BHP Group Limited

Dividend policy of minimum 50% pay-out of underlying attributable profit: BHP Group Limited (ASX: BHP), formerly known as BHP Billiton Limited, has experience of 133 years with over 62,000 employees and contractors working over different locations worldwide. BHP deals into the four key segments – (1) Petroleum – exploration, development and production of oil and gas (2) Copper – mining of copper, silver, lead, zinc, molybdenum, uranium and gold (3) Iron Ore - mining (4) Coal – mining of metallurgical coal and energy coal. BHP has assets in the form of open-cut mines, underground mines, onshore and offshore O&G (oil & gas) production and facilities, producing a wide range of commodities.

Financial Performance of 1H FY19:

-

EBITDA for the period came in at US$ 10.5 billion against US$ 10.8 billion in 1H FY18. Higher costs and inflation offset the benefits of higher volume in WAIO (Western Australia Iron Ore) and favourable exchange rate.

-

-

Balance sheet remains healthy with a focus on reducing debt. Net debt for the period came in at US$ 9.9 billion as compared to US$ 10.9 billion in 1H FY18. BHP intends to keep the debt in the range of US$ 10 billion to US$ 15 billion and expects the debt trajectory to be at the lower end in the near term.

-

-

Net operating cash flow at US$ 6.7 billion, along with free cash flow at US$ 3.6 billion on the books shows strong liquidity and internal source of funds.

-

.png)

1HFY19 Business Segments’ Financial Summary (Source: Company Reports)

Consistent Dividend payer: BHP has a dividend policy of minimum 50% pay-out of underlying attributable profit. In-line with the policy, BHP has rewarded its investors with strong dividend pay-out along with share buy-back. Strong dividend history might attract investor fraternity to insulate the portfolio from market hiccups.

.png)

Dividend History (Source: ASX)

From the analysis standpoint, FY18 EBITDA margins for BHP of 51.4% were quite higher than the industry median of 33.1%, depicting a healthy picture on the operational front.However, BHP seems slightly leveraged with FY18 debt/equity ratio at 0.48x as compared to its industry median of 0.13x. At CMP of $ 39.03, stock is trading at PE of 26.72x with an annual dividend yield of 4.27%, which is well above 3.7% industry median. The current price-to-book ratio at CMP stands at 2.6x, relatively not cheap as compared to the industry median of 1.4x. Considering the share price movement, stock has outperformed frontline indices and appreciated 41.86% in one year, generating handsome returns to its investors. Sharp movement in share price in last one year and slightly stretched valuations lead us to maintain our “Hold” recommendation on the stock at the current market price of $ 39.03 per share.

Woolworths Group Limited

Completed Sale Of Petrol Business And Announcement Of Off-Market Buy-Back Offer: Woolworths Group Limited (ASX: WOW), formerly known as Woolworths Limited, is one of the largest retailers in Australia with prestigious brands – Woolworths, Dan Murphy’s, Countdown, BWS, BIG W with total store network at 3,240, which includes 1,008 Australian Food, 181 New Zealand Food, 1,545 Endeavour Drinks, 183 BIG W, and 323 hotels. On the financial front, Revenue growth for FY18 grew by 3.4% to $ 56,726 million whereas Net profits for FY18 came in at $ 1,676 million recording a growth of 13.1% (Y-o-Y). Gross margins and EBIT margins for FY18 also improved to 29.5% and 4.5% from 29% and 4.2%, respectively.

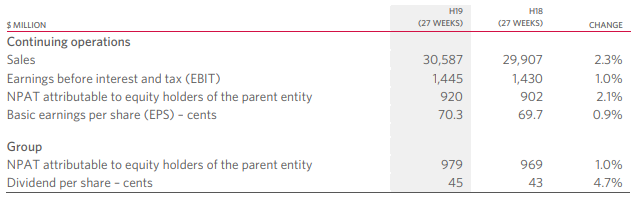

Looking at the half-yearly performance, financials were subdued with sales growth at 2.3% in 1H FY19 to $30.587 million. Net profits for the same period saw slower growth of 2.1% to $920 million on account of lower customer demand. Recently, the group announced that it has successfully completed the sale of its Petrol business to EG Group. Further, the proceeds from the sale to be returned to shareholders via a $1.7 billion off-market buy-back offer. The Buy-Back offer will be conducted by way of an off-market tender process which will open on 16 April 2019 and close on 24 May 2019. The sale of Woolworths Group’s Petrol business likely results around $1.1 billion after tax and it will be recorded as a significant item in the FY19 results.

that it will be conducting an off-market buy-back (Buy-Back) to return up to A$1.7 billion to shareholders, expected to complete in May 2019.

1HFY19 Financial Performance (Source: Company Reports)

What to Expect in FY19: Revenue from the Australian Food for Q1 FY19 was lower, which management expects to improve going forward on the back of certain plans to be adopted differentiating it from its rivals. WOW will keep an eye on productivity improvements, and for that matter, WOW will open a state-of-the-art distribution centre in South Melbourne in late FY19. BIG W is in the initial stages of a turnaround and will see a further reduction in losses in FY19.

Analysing the key ratio metrics, WOW has been on par with the industry. 1HFY19 EBITDA margins for the company stood at 6.7%, which is slightly higher than the industry median of 6.3%. Similarly, net margins at 3.1% vs industry median of 2.4 also portray a decent financial picture.

At CMP of $30.85, the stock is trading at an annual yield of 3.06% (as compared to its industry median of 8.7%). The stock is available at PE of 23.47x, which is quite higher than its industry median of 9.5x. Price to book value of 3.8x for WOW is slightly above than the industry median of 4x.

Looking at the share price performance, the stock has appreciated 17.46% (one year), 6.62% (YTD) and 11.4% (six months), giving good returns to its shareholders. Considering the aforesaid facts and future prospects, we maintain our “Hold” recommendation on the stock at the market share price of $ 30.85 (down 0.74% on April 02, 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...