OceanaGold Corporation

.png)

OGC Details

Robust growth in Haile Districtto be a Key Catalyst:Headquartered in Melbourne, OceanaGold Corporation (ASX: OGC) is a multinational gold producer company, which is involved in the production of gold, with its operating assets propagate in the New Zealand, US and the Philippines.

Shareholding update: On 3rd December 2019, the company issued an announcement stating that Van Eck Associates Corporation, a substantial holder of the company has increased the voting power from 11.51% to 12.51%. Recently, the company also announced that Michael F Wilkes, one of the directors has acquired 50,000 Common Shares for $140,000, effective 20 November 2019. Another Director, Ian MacNevin Reid acquired 57,000 direct common shares and 3,000 indirect common shares for a consideration of CAD2.63 per share.

OceanaGold Amends $200M Credit Facility: On 25 November 2019, the company revised a $200 million Revolving Credit Facility from a consortium of six banks, including Citi Bank, HSBC, Scotiabank, Commonwealth Bank of Australia, BNP Paribas & Natixis. The amendment reflected strong confidence of investors in the business and will help the company to further pursue its growth opportunities.

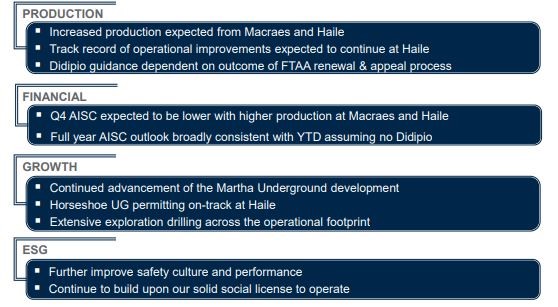

Quarterly Update:During the quarter ended 30 September 2019, the company reported strong exploration results at Haile. Total mine movements at Haile increased by 36% (Q-o-Q) and its unit mining costs decreased by 10%. Gold production for the period came in at 107,478 ounces, whereas copper production was 2,316 tonnes. Revenue for the quarter came in at $133.6 million, down ~28% from the year-ago quarter. The company reported All-In Sustaining costs at $1,122/oz on sales of 94,347 oz of gold and zero tonnes of copper sales.

Q3FY19 Results (Source: Company Reports)

The company reported cash and cash equivalents of $55.6 million at the end of the third quarter.Net operating cash flow for the period came in at $32.4 million and EBITDA stood at $33.9 million.

Outlook:The Company recently updated its 2019 outlook and now expectsGold and copper production for FY19 to be 460,000 and 480,000 ounces and 10,000 to 11,000 tonnes, respectively.AISC is anticipated to be in the range of US$1,040-US$1,090/oz.Also, the company is expected to receive the permit for its Horseshoe Underground Mine early in 2020.

Valuation Methodologies

Method 1: Price-to-Earnings Multiple Approach

.png)

PE Multiple Based Valuation (Source: Thomson Reuters)

Method 2: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Based Valuation (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock is trading below the average of its 52 weeks trading range of $2.520 - $5.280. As on 5th December 2019, the company’s market capitalisation stands at ~ $1.79 billion, with 622.28 million outstanding shares. The company expects production at Haile to improve in the fourth quarter. Considering the recent production data, development at Haile operations and decent guidance, we have valued the stock using two relative valuation methods, i.e., PE multiple and EV/EBITDA multiples and arrived at a high single-digit upside (in % terms). Hence, we recommend a "Buy" rating on the stock at the current market price of $2.770 per share, down by 3.484% on 5th December 2019.

OGC Daily Technical Chart (Source: Thomson Reuters)

Orocobre Limited

.png)

ORE Details

Adoption of Electric Vehicles and Commercial Grade Energy Storage system to Drive Growth: Orocobre Limited (ASX: ORE) is a global lithium carbonate supplier and producer of boron chemical and minerals. Its operations include its Olaroz Lithium Facility in Northern Argentina and Borax Argentina. ORE has provided an update on expected lithium carbonate price for December quarter to be approximately US$5400/tonne (FOB), subject to the planned shipping schedule. The company has made the decision to meet current pricing to ensure the retention of market share.

Orocobre’s Annual General Meeting 2019 Highlights: The company recently announced that the 2019 Annual General Meeting on 22nd November 2019, to pass few resolutions pertaining to the implementation of FY19 Remuneration Report, election and re-election of Directors, etc.

September Quarter 2019 Highlights: Revenue for the quarter came in at US$22.1 million, down 21% sequentially. Sales quantity for the period also increased by 45% on pcp. However, average price received fell by 52% on pcp. Gross cash margins for September quarter of 2019 (excluding export tax) was 78% down pcp. The September quarter of 2019 saw Borax delivering another good performance with sales volume of 12,480 tonnes, up 33% on pcp. Sales revenue was the same on qoq basis with the average price received down 6% on qoq basis due to the product mix. The company’s balance sheet remained strong, with a cash balance of US$223.5 million.

Production & Sales Data (Source: Company Reports)

What to Expect:Full-year FY20 production is expected to be at least 5% higher than FY19. For 2QFY20, the company expects average sales price to be US$6,200-6,500/tonne.

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week trading range of $2.180-$4.660. As on 5th December 2019, the company’s market capitalisation stands at $614.94 million, with 261.68 million outstanding shares. Considering the sales performance in September quarter, strong balance sheet, production guidance and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $2.360 per share, up 0.426% on 5th December 2019.

.jpg)

ORE Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...