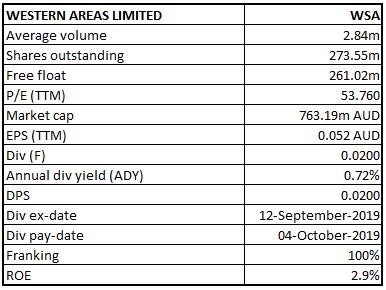

Western Areas Limited

WSA Details

No Major Incident at Forrestania Nickel Operation Following Bush Fire Incident:Western Areas Limited (ASX: WSA) is involved in mining, processing and sale of nickel sulphide concentrate. It is also engaged in the continued assessment of development feasibility of the high-grade nickel mines and exploration for nickel sulphides, and other base metals.

Recently, the company provided a final update regarding the bush fire incident that occurred in the area of the Forrestania Nickel Operation (FNO). WSA has confirmed the safety of all the personnel, with most staff returning to normal working duties over the weekend. Mains power was interrupted as a result of damage to three Western Power poles north of FNO and was restored shortly. Mining operations continued on-site using back-up power generation. The Cosmic Boy mill operations were suspended until the power transmission was restored; however, the company does not expect any impact to nickel production or cost guidance for FY20 as a result of the incident.

September’19 Quarter Key Highlights:Mine nickel production for the quarter stood at 5,805 tonnes. Mill nickel production for the quarter stood at 5,259 tonnes. Unit cash cost of nickel in concentrate for the quarter stood at A$3.06/lb. Nickel sales for the quarter stood at 5,051 tonnes. Cash at bank as on September 30, 2019, was reported at A$165.9 Mn as compared to A$144.3 Mn as on 30 June 2019 due to net cashflow of A$21.6 Mn.

.png)

Production Overview of September’19 Quarter (Source: Company Reports)

What to Expect:As per the release, the construction programme for the Odysseus mine is on schedule and progressing well, which is expected to support the company’s long-term future of profitable nickel production. FY20 Nickel production guidance has been estimated in the range of 21,000 to 22,000 tonnes for the full year, with a unit cash cost of nickel in concentrate to be in the range of A$2.90/lb to A$3.30/lb.

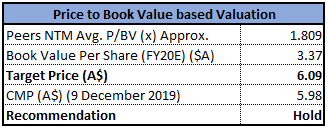

Valuation Methodology: Price to Book Value Multiple Approach

.png)

Price to Book Value Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation:WSA’s share generated a positive YTD return of 46.84%, and in the span of six months, it has posted a return of 32.23%. Company’s September quarter performance was in-line with the production and cost guidance across the operation, which combined with increased nickel prices, provided strong operational cashflow. Additionally, the construction of the Odysseus mine is advancing as planned, supporting the development of the company’s next long-life nickel sulphide operation. Net margin for FY19 stood at 5.3%, better than the FY18 result of 4.8%. Its current ratio for FY19 stood at 3.55x, better than the industry median of 1.82x, which implies that the company is in a better position to address its short-term obligations. Its cash cycle for FY19 stood at 38.3 days, lower than the industry median of 46.6 days. Hence, considering the current trading levels, business performance and FY20 guidance, we have valued the stock using a relative valuation method, i.e., Price to Book Value Multiple Approach and arrived at a target price of lower double-digit growth (in %). Hence, we recommend a “Hold” rating on the stock at the current market price of $2.840, up 1.792% on December 9, 2019.

WSA Daily Technical Chart (Source: Thomson Reuters)

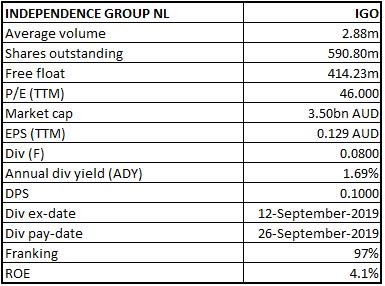

Independence Group NL

IGO Details

PAN Rejects Take-Over Bid from IGO:Independence Group NL (ASX: IGO) is a nickel, gold and copper-zinc-silver mining, development and exploration company.

On December 9, 2019, Panoramic Resources Ltd (ASX: PAN) rejected the takeover bid by Independence Group, where IGO offered one IGO share for every 13 PAN Shares. The reason has been attributed to the opportunistic timing, which may deprive PAN shareholders a future potential value plus a fear of dilution of PAN’s assets through accepting the offer. Moreover, PAN’s largest shareholder Zeta Resources (35.17%) stated that it does not intend to accept the offer in its current form and the offer appears to be highly conditional with no certainty to proceed.

In another update, Encounter Resources Limited announced that the large scale (~100-line km) magnetotelluric (MT) survey completed at the Yeneena project in the Paterson Province has identified a suite of new copper drill targets. The Yeneena project is a collaboration between Independence Group and Encounter Resources. IGO may, at any time before March 1, 2020, elect to enter an earn-in agreement to spend up to $15 Mn to earn a 70% interest in Yeneena.

.png)

Key Financial Metrics (Source: Company Reports)

What to Expect:The Paterson Province is a highly fertile district with enormous potential for new copper discoveries under thin sand cover. Applying new technologies is providing an improved understanding of the geological framework in areas where Encounter Resources Ltd has already drilled high grade copper mineralisation. These new targets generated are now being integrated and refined to be ready for drilling in the 2020 field season.

.png)

September’19 Quarter Production and FY20 Guidance Information (Source: Company Reports)

Valuation Methodologies:

Method 1: Price to Book Value Multiple Approach

Price to Book Value Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

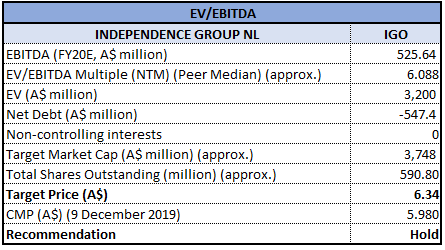

Method 2: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation:The stock generated a positive YTD return of 63.36%, and in the span of six months, it has posted a return of 38.55%. Its gross margin and EBITDA margin for FY19 stood at 62.6% and 44.3%, better than the industry median of 43.4% and 29.5%, respectively, implying decent fundamental for the company. Its current ratio for FY19 stood at 4.44x, better than the industry median of 1.82x, which implies decent liquidity position for the company. Its debt to equity ratio for FY19 stood at 0.05x, lower than the industry median of 0.13x. Company’s Q1FY20 revenue increased by 29% on Q-o-Q to $263 Mn and underlying EBITDA increased by 64% on Q-o-Q to $154 Mn. Considering IGO’s Q1FY20 performance, recent development at Yeneena project under partnership with Encounter Resources and FY20 guidance, we have valued the stock using two relative valuation methods, i.e., Price to Book Value and EV/EBITDA multiples and arrived at target of single-digit growth (in %). Hence, we, recommend a “Hold” rating on the stock the current market price of $5.980, up 0.843% on December 9, 2019.

IGO Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...