Transurban Group

Transurban headed towards growth, driven by acquisition and robust numbers: Transurban Group (ASX: TCL) is one of the world’s largest toll-road operators. The company is into designing and building new roads, researching new vehicles and road safety technology. It is partnering with governments to address several safety and traffic challenges and is undertaking major development projects to create more efficient transport routes and ease congestion.

Key Highlights:

-

Financial close on the West Gate Tunnel (WGT) Project in Melbourne

-

-

Acquisition of the A25 toll road and bridge in Montreal, Canada

-

-

395 Express Lanes project reached financial close in the Greater Washington Area (GWA)

-

-

Retail tolling brand Linkt launched across Brisbane, Sydney and Melbourne

-

-

$4.8 billion of debt raised with minimal debt to be refinanced in FY19

-

-

$1.9 billion of equity raised from an entitlement offer

-

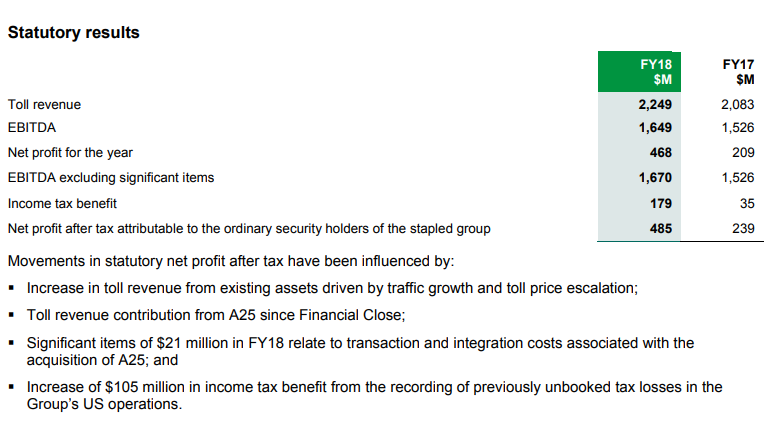

FY18 Statutory Results (Source: Company Reports)

The toll revenue increased by 8% Y-o-Y to $2,249 million, however the total revenue came in at $3,298 million for FY 2018 an increase of ~20% on Y-o-Y basis. The profit from ordinary activities after tax excluding significant items increased 134.3% to $489 million in FY 2018 as compared to the prior year. The current ratio of the company stood at 0.82x in FY18 which is broadly in-line with the industry median of 0.84x. The net CFO increased significantly in FY 2018 to $1,053 million, an increase of 25%. The company acquired 100% of A25 concession (the entities that holds a 7.2 km project connecting Northern Montreal across the Riviere Des Prairies to commercial and residential areas), which resulted in an increasing CFI as well for FY 2018. The company’s borrowings decreased by almost 70% in FY 2018 Y-o-Y resulting to a decrease in net finance cost as well. Moreover, the total assets increased by almost 13% Y-O-Y. The free cash marginally decreased 0.5% to $1,215 million in FY 2018. The company maintained its account receivable turnover ratio of 12.5x in FY18 which is higher than the industry average of 5.9x, signifying robust collection policy. Based on robust performance in FY18, RoE and RoIC substantially increased from 5.0% and 1.0% to 10.1% and 2.3%, respectively over the prior year. Hence, we presume that FY18 was the successful year for the company and is now well positioned to deliver sustainable shareholder returns in the upcoming period.

Meanwhile, the share price has risen 3.10% in the past three months as at December 24, 2018 and is trading above the average of 52-week High and Low level. However, the outlook for TCL looks positive, since the company has posted robust growth and performed well over the past few years. Driven by strong growth in revenues, margins, and operating cash flow and closed multiple deals during the year, TCL gained ample opportunities to grow further. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $11.870 (up 1.976% on December 27, 2018).

Boral Limited

Uptick in Revenue Driven by Strong Sales in Australia and North America: Boral is an Australia-based building products and construction material group. It operates through its three segments which includes Boral Australia, USG Boral, and Boral North America. The company offers infrastructure and commercial building solution along with providing a wide range of products and services required for construction.

Robust Strategies:

• Long-term sustainability and value creation.

• The company has fundamentally altered its portfolio to deliver better financial returns.

• They have been shifting away from energy and resource-intensive, high fixed cost manufacturing to lightweight, innovative and more variable cost building products and materials.

• The massive transformation over the past five years was driven by consolidations, joint ventures, divestitures, plant closures, innovations, and acquisitions.

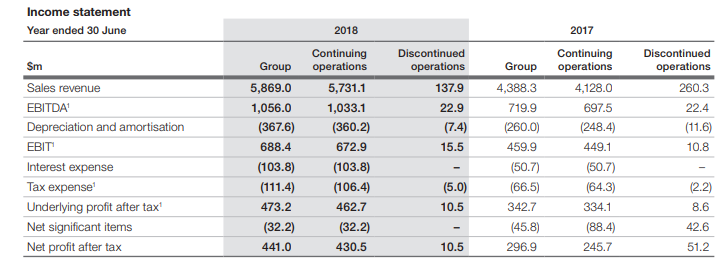

Financial Performance (Source: Company Reports)

In FY18, EBITDA stood at $1.06 billion with EBITDA margins of 18.0%, representing a significant rise of ~46.8% and 161 bps, respectively over the prior year.The revenue of the company came in at $5.87 billion, up 34% on the prior year, with growth in Boral Australia and Boral North America. The underlying profit after tax was $473.2 million, an increase of 38% Y-O-Y. This improvement was driven by a 50% increase in EBIT, offset by higher interest and tax expense. Capital expenditure stood at $425 million in FY2018 increase of $85 million higher Y-O-Y, reflecting increased capital expenditure in North America following the acquisition of Headwaters. Operating cash flow increased by $165 million to $578 million in FY2018, because of improved earnings offset by higher interest and tax payments and an adverse working capital movement. The net debts increased primarily due to the impact of unfavourable exchange rates, and net cash outflow of $54 million. Among the key ratios, current ratio and asset turnover increased significantly. ROE, however, grew by 160 bps to 7.1% in FY18 which is marginally down from the industry median of 8.3%.

Meanwhile, the share price has fallen 31.28% in the past three months as at December 24, 2018 and is trading at reasonable PE multiple of 12.730x. Based on strong fundamentals along with strategic acquisition with Headwaters and focuses on cost optimization strategy, we believe that the company has a decent outlook ahead. Hence, we maintain our “Buy” recommendation on the stock at the current market price if $4.880 (1.897% on December 27, 2018).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...