Woodside Petroleum Limited

Scarborough Resource Volume Increased by 52%:Woodside Petroleum Limited (ASX: WPL) is engaged in the management and operation of hydrocarbon exploration, development, production, transportation and marketing. It is also engaged in the implementation and operation of the North West Shelf Gas Project. The market capitalisation of the company stood at $31.06 billion as on 8th November 2019.

Scarborough field reported an estimated gross contingent resource (2C) dry gas volume of 11.1 Tcf, which is up by 52% from 7.3 Tcf. Woodside Petroleum Limited’s interest in Greater Scarborough comprises of 75% interest in WA-1-R and 50% interest in each of WA-61-R, WA-62-R and WA-63-R. It was added that, as a result of Scarborough resource volume increase, Greater Scarborough contains estimated gross dry gas contingent resource (2C) volume of 13.0 Tcf, a 41% rise from the previous 9.2 Tcf.

As per the CEO of the company, the increase in the estimated resource volume at Scarborough highlighted its ability as a world class project, which could meet the growing demand for gas in Asia and beyond and supplying the domestic market in WA.

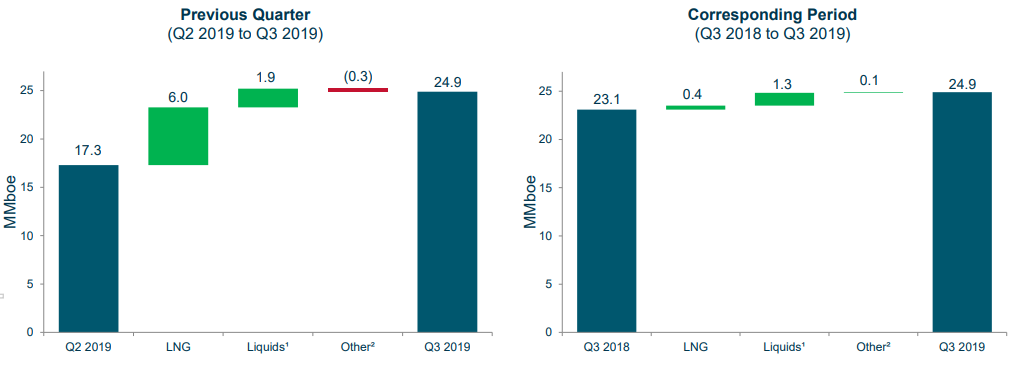

Woodside Petroleum Limited Records Revenue Growth of 58%: The company recorded sales revenue of $1,164 million, up by 58% QoQ, led by a 44% increase in production from the previous quarter and stronger realised LNG pricing. The company recorded production of 24.9 MMboe and achieved 99.7% reliability at Pluto LNG with record quarterly production and daily production rates.

LNG Production (Source: Company Reports)

Future of WPL: The company is targeting a final investment decision for the development of the Scarborough gas resource in H1 2020. Scarborough gas will be initially processed on the deep-water floating production unit and transported through an around 430 km pipeline to the proposed second LNG production train at existing Woodside-operated Pluto LNG facility on WA’s Burrup Peninsula.

Stock Recommendation: WPL has significantly increased dry gas volumes from its Scarborough field. With the increase in production, the company has also maintained its EBITDA margins. In FY16, the company reported EBITDA margins of 62.7% and in FY19 it reported EBITDA margin of 71.0%. As per the ASX, the stock has gained 5.81% in the last one month and is currently trading slightly above the average of 52-week high and low. Based on final investment decision for the development of the Scarborough gas resource and current trading levels, we give a “Hold” rating on the stock at the current market price of $33.630 per share, up 2.033% on 08 November 2019.

Worley Limited

BP Exploration Extends its Contract with Worley Limited:Worley Limited (ASX: WOR) provides professional services to help their customers to meet the world’s changing energy, chemicals and resources needs. The market capitalisation of the company stood at $7.27 billion as on 8th November 2019.

Worley Limited has been awarded a two-year contract extension by BP Exploration to provide wells support services and fluids hauling for BP’s North Slope operations.As per the contract, the company will continue to provide wells support services and fluids hauling, which includes modifications, maintenance, operations and drilling support for new and existing wells. It is an extension of the contract, which was originally awarded in 2012.

Worley Limited Gets Master Services Agreement by Nouryon: Worley Limited has been awarded by Master Services Agreement (MSA) from Nouryon Chemicals B.V. to provide engineering, procurement and construction management (EPCM) services.As per the agreement, twenty Nouryon sites will be provided services, which are located across Europe and for a period of five and a half years.

Outlook for Future: The growth in the backlog and the market indicators of energy, chemicals and resources indicate the continued improvement in market conditions.However, the company’s markets are being tempered by the macroeconomic uncertainty. But after the acquisition of ECR, the company has enhanced the diversity and resilience of its earnings. In FY20, the company expects to deliver the benefits of the acquisition, which includes realization of cost, margin, and revenue synergies.

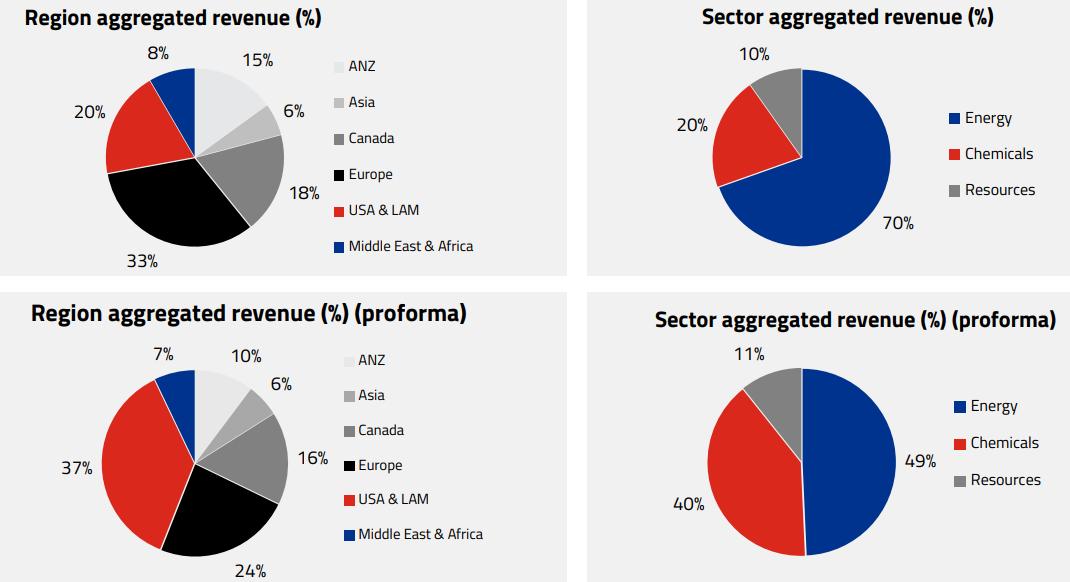

Revenue Split of the company (Source: Company Reports)

Stock Recommendation: The company is moving at a high pace as it has grabbed two agreements from BP Exploration and Nouryon. WOR’s latest acquisition of ECR will further help it to improve its earnings in FY20. The company has delivered a CAGR growth of 86.28% in the bottom-line over the period of FY16 - FY19. EBITDA margin of the company has improved from 6.4% in FY17 to 7.0% in FY19. Hence, considering its new contracts, latest acquisition and decent margins, we give a “Buy” rating on the stock at the current market price of $14.300 per share, up 2.362% on 8th November 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...