Stocks’ Details

G8 Education Ltd

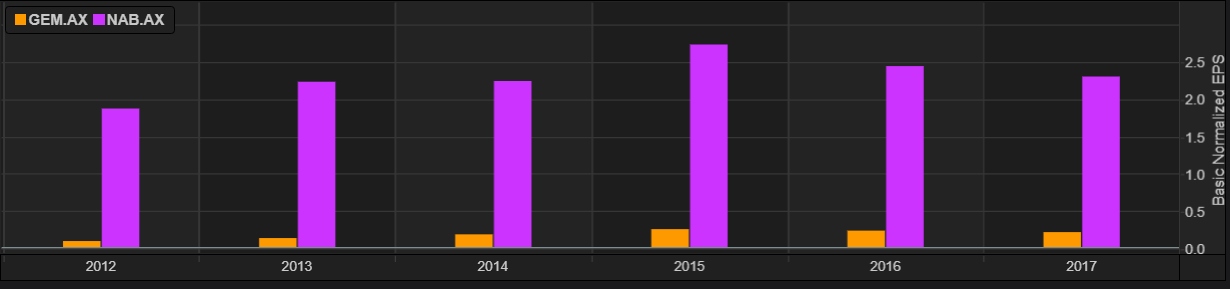

Decent pipeline and an improved outlook: G8 Education Ltd.’s (ASX: GEM) stock has risen 20.64% in three months as on July 27, 2018. There is speculation that the company may be a takeover target in the Australian private equity industry and this has been behind the latest boost in stock price. It is worth noting that the childcare centre market in Australia has big influence from private equity owners at the back of government support and the position to have cost savings in terms of operating the centres for profit. Meanwhile, the industry is highly fragmented, and given that GEM has set an attractive pipeline of 40 centres for the next 2 years, the opportunities look decent. Further, the expectations that the occupancy level will recover now seem to be falling in place. Moreover, so far in 2018, supply environment has remained challenging, with LFL occupancy down circa 2.5 to 3%. GEM had earlier flagged to have earnings per share (EPS) target of 40 cents per share by 31 December 2019. However, due to the prevailing market environment and impact on occupancy, this target did not look achievable. GEM is however, confident that the market environment will once again become favourable given the funding related regulatory changes slated from July 2018 and will deliver significant growth for shareholders. Meanwhile, GEM is trading at a reasonable P/E of 13.90x. Lately, FIL Ltd and entities enhanced the interest in GEM to 7.4% from 6.3%. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.560.

National Australia Bank Ltd.

NAB expects costs savings of ~$300m for FY 18: National Australia Bank Ltd.’s (ASX: NAB) stock has risen 4.07% in one month as on July 27, 2018. NAB has lately named Geoff Lloyd as the CEO of retirement fund manager MLC, which is the bank’s retirement fund manager. NAB might demerge and float MLC, or may seek any prospective sale opportunity by the end of 2019. On the other hand, NAB will stop charging farmers extra for defaulting of loans in droughts, after a major inquiry was conducted on lender’s way of managing rural borrowers given the dry weather adversity hovering over the country. Now, farmers will be allowed to access money at discounted interest rates; and this move by NAB is a part of strategy to tighten lending and reform their own practices ahead of expected recommendations for stricter regulation of the sector. Moreover, for FY 18, NAB expects costs savings of ~$300m and more than $1.0bn cost savings by FY20. FY18 expense growth is expected to be 5-8%, excluding restructuring costs and large one-off expense. The bank expects to achieve APRA’s ‘Unquestionably Strong’ CET1 ratio benchmark of 10.5% by January 2020 in an orderly manner, with accommodation of APRA’s proposed revisions to RWAs (risk weighted assets). NAB’s leverage ratio is of 5.6% on APRA basis. Further, NAB aims to achieve FY18 dividend at the FY17 level, however this will be subject to no material change to external environment and satisfactory group performance. Meanwhile, NAB is trading at a reasonable P/E of 14.59x. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 28.310.

Basic Normalised EPS (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...