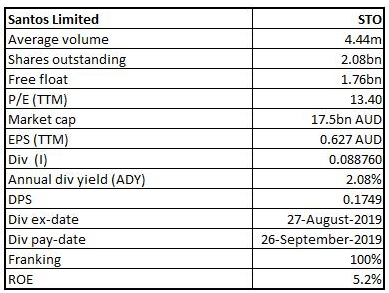

Santos Limited

STO Details

Record Quarterly Production and Sales Volumes: Santos Limited (ASX: STO) is engaged in the exploration and production of gas and petroleum, natural gas treatment and marketing, crude oil, condensate, naphtha and liquid petroleum gas and transportation by pipeline of crude oil. As on 18th December 2019, the market capitalisation of the company stood at $17.5 billion. For the period ending 30th September 2019, the company witnessed a record production of 19.8 mmboe, up by 7%on the previous quarter, along with record sales volumes of 25.2 mmboe, a rise of 13% as compared to Q2 FY 2019. Santos Limited generated $214 million in free cash flow in Q3 FY 2019, which brings total free cash flow for nine months to $852 million.

Financial Performance (Source: Company Reports)

What to Expect from Santos Going Forward: Recently, the company has narrowed its 2019 production guidance to 74-76 mmboe and its sales volumes to 93-95 mmboe. However, it was added that the acquisition of ConocoPhillips’ northern Australia interests might help in driving production higher in 2020. Notably, the company has lifted up its 2025 production target further to 120 million barrels of oil equivalent, which is more than double output of 2018. This new target represents a cumulative annual growth rate in production of more than 8% to 2025.

The acquisition of ConocoPhillips’ northern Australia business increases pro-forma production by around 25% and reduces forecast 2020 free cash flow breakeven oil price by approximately US$4 per barrel. The company is targeting pre-tax synergies of US$50 million to US$75 million per annum, driven by Santos operatorship and efficiencies.

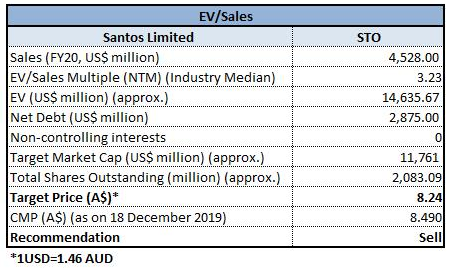

Valuation Methodology: EV/Sales Multiple Valuation

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of STO gave a return of 21.74% in the past six months and a return of 3.58% in the last one month. The stock is trading close to its 52-week high of $8.520.During 1H19, EBITDA margin of the company stood at 57.2%, higher than the industry median of 36.2%. Return on Equity was 5.2%, slightly higher than the industry median of 5%. We have valued the stock using one relative valuation method, i.e., EV/Sales multiple approach and arrived at the target price, offering downside in percentage terms. Hence, we recommend a “Sell” rating on the stock at the current market price of $8.490, up by 1.071% on December 18, 2019.

STO Daily Technical Chart (Source: Thomson Reuters)

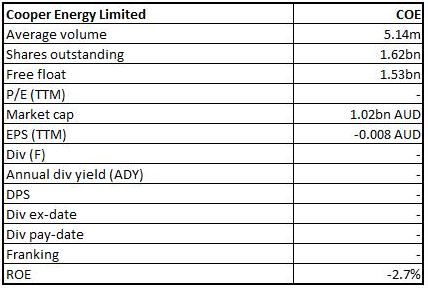

Cooper Energy Limited

COE Details

Sole Gas Project Update: Cooper Energy Limited (ASX: COE) is an upstream oil and gas exploration and production company, of which, primary purpose revolves around securing, finding, developing, producing and selling hydrocarbons. As on December 18, 2019, the market capitalisation of the company stood at $1.02 billion. The company has recently provided an update on the status of the Sole Gas Project, particularly on the upgrade of the Orbost Gas Plant as well as the outlook for first gas production. It was stated that Sole gas field is ready to produce gas on completion of the Orbost Gas Plant upgrade and commissioning. It needs to be noted that COE has also completed the transaction for the acquisition of the Minerva Gas Plant by participants in Casino Henry joint venture.

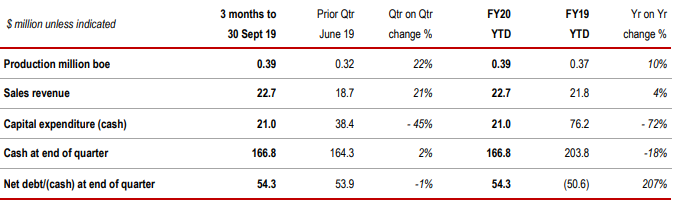

Record Quarterly Sales Revenue: For the quarter ended 30 September 2019, the company reported a record quarterly sales revenue of $22.7 million, up by 21% from $18.7 million, due to higher gas production and prices. During the same time period, quarterly production went up by 22% to 0.39 million boe from prior quarter’s 0.32 million boe. COE also witnessed successful oil appraisal drilling results at Parsons in the Cooper Basin and spudded Dombey-1, which recorded a new gas field discovery in the onshore Otway Basinafter the quarter’s end.

Financial Performance (Source: Company Reports)

What to Expect:The company is optimistic with respect to the start of gas supply from the Sole gas field, which will bring a step change in the company’s gas production and cash generation. Once, Sole is in production, the company will establish the ‘twin-hub’ model with production from the Gippsland and Otway basins, providing COE with development and exploration opportunities with the potential to contribute significant growth in the years from 2022 to 2025.

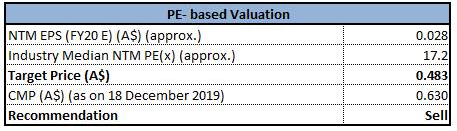

Valuation Methodology: Price to Earnings Multiple Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gained 48.24%, 20% and 12.5% in the last one year, six months and one month, respectively. The stock is inclined towards its 52-week high of $0.685. Given the valuation and current trading levels, we are of the view that most of the growth catalysts have been discounted at the current juncture. During the year, gross margin at 44.4% was broadly in-line with the industry median of 44.3%. EBITDA margin at 49.7% stood higher than the industry median of 32.2%. We valued the company using a relative valuation method, i.e., price to earnings multiple and arrived at the target price, offering a downside (in % terms). Hence, we recommend a “Sell” rating on the stock at the current market price of $0.630 per share as on 18 December 2019.

COE Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...