Perseus Mining Limited

.JPG)

PRU Details

Earnings impacted by non-recurring expenses: Shares of Perseus Mining Limited (ASX: PRU) moved up over 8% on 1 September 2017, with positive sentiments and commodity price movements. The company recently announced its FY17 results and reported a net loss after tax of $79.3 million on account of a foreign exchange loss of $11.7 million (gain of $9.2 million in FY16), mainly due to the appreciation of the Australian dollar against the US dollar and revaluation of an intercompany loan. Additionally, a loss of $27.5 million was incurred following the acquisition in April 2016 of Amara Mining plc (Amara) including a one-off expense of $24.5 million to settle outstanding claims made by Bayswater Construction and Mining (BCM) against Amara in relation to mining services provided by BCM prior to 2015. Further, a write down of capitalised exploration expenses totalling $16.1 million was incurred on tenements in Ghana following a write down of $17.9 million in the prior year. A reduction in the carrying value of low grade stockpiles due to a net realisable value adjustment led to a negative impact on earnings of $6.3 million, compared with a profit contribution of $13.1 million in 2016 coupled with 17% increase in depreciation and amortisation expense of $56.2 million due to higher rates of mining and processing. An increase in the capital base following investment in plant, equipment and relocation housing added to the loss.

.png)

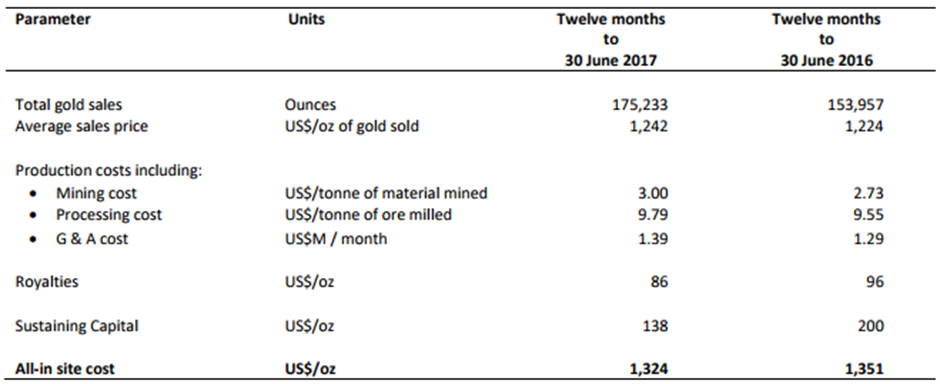

FY17 results summary; (Source: Company reports)

Development of Sissingué and Yaouré Gold Projects remains on track: Notably, the company achieved a solid turnaround in operating performance in the second half of the 2017 and remains on track to report increased production and earnings in 2018. Perseus’ cornerstone Edikan Gold Mine in Ghana (Edikan) produced 100,218 ounces in the six months to June 2017, up 32% from 75,999 ounces in the preceding six months to December giving total annual production of 176,217 ounces. The improvement was driven by increased mining rates, higher head grade of processed ore, significantly improved plant throughputs and rising recoveries following a significant capital works program completed in December 2016. Further, development of Sissingué remains on schedule and project development is funded through a US$40 million project debt finance facility provided by Macquarie Bank Limited and cash reserves. The Definitive Feasibility Study for Perseus’s third prospective gold mine, the Yaouré Gold Project in Côte d’Ivoire is continuing to advance on all fronts and is on schedule for completion in the December 2017 quarter. Preliminary results of the DFS confirm that key project parameters are either in line with or better than those estimated by Perseus prior to the acquisition of the project in April 2016.

Key financial statistics; (Source: Company reports)

Notably, operating cash flows in H2FY17 rebounded to positive $18.2 million from negative $17.4 million in the first six months, despite the bulk of the payment of the legal settlement with BCM being paid in the second half of the year. On the other hand, group gold production for FY18 is expected to increase to 250,000 - 285,000 ounces from 176,218 ounces in FY17. The projected increase is said to be driven by higher output at Edikan, together with the commencement of production at Sissingué, which is scheduled to produce its first gold in the March 2018 quarter. Together, the two sites are expected to deliver a reduction in Group all-in site costs to US$950-1,100/ounce in 2018, from US$1,324/ounce in 2017. Given the ongoing mining developments, and improving resource and production outlook with reduction in costs, we maintain a “Buy” recommendation on the stock at the current market price of $ 0.32

PRU Daily chart; (Source: Thomson Reuters)

Independence Group NL

.JPG)

IGO Details

Earnings driven by higher realisations: Shares of Independence Group NL (ASX: IGO) also surged 4.7% at the back of positive sentiments and commodity price movement, post a decline of about 10.2% in the last six months as on 31 August 2017. For FY17, IGO reported 1% year on year (yoy) growth in revenue at $421.9 million, driven by 10% increase in long operation’s total revenue to A$70.5 million due to higher nickel price and higher realised zinc and copper prices from the Jaguar operations. However, revenue at Tropicana decreased by 1% due to the cessation of grade streaming, which resulted in lower volumes offset by a higher average FY17 gold price. The company posted a $17.0 million net profit after tax against a loss of $58.8 million in FY16 led by higher realised base metal prices in Zinc (Up 69%), Copper (Up 15%), Nickel (Up 11) and Gold (Up 4%).However, higher cash flow from operating activities contributions from Tropicana, Long and Jaguar, was offset by payments of stamp duty taxes to the Western Australian State Government totalling A$58 million resulting in net cash flows from operating activities at A$78 million.

Net cash outflows from investing activities amounted to A$273.3 million for the year, primarily related to the continued construction and development of the Nova Operation, with net project capital expenditure amounting to A$165.6 million for FY17. Cash outflows from investing activities were lower than FY16 as that year included payment for the acquisition of Sirius (A$202.1 million, net of cash acquired). Other movements in cash outflows from investing activities include A$17.6 million net cash outflow for the takeover of Windward, A$14.6 million for the acquisition of property, plant and equipment, and A$13.4 million cash outflow in relation to capitalised borrowing costs on the syndicated debt facility.

.png)

Group Financial Summary; (Source: Company reports)

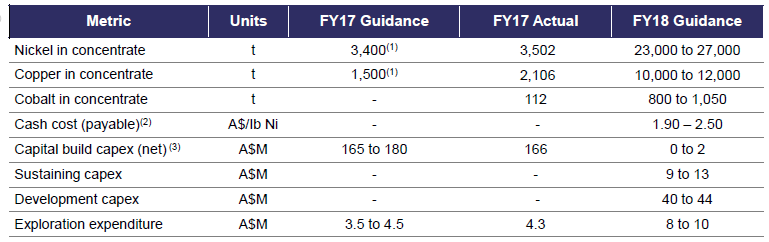

Ramp up of Nova mining activities: Significant progress was achieved during the year to advance the ramp up of Nova mining and processing activities towards the 1.5Mtpa nameplate production capacity, which is expected to be achieved in the September 2017 quarter. Further, underground mining from Tropicana Gold Mine is estimated to contribute to supplementary high-grade production from 2020.

FY17 operational scorecard and FY18 guidance; (Source: Company reports)

Given the ongoing progress at Tropicana Gold Mine and Ramp up of Nova mining activities, we maintain a “Buy” recommendation on the stock at the current market price of $ 3.53

.PNG)

IGO Daily chart; (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...