Sandfire Resources Limited

.png)

SFR Details

Sandfire Farm-In to Cheroona JV: Sandfire Resources Limited (ASX: SFR) is engaged in gold and base metal exploration. As on 11 February 2020, the market capitalisation of the company stood at ~$907.95 million. The company has recently announced that it has entered into a third farm-in agreement with Auris Minerals Limited wherein it has a right to earn a 70% interest in Cheroona Project tenements on making a discovery of a minimum 50,000 tonnes contained copper. Under the terms of the agreement, the company must spend a minimum of $1.2 million on exploration on the Cheroona Project tenements within the first 12 months.

Update on Strategic Partnership - Red Mountain Project: The company recently announced that it intends to withdraw from the Red Mountain Project Earn-In and Joint Venture Option Agreement and will remain an 11.3% shareholder of White Rock Minerals Limited. Post SFR’s withdrawal of interest, White Rock will retain 100% ownership of the Red Mountain Project, providing the shareholders greater upside leverage in value creation through discovery. The company has recently released its quarterly report for the period ending 31 December 2019, wherein it stated that it produced 18,258t of copper and 10,723oz of gold at C1 costs of US$0.83/lb. In the same time span, cash and deposits were $199 million.

.png)

Production & Operations (Source: Company Reports)

Guidance: SFR has a clear vision to create a diversified and sustainable metals company and is well-positioned for growth. The company gave guidance for FY20 production, wherein it expects to produce 70,000 to 72,000t of copper and 38,000 to 40,000 oz of gold. It also anticipates its C1 costs to be around ~US$0.90/lb.

Valuation Methodology: P/E Based Valuation

.png)

P/E Multiple based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SFR is trading close to its 52-week low of $5.040, proffering a decent opportunity for accumulation. During FY19, gross margin of the company stood at 67.1%, higher than the industry median of 41.1%. In the same time span, Return on Equity was 18.8% as compared to the industry median of 12.3%. Considering the current trading levels, higher gross margin and ROE, and decent outlook, we have valued the stock using price to earnings based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $5.180, up by 1.569% on 11 February 2020.

SFR Daily Technical Chart (Source: Thomson Reuters)

Beach Energy Limited

.png)

BPT Details

Strong Financial Performance: Beach Energy Limited (ASX: BPT) is engaged in the exploration, development and production of oil and gas. As on 11 February 2020, the market capitalisation of the company stood at $5.41 billion. The company has recently released its interim results for the period ended 31 December 2019, wherein it reported underlying EBITDA of $622 million and underlying NPAT of $274 million. The company has also achieved operational excellence with a production of 13.0 MMboe in 1H20. The company has also declared a fully franked interim dividend of 1 cent on ordinary fully paid shares of BPT which is to be paid on 31 March 2020.

.png)

1H20 Financial Performance (Source: Company Reports)

What to Expect: The company has recently narrowed down its FY20 production guidance wherein it expects to produce in the range of 27 to 28 MMboe. It also expects its capital expenditure to be in between $875 to 950 million and underlying EBITDA in the range of $1.275 to $1.35 billion.

Valuation Methodology: EV/Sales based Valuation

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

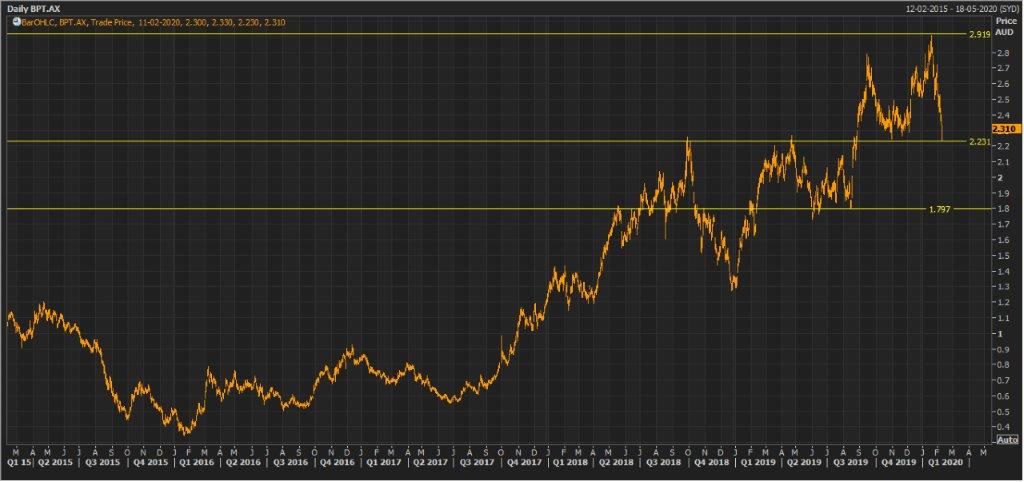

Stock Recommendation: As per ASX, the stock of BPT gave a return of 26.06% in the past 6 months. During FY19, EBITDA margin of the company stood at 65.4%, higher than the industry median of 32.2%. In the same time span, Return on Equity was 27.4% as compared to the industry median of 13.2%. Considering the returns, trading levels, higher EBITDA margin and ROE, we have valued the stock using EV/Sales based relative valuation method and arrived at a price correction of higher single-digit (in % terms). Hence, we have a watch stance on the stock at the current market price of $2.310, down by 2.532% on 11 February 2020.

BPT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...