The a2 Milk Company Limited

.png)

A2M Details

Extended Agreement with Synlait: The a2 Milk Company Limited (ASX: A2M) is a premium branded dairy nutritional company, focused on products containing A2 beta-casein protein type. As on 2nd January 2020, the market capitalisation of the company stood at $10.52 billion. Geoffrey Babidge has agreed to take the position of Interim CEO with effect from 9th December 2019 at fixed remuneration of AUD 1,600,000 per annum. Recently, Synlait Milk Limited renegotiated certain aspects of the comprehensive manufacturing and supply arrangements with the Company. The release stated that changes reinforce long-term partnership of both the companies.

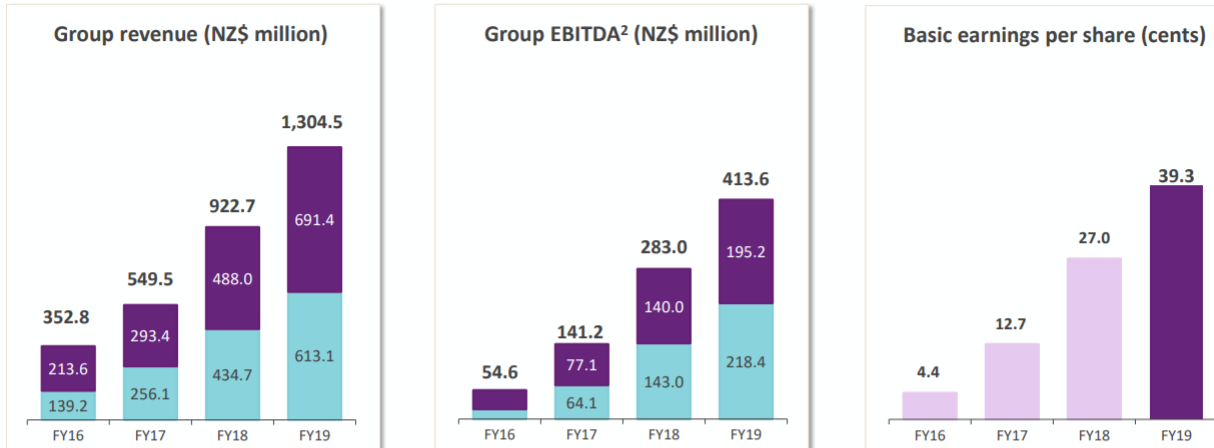

Substantial Rise in Revenue and EBITDA: During FY19, the revenue of the company stood at NZ$1.3 billion, up by 41% from NZ$922.7 million in FY18. During the same time span, EBITDA of the company went up to NZ$413.6 million from NZ$283 million. This resulted basic earnings per share to increase to 39.3 cents, up from 27 cents per share.

Financial Performance (Source: Company Reports)

Growth Opportunities: The company has re-affirmed its outlook and expects a stronger full-year EBITDA margin in the range of 29% - 30%. Gross margin is expected to benefit from improved price yield and reduction in Costs of goods sold (or COGS).

The company also expects 1H20 revenue to be in between $780 million to $800 million. The company is progressing well for key new product innovations and expects more product launches in the second half of FY20. It also anticipates distribution to grow by approximately 2000 stores in the first half. For FY 2020, A2M also anticipates strong growth in revenue across the key regions supported by brand and marketing investment in China and the US, as well as the development of capability and infrastructure in order to help in-market execution.

Valuation Methodology: Price/Earnings Multiple Approach

.png)

Price/Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: As per ASX, the stock of A2M gave a return of 37.50% on YTD basis and a return of 15.04% in the past 3 months. In the time span of 4 years from FY15 to FY19, the company witnessed a CAGR of 70.37% in revenue and a CAGR of 90.32% in gross profit. During FY19, net margin of the company stood at 22.1%, higher than the industry median of 7.3%. This indicates that the company is managing its costs well and is capable to convert its revenue into profits. The company’s Return on Equity during FY 2019 was 42.8% as compared to the industry median of 13.1%. Considering the returns, decent outlook, CAGR in revenue and gross profit, and high net margin and RoE, we have valued the stock using P/E based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $14.020, down by 1.958% on January 02, 2020.

A2M Daily Technical Chart (Source: Thomson Reuters)

Wattle Health Australia Limited

WHA Details

Rights Issue Offer and B&P Transaction: Wattle Health Australia Limited (ASX: WHA) is a food and beverage company. The company has recently announced that it was unable to secure the full amount of $55 million funding, which was required as a minimum offer amount under its prospectus. It was stated that, pursuant to the rights issue prospectus, WHA received approximately $11.6 million from existing eligible shareholders. This resulted in the lapse of the underwriting agreement with Claymore Capital Pty Ltd on 31st December 2019.

However, the company and Mason Financial Holdings have agreed to extend the sunset date of the proposed transaction to acquire 75% of Blend and Pack from 31st December 2019 to 7th January 2020.The extension would allow WHA and Mason to further negotiate on a potential amended proposal in light of circumstances arising from the outcome of the rights issue offer.

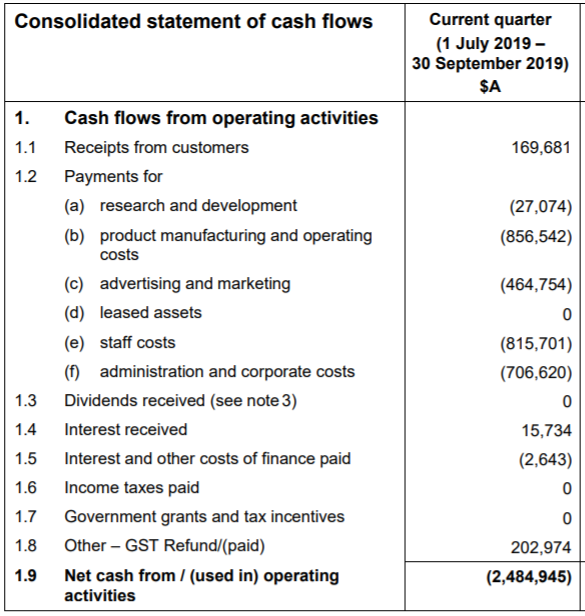

Strong Balance Sheet: Forthe quarter ended September 2019, WHA reported a strong balance sheet with cash at bank of approximately $18.5 million and zero debt.In the same time span, the company reported lower sales due to delay in the production of Uganic. There were higher production and manufacturing costs due to brand redesign and relaunch of Little Innoscents across numerous distribution channels.

Cash Flow from Operating Activities (Source: Company Reports)

Future Opportunities: The construction of the joint venture Corio Bay Dairy Facility is on track and is under budget for the start-up of operations in the first half of 2020. The company has also launched its premium brand Uganic in September after conducting extensive research and planning, and the early signs are positive. The company will continue to take up opportunities for sales of its recently manufactured organic nutritional dairy products in domestic and overseas markets, mainly China. WHA stock was under suspension and traded at $ 0.472 as at September 27, 2019.

WHA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...