Nufarm Limited

.png)

NUF Details

Decent FY19 Revenue Growth: Nufarm Limited (ASX: NUF) is engaged in the manufacturing and sale of crop protection products. As on 15 November 2019, the market capitalisation of the company stands at ~$2.33 billion. The company notified that its Annual General Meeting 2019 is to be held on 5 December 2019.The company has recently released its annual report for the year ended 31 July 2019, wherein it reported a rise in sales by 13.6% to $3,758 million as compared to $3,308 million in FY18.Underlying earnings before interest, tax, depreciation and amortisation (EBITDA) increased by 9% to $420 million, mainly due to a full-year contribution from the European portfolios and strong earnings in North America, Seed Technologies and Asia, offsetting a weaker performance in ANZ and flat earnings in Latin America. During the year, statutory net profit of year went up to $38 million on the prior year loss of $16 million. The company reduced the net debt with the support of equity raising in the first half of the year.

.png) |

Financial Performance Highlights (Source: Company Reports)

What to Expect: The company intends to divest the crop protection and seed treatment assets in South America for cash proceeds of $1.18 billion and customary net working capital adjustments, the completion of which is targeted in the first half of 2020. Nufarm Limited expects continued growth in sales, cost saving benefits and improvements in supply chain efficiencies to drive earnings growth in the remaining businesses in 2020. The company provided guidance for EBITDA in the range of $10 million to $15 million. Net interest expense is forecasted to be in between $105 million and $110 million in 2020, including an estimated $30 million of interest costs related to the South American businesses which is to be divested.

Valuation Methodology:Price to Earnings Multiple Approach:

P/E Valuation Multiple (Source: Thomson Reuters), NTM* Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: As per the ASX, the stock of Nufarm Limited generated returns of 34.87% and 39.46% in the past three and six months, respectively, but witnessed a decline of 7.38% in the last one month. The stock is currently trading close to its 52-week high of $6.940. EBITDA margin and net margin of the company stand at 11.5% and 1% as compared to the industry median of 12.4% and 4%, respectively. In terms of valuation, the stock of NUF is trading at a Price to Earnings multiple of 59.250x, higher than the industry median (Basic Materials) of 14.9x on TTM basis. Thus, considering the price movement in last three months, current trading levels, and valuation, we recommend a “Sell” rating on the stock at the current market price of $6.410, up 4.228% on 15 November 2019.

NUF Daily Technical Chart (Source: Thomson Reuters)

Crown Resorts Limited

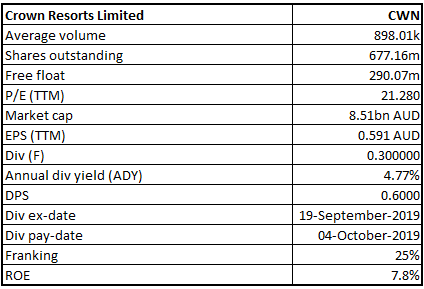

CWN Details

Completion of purchase of Queensbridge: Crown Resorts Limited (ASX: CWN) is one of the largest entertainment groups, with its core businesses and investments in the integrated resorts sector. The company has recently announced that it has completed the purchase of Schiavello Group’s 50% ownership interest in the One Queensbridge development site, as well as all pre-development assets. In the recently held Annual General Meeting of the company, the top management stated that the gaming revenue from the Australian resorts main floor, for the period starting 1 July to 20 October 2019, was up 2% on the prior corresponding period, whereas, non-gaming revenue was broadly flat.

Financial Highlights: For the full year ended 30 June 2019, CWN reported normalised EBITDA of $802.1 million, down 8.7% on the previous year and normalised net profit after tax (NPAT) of $368.6 million, down 4.7% on the previous year. This result reflected subdued market conditions, with a reduction in VIP program play revenue and continued softness in Perth, partly offset by modest revenue growth in Melbourne’s local businesses. At year end, Crown had net debt of $87 million leaving its balance sheet well placed to deliver on its major focus areas, including the construction of Crown Sydney.

Financial Performance (Source: Company Reports)

Stock Recommendation: The company stated that the podium structure of Crown Sydney is majorly completed and expects its opening in the first half of 2021, with net project cost expected to be about $1.4 billion. As per the ASX, the stock of CWN generated a return of 7.44% on YTD basis and a return of 3.88% in the last one month. EBITDA margin of the company stands at 29.9%, higher than the industry median of 25.6%, indicating stability in the business. Net margin of the company stands at 13.8% as compared to the industry median of 9.4%, implying that the company is capable to manage its costs effectively. Currently, the stock is trading at a price to earnings multiple of 21.280x with an annual dividend yield of 4.77%. Thus, considering the trading levels, positive returns, decent outlook and higher EBITDA and net margin than the industry, we recommend a “Hold” rating on the stock at the current market price of $12.680, up 0.875%, on 15 November 2019.

.jpg)

CWN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...