Origin Energy Ltd

Resilient Energy Markets: Formed in 2000 and headquartered in Sydney, Origin Energy Limited (ASX: ORG) is Australian listed public company which manages energy businesses that includes production of natural gas, and generation of electricity.

Shareholding update: On 6th December 2019, the company announced that Frank Calabria, one of the company’s director have disposed 60,000 Common Shares for $8.75 per share.On 6th November 2019, Frank Calabria, who holds a direct interest in the company disposed 570,150 options and 57,739 Performance Share Rights under an Equity Incentive Plan.

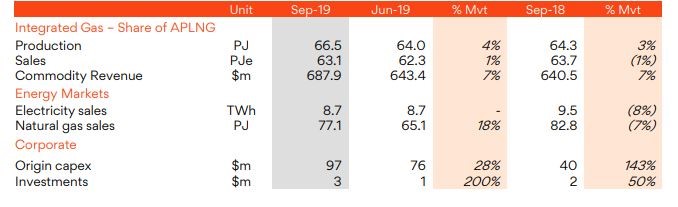

Quarterly Update:During the quarter ended 30 September 2019, Origin Energy LimitedAPLNG production increased 3%, year over year, primarily due to better-than-expected accessibility and the ERIC pipeline coming online as compared to previous quarter. APLNG revenue increased 7% year over year, mainly due to better oil prices and enhanced LNG volumes.

Sales from Energy Markets electricity went down 8% year over year owing to lower-than-expected business sales, lower customer numbers coupled with market changes. Volumes of Energy Markets gas was down 7% year over year quarter due to absent of wholesale contracts in the near-term. The company’s increased 143% year over year and came in at $97 million.

Quarterly Results (Source: Company Reports)

What to Expect:In FY20, Australia Pacific LNG’s production is predicted to be in the range of 690 to 710 petajoules. The company updated APLNG break-even outlook from US$33 and US$36 per boe to US$31 and US$34/boe. In FY20, Energy Markets’ Underlying EBITDA is now expected to in the range of $1,400 – $1,500 million. During fiscal 2020, corporate costs are now expected to be between $60 to $70 million. The company continues to expect capital expenditure and investments, to be in the range of $530 to $580 million.

.jpg)

FY20 Guidance (Source: Company Reports)

Valuation Methodology: P/E Multiple Approach

.png)

P/E Multiple Approach (Source: Thomson Reuters), NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation:As per ASX, the company’s stock is trading above the average of its 52-weeks trading range of $6.030 - $8.790. Over a period of 1 year, the stock has reported a positive return of 26.7%. The business has attracted further growth opportunities, after constant production at Australia Pacific LNG, elevated effective oil prices and cost control measures. Hence, considering the above factors, we give a “Hold” recommendation on the stock at the market price of $8.570, up 0.469%.

Oil Search Limited

Continuous Achievement in PNG Oil Field Exploration Programme are Key Catalysts: Established in 1929, Oil Search Limited (ASX: OSH) is involved in the oil and gas exploration and production in Papua New Guinea. The company has approximately 51% interest in major oil assets situated in North Slope of Alaska. On 5th December 2019, the company provided a detailed update report on exploration and appraisal drilling status. In November 2019, the company stated that the drilling of Gobe Footwall recoded a 17-½ inch hole with 1,260 metres of depth. By the end of the month, the well was 2,226 metres deep.The company plans to further continue with the drilling initiatives. Total production during the first half of 2019 was 14.1 mmboe, up more than 38% year over year.

Quarterly update: During the quarter ended 30 September 2019, the company reported third-quarter total production of 6.81 mmboe, down 10% year over year. Total volume sales of during the period came in at 6.47 mmboe. Total revenues stood at US$361.1 million, down 24% year over year. Cash in hand during the quarter came in at US$547.3 million. Credit facilities amounted to US$635.7 million. The company’s net debt came in at US$3,042 million as compared to US$2,871.6 million reported at the end of year-ago quarter.

Q3 FY19 Results (Source: Company Reports)

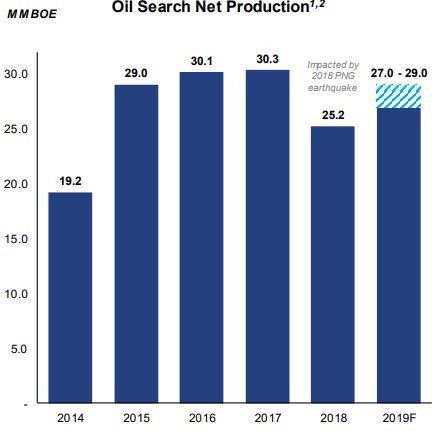

Outlook:For 2019, the company expects oil search-operated production to be in the range 2.8 – 3.5 mmboe. Total PNG LNG production in FY19 is expected to be 24 – 26 mmboe, whereas Oil Search production net production is expected to be 27 – 29 mmboe. Further, the company expects investment expenditure to be in the range of US$823-883 million. Other operating costs for the period went up slightly to US$140 - 150 million, primarily due to due to lower-than-expected recoveries from overheads and higher execution costs. The Company intends to drill and explore Gobe Footwall Well in the coming quarter.

Oil Search Net Production (Source: Company Reports)

Valuation Methodology: Price to Cash flow Multiple Approach

.png)

Price to Cash Flow Multiple Approach (Source: Thomson Reuters), NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: As per ASX, the stock is trading above the average of its 52 weeks high-low. As on 6 December 2019, the company’s market capitalisation stands at ~ $10.83 billion, with 1.52 billion outstanding shares. The company has a liquidity management plan and aims in drilling and exploring existing Gobe production facilities, extend the life of the mature Gobe fields and therefore postponing field rejection. The company has forward plan to drill ahead into the target lagifu and Toro reservoir. Considering the above factors, valuation, and recent announcement for construction of purified spherical Graphite for BAM Project, we have a “Buy” rating on the stock at the current market price of $7.060 per share, down by 0.563% on 6th December 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...