Stocks’ Details

Goodman Group

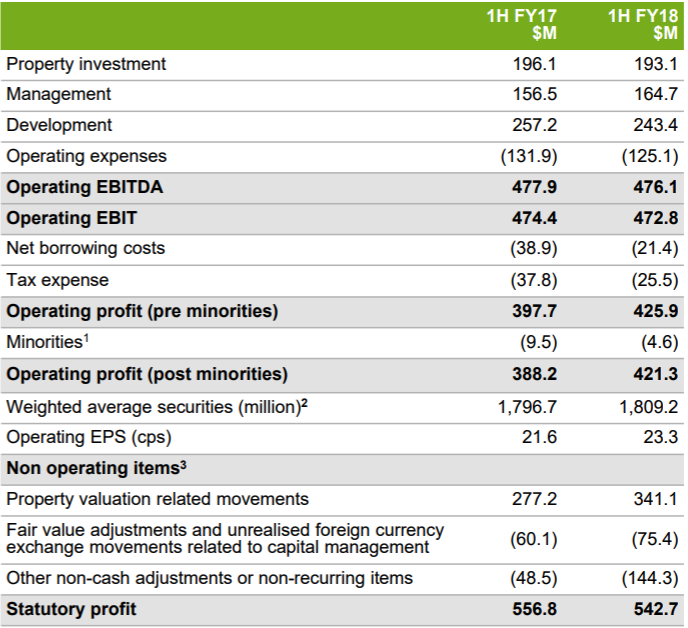

Upgraded FY18 operating EPS: Goodman Group (ASX: GMG) has posted operating profit growth of 8.5% YoY to $421.3 Mn in 1HFY18 as compared to previous corresponding period (pcp). As a result of this, EPS came at 23.3 cents per share in 1HFY18, up 7.9% over pcp. Beside this, Goodman’s statutory profit attributable to securityholders was down by 2.5% to $542.7 Mn in 1HFY18 as compared to prior corresponding period. This decrease was primarily due to the debt restructure expense of $82.1 million partly offset by higher property valuation gains. In the last five years, the group has sold over $11 billion worth of assets to focus on core markets and moved 80% of the $3.5 billion development workbook into Partnerships and reduced gearing from 19.4% to 6.4%. Cash and cash equivalent at the end of the half year amounted to 2,343.8 Mn. The Group has strong free cash flow that provides resources in the hand of the company to expand into new projects.

1HFY18 Performance (Source: Company Reports)

Further, the Group has built expertise at entering new markets and making success out of them. The expansion has helped the organization to build new revenue stream and diversify the economic cycle risk in the markets it operates in. Meanwhile, State Street Corporation and its subsidiaries became a substantial holder of the group with 5.00% interest as at February 27, 2018. Moreover, the Group disclosed to ASX that one of its directors, Ian Ferrier has direct interest in the Company and further acquired 4,541 shares through on-market trade under Directors’ Securities Acquisition Plan. Given the first half performance and sustained momentum into the second half, forecast FY18 operating EPS has been upgraded to 46.5 cents (up 8% on FY17) with forecast full year distribution of 28.0 cents per security (up 8% on FY17). The share price has risen 10.99% in past three months as on April 26, 2018 and currently is inching towards its 52-week high levels. We give an “Expensive” recommendation on the stock at the current price of $ 8.960.

National Storage REIT

Robust momentum in businesses: National Storage REIT’s (ASX: NSR) revenue in 1HFY18 has grown by 22% to $66,546,000 as against $54,359,000 in 1HFY17. The sales were mainly driven by strong storage revenue growth through increase in centre occupancy, rate per square and acquisition of additional centres during the same period. Profit after tax (PAT) recorded splendid growth of 153% YoY to $59,813,000 in 1HFY18 from $23,682,000 in 1HFY17. As a result of this, EPS stood at 11.56 cents per share in 1HFY18, up by 140.3% on year on year (YoY) basis. Based on strong first half year performance, the group affirmed an underlying EPS and earnings guidance of 9.6-10.1 cents per stapled securities and $51.5-$54.2 million, respectively for the full year. Return on Equity (RoE) has been consistently improving because of robust performance across the business verticals and recorded 204.0% in FY17 from 62.7% in FY14. We expect that the Group will continue to grow organically and inorganically in years to come on the back of developing multiple revenue stream to maximize the returns, product innovation, and acquisition across Australia and New Zealand region. Meanwhile, NSR stock was up 8.87% in the last six months as on April 26, 2018 and is trading at very high price to earnings ratio among its peer group. We give a “Hold” recommendation on the stock at the current market price of $ 1.610.

Business Strategy (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...