Incitec Pivot Limited

Result Highlights for FY19:Incitec Pivot Limited (ASX: IPL) manufactures and distributes industrial explosives, industrial chemicals and fertilisers. The company is also engaged in the provision of related services. The market capitalisation of the company stood at ~$5.67 billion as on 13th November 2019.

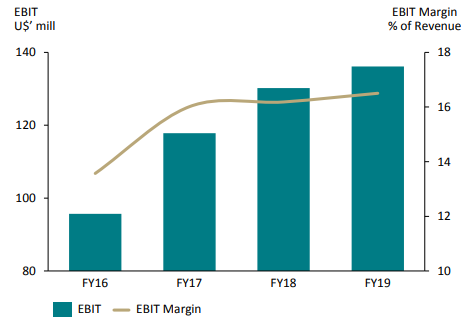

The company reported net profit after tax of $152 million for FY19 after $140 million of non-recurring items (net of tax). The company’s EBIT stood at $304 million, reflecting a fall of $253 million as compared to EBIT ex IMIs of $557 million in FY18.

The decrease in EBIT was mainly due to $197 million net adverse movement in non-recurring items. The company’s net debt increased by $320 million to $1.6 billion, mainly due to the lower operating cash flows of $248 million and the impact of lower A$:US$ exchange rate on translation of US$ borrowings as well as maturing debt hedges during the year. The company declared a final dividend of 3.4 cents per share, 30% franked. This makes a full-year dividend of 4.7 cents per share (cps), which implies a payout ratio of around 50%.

Explosives EBIT and Margin Growth (Source: Company Reports)

Outlook: The outlook for FY 2020 is based upon underlying assumption that FY 2019 non-recurring items, which amounted to $197 million in FY19, will not occur in FY 2020. The company’s explosives business is expected to deliver earnings growth in FY20, underpinned by stronger volumes and efficiencies.The Waggaman plant is expected to deliver improved production as compared to FY19 at slightly below nameplate capacity, with no planned outages scheduled for FY20.

In 2020, the demand for ammonium nitrate is expected to remain strong in Australia, however, sales volumes related to Moranbah in Australia are expected to be lower in 2020 after contract renewals. The effective tax rate is expected to come in between 25% and 28%.

Stock Recommendation: As per the ASX, the stock gained 6.97% in the past six months and 6.01% in the last one month. The company reported gross margins of 50.1% in FY19, which is above the industry median of 29.1%. Based on its EBIT performance in FY19, coupled with the aforesaid facts, gross margins, and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $3.490 per share, down 1.133% on 13th November 2019.

Fletcher Building Limited

NZICC Site Handed Back to Fletcher Construction:Fletcher Building Limited (ASX: FBU) is into the business of building products, distribution, laminates & panels, concrete, construction and steel. The market capitalisation of the company stood at ~$3.99 billion as on 13th November 2019.

Fletcher Buildings Limited has provided a further update on the fire that happened in the NZICC project, which was damaged by a significant fire that started on 22 October.It stated that Fletcher Construction staff has been working closely with fire and emergency services teams, local authorities, and SkyCity to handle the impact of fire. The NZICC site has now been handed back to Fletcher Construction, though access remains restricted as safety and structural assessments and investigations into the cause of the fire are completed. The company is working closely with the insurer for the contract works as well as third-party liability insurances, which are in place on the project.

Company Confirms Director Appointment: The Chairman of the company, Bruce Hassall announced the appointment of Peter Crowley as non-executive director of the company.Peter will bring wealth of leadership, commercial and operational experience from leading Australian building product companies that will enhance the Board experience.

Outlook for FY20: In FY20, the company expects ongoing favourable market conditions in New Zealand and Australia residential market contraction.In New Zealand market, the company expects residential consents to ease slightly off peaks and Auckland to remain strong. It is expected that commercial construction will remain in similar levels. In Australian market, residential sector is expected to contract, and it is forecasted that in FY20, 150k to 160k approvals will be there, however, the market environment remains uncertain. In Australia, commercial market is expected to remain broadly flat.

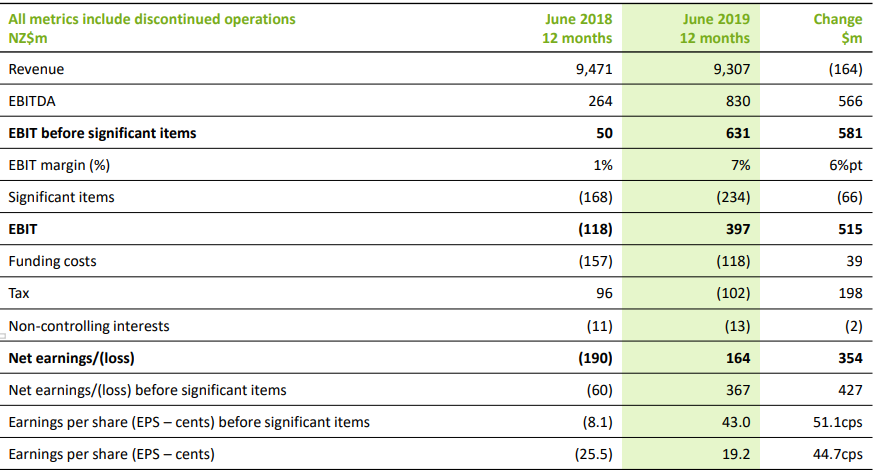

Income Statement (Source: Company Reports)

Stock Recommendation: The stock is trading at an EV/EBITDA multiple of 5.7x, which is below the industry average of 10.6x on TTM basis. This shows that the stock is trading below its peers. The company’s net margin stood at 3.1% as compared to the industry median of 10.2%. FBU is expected to conduct its AGM on November 27, 2019. Therefore, we advise investors to keep a close eye on its AGM and outcome as it might contain some important financial information in the form of outlook of the business. Based on the recent development, EV/EBITDA multiple and other financial parameters, we have a watch stance on the stock at the current market price of $4.820 per share, up 1.261% on 13th November 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...