Reliance Worldwide Corporation Limited

Positive outlook for Reliance, with new chairman on-board:One-stop complete solution provider, Reliance Worldwide Corporation Limited (ASX: RWC) is a mid-cap company with the market capitalization of ~$3.63 Bn as of 15 March 2019. It recently released H1FY19 result where it reported an increase in its net sales by 50.1% on the PCP to $544.2 Mn. The core net sales excluding John Guest increase by 7.4% pcp to $389.4 Mn resultantly due to robust growth in underlying sales in the America segment. Mr. Stuart Crosby has been appointed as the New Chairman. He has been a non-executive director of RWC since April 2016.

Its adjusted EBITDA increased by 65% on the PCP basis to $130.8 Mn, however there was a decrease in adjusted EBITDA excluding John Guest by 3% pcp to $77.2 Mn. This was due to higher raw materials costs primarily Copper as compared to the previous period along with the negative impact of one-off supplier issues in the Americas.The Board of Directors declared an interim dividend (fully franked) worth $31.6 Mn at 4 cps with payment date on March 29, 2019 and record date on March 8, 2019.

.png)

1HFY19 Financial Metrics (Source: Company Reports)

What to Expect From RWC: The company expects its EBITDA in the range of $280 Mn to $290 Mn for FY 2019 which including the actual synergies which are anticipated to be realised in FY19 and excluding the one-off integration costs which are anticipated to be incurred. The company expects capital expenditure between $65 million and $75 million which includes the capital spending for John Guest of around $25 million and excludes $8 million which is related to non-recurring facility repair at Cullman.

Stock Recommendation:RWC’s share has generated positive YTD return of 3.60%. The company’s ROE stood at 4.9% in H1FY19 better than 3.5% in H2FY18. Taking into consideration of decent fundamentals along with positive outlook and its current price levels which is close to 52-week low level, we, therefore, recommend a “Buy” rating on the stock at the current market price of $4.600.

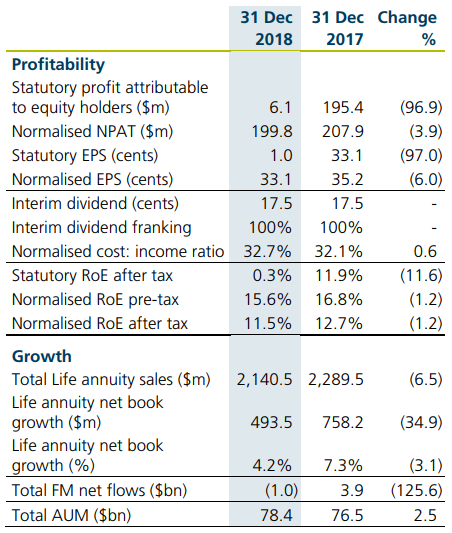

Challenger Limited

Increased interest in Vocus: An investment management mid-cap company, Challenger Limited (ASX: CGF), in its H1FY19 result reported an increase in its asset under management of 2% on pcp basis to $78.4 billion. The normalised net profit before tax decreased by 2% pcp to $270 Mn. The earnings were majorly impacted by volatility in the investment market (equity and fixed income) in the December quarter resulting in lower asset returns in the life businesses and lower funds management fees.

The company maintains excess regulatory capital and group cash at $1.4 Bn. The Board of Directors declared a fully franked interim dividend of 17.5 cps with payment date on March 26, 2019 and record date on February 27, 2019. In the recent update, CGF increased its interest in Vocus Group from 7.23% to 8.24%.

Profitability & Growth Metrics (Source: Company Reports)

What to Expect From CGF: The company, in H2FY19, will target new consumer brand campaign launch in mid-2019. It will add new Funds Management products including ActiveX Series.In its guidance for FY2019, normalised NPBT expectation has been reduced to $545 Mn to $565 Mn. It expects ROE to be below 18% in FY19. Its dividend payout ratio is expected to be in between 45% to 50% of normalised NPAT.

Stock Recommendation:CGF’s share has generated negative YTD return of -15.01%. The decent company’s guidance along with new launches in H2FY19 will boost the company earnings in the forthcoming years. Moreover, it reported a higher dividend yield of 4.57% as compared to the insurance industry median of 4.0% representing decent income for its shareholders. Hence, we recommend a “Buy” rating on the stock at the current market price of $7.760 per share.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...