Whitehaven Coal Limited

.png)

WHC Details

WHC Revises FY20 Production Guidance:Whitehaven Coal Limited (ASX: WHC) is engaged in the business of development and operation of coal mines in New South Wales. Recently, Lazard Asset Management Pacific Co increased its stake from 9.94% to 10.95% in the company, effective from December 6, 2019.

September’19 Quarter Key highlights: The managed saleable coal production rose by 23% on pcp, to 4,909k tonnes, and the company’s managed total coal sales stood at 5,546k tonnes during the quarter, up by 14% against the previous corresponding quarter. Total equity coal sales for the quarter stood at 4.5 million tonnes, with equity own coal sales of 3.9 Mn tonnes, which remained in line with the previous quarter.

.png)

Whitehaven Equity Totals for September Quarter (Source: Company Reports)

FY20 Guidance: Earlierthe company provided FY20 managed ROM coal production guidance to be in the range of 22.0 to 23.5 Mn tonnes with managed coal sales of 20.0 to 21.0 Mn tonnes. The unit cost guidance (excluding royalties) stood at $70 per tonne. However, due to challenges of sourcing skilled operators for Maules Creek and impacts from dust events related to severe and ongoing drought conditions in North West NSW, the company has issued updated FY20 guidance.

.png)

FY20 Guidance (Source: Company Reports)

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: WHC’s share generated a negative YTD return of 33.77%. Its gross margin, EBITDA margin and net margin for FY19 stood at 54.6%, 59.1% and 21.2%, better than the industry median of 44.3%, 32.2% and 15.3%, respectively, implying decent fundamentals of the company. ROE for FY19 stood at 15.1%, better than the industry median of 13.2%. Debt to equity ratio for FY19 stood at 0.12x, lower than the industry median of 0.24x. Hence, considering the company’s September Quarter production data, updated FY20 production guidance and current trading levels, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple approach and arrived at a double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.710, up 2.264% on December 11, 2019.

WHC Daily Technical Chart (Source: Thomson Reuters)

New Hope Corporation Limited

NHC Details

Unaudited Revenue for Oct Qtr Improved by 14% on pcp:New Hope Corporation Limited (ASX: NHC) is involved in the exploration, development, production and processing of coal, oil & gas. Recently, company’s wholly owned subsidiary, New Acland Coal Pty Ltd has received an application by Oakey Coal Action Alliance, for special leave to appeal to the High court of Australia in regard to orders made by the Queensland Court of Appeal. On November 1, 2019, Oakey Coal’s appeal was dismissed by the Queensland Court, allowing NAC's cross appeal. Oakey Coal has not challenged the appeal findings against it on the substantive issues of groundwater. Its current application seeking leave doesn’t change any position of the court’s final approvals for the New Acland Coal Mine Stage 3 Project, which is expected to generate $7 Bn in economic activity over the estimated 15-year life of the project.

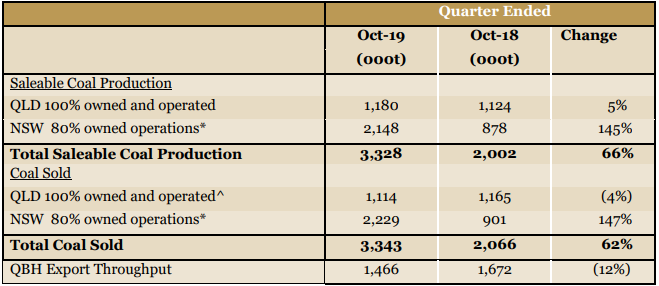

Key Highlights of October’19 Quarter: Unaudited revenue for the quarter increased by 14% to $327,340,000. Net profit after tax before non-regular items for the quarter decreased by 51% to $36,209,000, mainly due to a drop in the thermal coal price of 40% over the past year. Total saleable coal production was 66% higher and total coal sales was 62% higher than the prior corresponding period, mainly due to the increased ownership in the Bengalla mine.

Quarter Production Metrics (Source: Company Reports)

Outlook: Traditionally, Japan has demanded the highest quality coal in the world due to ash disposal costs. Taiwan is now seeking lower ash, higher energy coals for environmental reasons. Korea is seeking lower sulphur and considering tighter controls on ash. The scenario is positive for Australian coals in general. The company believes in a positive outlook for coals of Surat Basin quality which have low ash and sulphur, comparatively high energy and low emissions.

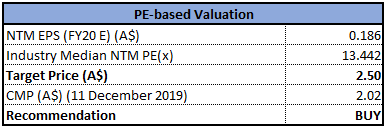

Valuation Methodology 1: Price to Earnings Multiple Approach

Price to Earnings (PE) Multiple Approach (Source: Thomson Reuters)

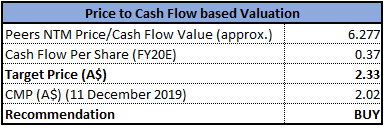

Valuation Methodology 2: Price to Cash Flow Multiple Approach

Price to Cash Flow Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: NHC’s share generated a negative YTD return of 39.51%. The company’s profitability margins, including gross margin, EBITDA margin and net margin for FY19 stood at 45.2%, 39.6% and 16.1%, better than the industry median of 44.3%, 32.2% and 15.3%, respectively. It posted positive revenue growth for the October quarter. However, due to decrease in coal prices, net income reduced by around 51% as compared to pcp. Given the effective coal operations with growing production and safety levels along with the projects in pipeline, the company seems well-positioned to meet the growing energy demands of its Asian customers. Hence, considering the above factors, we have valued the stock using two relative valuation methods, i.e., Price to Earnings and Price to Cash Flow multiples and arrived at a lower double-digit growth (in %). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.020, up 1.508% on December 11, 2019.

NHC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...