Clinuvel Pharmaceuticals Limited

.png)

CUV Details

Decent Top-line and Bottom-line Performance for FY19:Clinuvel Pharmaceuticals Limited (ASX: CUV) is an Australia based biopharmaceutical company, devoted to the enhancement of treatments for skin diseases. Recently, the company informed the market about the submission of its application for its drug SCENESSE® (afamelanotide 16mg) to be registered in the Australian Register of Therapeutic Goods (ARTG). The application has been submitted to the Australian Therapeutic Goods Administration (TGA) for registration approval. Following registration, the drug will be made available to adult patients with erythropoietic protoporphyria (EPP) to prevent phototoxicity.

In another update, The Bank of New York Mellon Corporation and its entities, changed its substantial holding in the company from 10.74% to 9.73%, effective from December 6, 2019.

FY19 Key Highlights for the period ended June 30, 2019: Total revenue and other income for the period was reported at $32.50 million, an increase of 24% on a y-o-y basis. Profit after tax for the period was reported at $18.134 million, up from $13.224 million in prior corresponding year. During the period, the company reported an increase of 35.7% in earnings per share, which came in at 37.6 cents. Cash and cash equivalents at the end of the period was reported at $54.269 million. During the period, the Board of Directors declared an unfranked dividend of 25 cents per share.

.png)

FY19 Key Metrics (Source: Company Reports)

What to expect:As per the release, the company has its focus on developing and commercialising its drug SCENESSE® as a preventative therapy to photo-protect patients with EPP. Its active product development pipeline covers existing and new treatments for a range of skin related indications. The pipeline includes research and development into SCENESSE® for adult vitiligo patients; paediatric formulation of SCENESSE®; SCENESSE® for adult patients with VP; next generation products based on melanocortin analogues CUV9900 and VLRX001; and a range of over the counter products for the general photoprotective application. These developments are expected to help the company in delivering sustainable returns for its shareholders.

Valuation Methodology: EV/SalesMultiple Approach

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company has a market capitalisation of ~$1.43 billion and ~49.41 million outstanding shares. Currently, the stock is trading below the average of 52-week high and low of $45.880 and $17.770, respectively, proffering an opportunity for share accumulation. Its EBITDA margin and net margin for FY19 stood at 54.9% and 57.4%, better than the FY18 result of 48.5% and 51.4%, respectively, implying decent fundamentals for the company. Its current ratio for FY19 stood at 12.33x, higher than the industry median of 5.08x, which implies that the company is in a better position to address its short-term obligations. Debt to Equity ratio for FY19 stood at 0.01x, lower than the industry median of 0.19x. Considering the recent developments with respect to the key product SCENESSE®, strong cash position and decent outlook, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple approach and arrived at a target price of lower double-digit upside (in percentage term). Hence, we recommend a “Hold” rating on the stock at the current market price of $28.450, down 1.557% on 31 December 2019.

.jpg)

CUV Daily Technical Chart (Source: Thomson Reuters)

Pro Medicus Limited

.png)

PME Details

PME Enters into 5-year contract with Palo Alto based Nines:Pro Medicus Limited (ASX: PME) is primarily engaged in the supply of healthcare imaging software and services to hospitals, diagnostic imaging groups and other health related entities in Australia, North America and Europe.

Recently,the company informed the market that its wholly-owned U.S. subsidiary, Visage Imaging, Inc., has entered into a 5-year, multi-million-dollar contract with Palo Alto based Nines.Under the contract, Visage Imaging will provide Nines with an immensely scalable and highly optimised platform via its offering based on Visage 7 technology. This partnership is expected to give Visage Imaging an opportunity to support Nines’ efforts to develop future products with the highly optimised Visage 7 cloud-based solution for on-demand reads. Pro Medicus is expected to reap revenue in excess of AUD$6 Mn over the life of the contract with the potential for a significant upside.

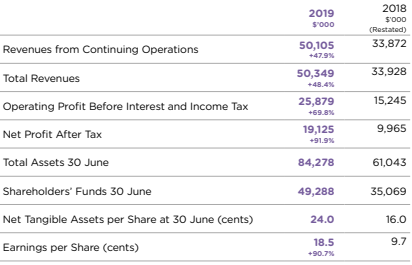

FY19 Key Highlights for the period ended June30, 2019: Revenue for the period was reported at $50.11 million, up 47.9% on prior corresponding year. This can be attributed to a 42.2% increase in revenue in North America, 102.3% in Europe and 30.2% in Australia. Net profit after tax (NPAT) for the period was reported at $19.13 million, up 91.9% on pcp. The company’s cash balance at the end of the period was reported at $32.3 Mn, with nil debt. The Board of Directors declared a final dividend of 4.5 cps.

FY19 Key Financial Metrics (Source: Company Reports)

What to expect:As per the release, the company is expected to showcase Visage AI Accelerator at the Radiological Society of North America (RSNA) 2019 meeting in Chicago. The product is a complete “end to end” platform for AI that entails the daily workflow of a radiologist. PME is also expected to showcase its new Breast Density algorithm that delivered promising results, depicting the potential for commercialisation and FDA approval. It has highlighted that the RSNA impacts three major customer groups in its pipeline and the company saw increased attendance and quality of personnel from all the three groups.

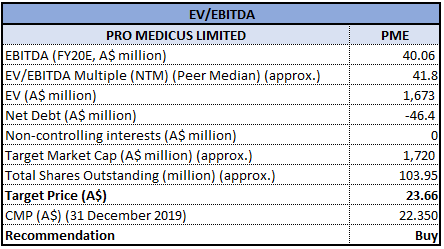

Valuation Methodology: EV/EBITDAMultiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock generated a whopping YTD return of 115.80% and is currently trading close to the average of its 52-week high and low level of $38.390 and $10.863, respectively. Its EBITDA margin and net margin improved from 58.3% and 29.4% in FY18 to 63.2% and 38.0% in FY19, respectively. In FY19, the company reported an improvement in profitability with a complete focus on its strategic plans. Moreover, the company is continuously investing on innovative products to position in the market. In the coming weeks, it will be showcasing its two specialities, i.e., Visage AI Accelerator and the Breast Density Algorithm at the RSNA 2019 meeting. Considering the above factors, we have valued the stock using EV/EBITDA multiplebased relative valuation method and arrived at a target price with single-digit upside (in % terms). Hence, we give a “Buy” rating on the stock at the current market price of $22.350, down 8.924% on 31 December 2019. The stock surged over 4% on December 30, 2019, on account of positive sentiments owing to the contract with Palo Alto based Nines.

PME Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...