltd (ASX: HUB) and arrived at a target price with an upside of high single digit (in percentage terms). Thus, in light of a pipeline of significant opportunities, improved capabilities to convert its topline into the bottom line and valuation, we maintain a “Hold” rating on the stock at the current market price of $4.860 per share, up by 0.413% on 30th April 2020.

BVS Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...