ImpediMed Limited

Revenue from SOZO contracts in March’19 quarter increased by 12% pcp: ImpediMed Limited (ASX:IPD) is a global provider of medical technology to non-invasively measure, monitor and manage tissue composition and fluid status using bioimpedance spectroscopy. It operates in the US (San Diego), Australia (Brisbane) and Europe (Greece) with a total of 68 staff.

The Company recently published its investor presentation where it highlighted its Software as a Service (SaaS) Business Model is now well established in Lymphoedema. Its SOZO devices have been sold to hospitals and clinics.Its monthly subscription fee is based on indications licensed and estimated case load per device.

March’19 Quarter Key Highlights: The contracted revenue pipeline increased by 10% to $7.7 Mn. The total contract value for SOZO was reported at $1.3 Mn in the March’19 Quarter and $9.8 Mn since SOZO launch. The annual recurring revenue for SOZO contracts in the quarter increased by 12% to $2.8 Mn. The net operating cash outflow for the quarter period was reported at $4.8 Mn. During the period, $1 Mn cash receipts from customers were reported, while cash of around $17.1 Mn was reported at the end of the period. IPD reported 33 new contracted SOZO devices, and a total of 350 such devices since launch.

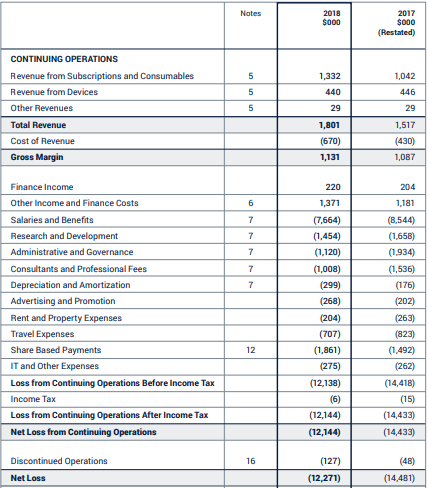

H1FY19 Financial Performance: Total revenue for the period increased by 20% pcp to $1.8 Mn. Net loss from both continuing and discontinuing operation, decreased by 15.26% pcp to $12.27 Mn.

H1FY19 P&L Statement (Source: Company Reports)

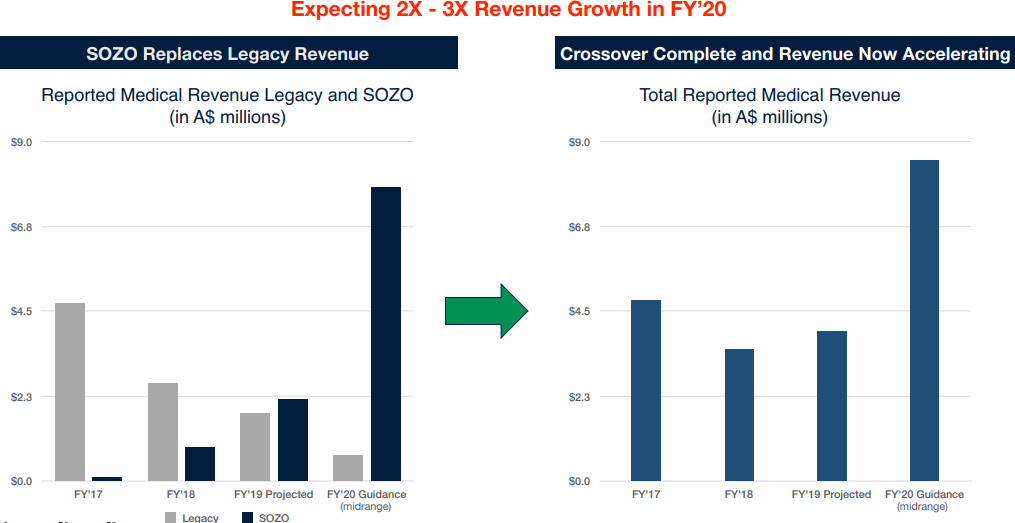

What to expect: As per the release, at present around 6.5 Mn people (Americans) has been diagnosed with the heart failure, and this number is expected to increase by 46% to more than 8 Mn people by 2030. The annual cost in heart failure (health care services, medications to treat heart failure and missed days of work) has been estimated at ~$31 Bn. The report also states that the SOZO revenue will replace legacy revenue in FY19 and FY20. Total reported medical revenue is expected to be in the range of $2.3-$4.5 Mn and $6.8-$9.0 Mn in FY19 and FY20, respectively.

Revenue Growth Expectation (Source: Company Reports)

Stock Recommendation: ImpediMed’s share is presently trading at its 52 weeks low level, and therefore probability to bounce back increases. Its current ratio for H1FY19 stands at 5.61x, which is better than the industry median of 2.83x, which implies the company is in a better position to address its short-term obligations. Recently,the company informed that Kinetic Investment Partners Ltd became a substantial holder of the group with voting rights of 5.56% since 16th June 2019. Meanwhile, the stock has delivered the return of -45.24% and -48.89% in the span of the previous one month and three months, respectively. Hence, considering the aforesaid facts and current trading level, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.115 per share.

Ellex Medical Lasers Limited

Trading Towards 52-week Lower Levels: Ellex Medical Lasers Limited (ASX: ELX) recently published its investor presentation where it highlighted that it operates in comprehensive range of ophthalmic lasers, evolving consumable device business and diagnostic equipment, targeting Glaucoma, Age-related macular degeneration (AMD), Diabetic eye disease, Secondary cataracts and Vitreous opacities. It has installed base of over 35K Ellex ophthalmic laser and ultrasound systems globally. Till date, it has sold more than 100K Ellex iTrack™ consumable devices to treat glaucoma. It has a direct sales network in the major markets such as Japan, USA, Australia, Germany, and France, and product distribution in around 100 countries.

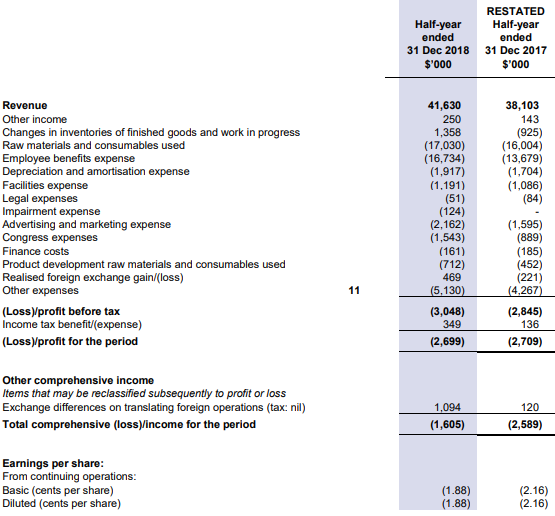

H1FY19 (ended on December 31, 2019) Key Highlights: Group’s sales revenue increased by 9% pcp to $41.6 Mn. Following the release of the LEAD clinical trial data in intermediate age-related macular degeneration in September’18, Ellex 2RT® revenue increased by 532% pcp to $1.2 Mn. Ellex iTrack™ revenues increased by 24% to $6.5 Mn, driven by continued growth in volume by ~27% and revenue by ~39% in the United States of America.

Its earnings before interest, tax, depreciation and amortization (EBITDA) loss improved by 12% on pcp to $0.85 Mn, majorly driven by a 53% increase in Lasers & Ultrasound EBITDA to around $5.9 Mn, offset by an increase in expenditure in the high growth segments comprising glaucoma and iAMD diseases. ELX reported net loss decreased by 0.3% pcp to $2.7 Mn.

H1FY19 P&L Statement (Source: Company Reports)

What To Expect: While Ellex 2RT and Ellex iTrack performed strongly in the H1FY19, there was an unexpected slowdown in core Laser % Ultrasound sales in the United States of America and EMEA (Europe, the Middle East and Africa) in the Q2FY19, which saw group revenue growth moderate for the first half. The Company expects its Ellex iTrack’s growth will continue in the FY19, and it anticipates its EBITDA to be like FY18 levels.

Earnings before interest, tax, depreciation and amortization (EBITDA) growth for Laser & Ultrasound segment in FY19 is expected on FY18, with continued clinical adoption of Ellex Tango™ / Ellex Tango Reflex™ in glaucoma along with meticulous cost management. ELX aims to grow its group sales along with delivering an improved EBITDA result in FY19 subject to foreign exchange rates and global economic conditions.

Stock Recommendation: Ellex Medical’s share is presently trading closer to its 52 weeks low level ($0.500). Its gross margin for H1FY19 stands at 62.4%, which is lower than the industry median of 68.4%. Its current ratio for H1FY19 stands at 1.95x, which is lower than the industry median of 2.83x. Given the mix scenario, we have a wait and watch view on the stock at the current market price of $0.540 per share (down 2.703% on June 20, 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...