Medical Developments International Limited

.png)

MVP Details

Revenues up 14.4% Year Over Year: Medical Developments International Limited (ASX: MVP) is in the business of pharmaceutical drug, medical and veterinary equipment. The market capitalisation of the company stood at $527.61 million as on 19 June 2020. In a recent update, the company stated that Bank of America Corporation and its related bodies corporate, became a substantial holder of the company, with a voting power of 5.11%. In another update, the company stated that Regal Funds Management Pty Ltd, a substantial holder of the company, hasdecreased its voting power from 7.12% to 6.05%. Also, the company informed the market that it has appointed Christine Emmanuel as a Non-Executive Director of the company, effective immediately.

Approval Received for Penthrox®: Recently, the company announced that it has received approval for the sale of Penthrox in Hungary. Penthrox® is used for emergency relief of mild to serious pain in sensible adult patients with shock and associated pain.Previously, the company has received approval for Penthrox® in The Netherlands and Bosnia & Herzegovina and Thailand.

Significant Growth in Revenue and Profit: The company has recently released its half-year results for the period ending 31 December 2019, wherein it reported an increase of 14.4% in revenue to $10.8 million and a growth of 81.8% in net profit after tax of $240k. This resulted in an increase in EPS by 76.2% to 0.37 cents. The decent financial and operational performance of the company enabled the Board to declare a fully franked interim dividend of 2 cents per share.

.png)

Key Financials (Source: Company Reports)

Future Expectations and Growth Opportunities: The company expects to roll out Penthrox® in remaining European Union countries, Mexico, Iran, Jordan, and South Korea. Over the next few years, the company will advance its manufacturing processes and is expected to deliver strong growth.

Risk Analysis: The company’s financial instruments comprise mainly of receivables, payables, bank loans and overdrafts, finance leases, loans from related parties, cash, and short-term deposits. The main risks MVP is exposed to through its financial instruments are foreign currency risk, interest rate risk, liquidity risk and credit risk.

Stock Recommendation: As per ASX, the stock of MVP gave a return of 8.94% in the past six months and is trading above the average of its 52-weeks’ low and high level of $3.760 and $11.78, respectively. Current ratio of the company stood at 3.74x in 1H FY20 as compared to the industry median of 1.69x. This implies that MVP is in a decent position to address its short-term obligations against the broader industry. Debt to equity of the company stood at 0.08x in 1H FY20, which is lower than the industry median of 0.18x. Hence, considering recent approval for Penthrox®, decent liquidity position and deleveraged balance sheet, we give a “Hold” recommendation on the stock at the current market price of $8.18 per share, up by 1.741% on 19 June 2020.

MVP Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

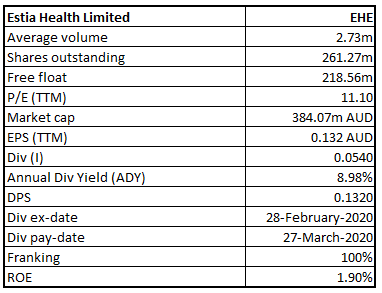

Estia Health Limited

EHE Details

EHE Suspends FY20 Guidance: Estia Health Limited (ASX: EHE) is engaged in the provision of services in residential aged care homes in Australia. Recently, the company stated that Vinva Investment Management became a substantial shareholder of the company, with a voting power of 5.04%. Another key update was regarding the suspension of FY20 guidance due to rising uncertainty because of COVID-19. The company is continuously monitoring the situation and has not reported any material impact among its residents or employees so far.

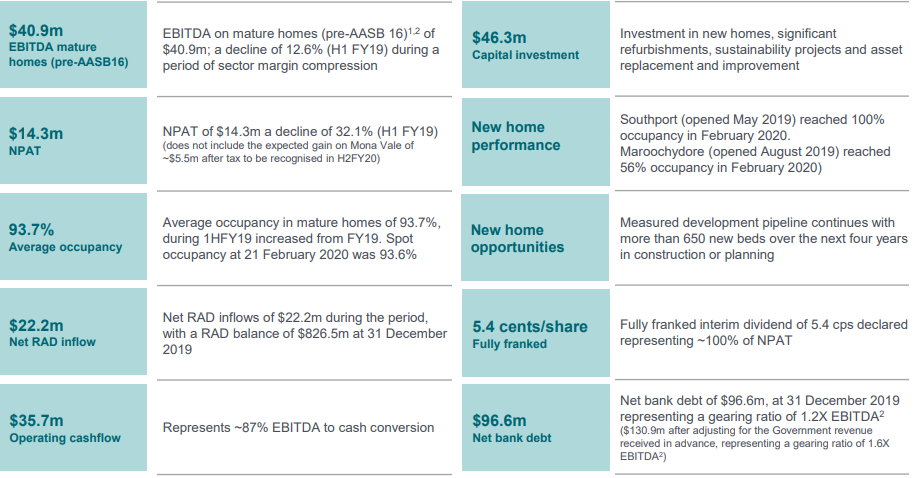

1HFY20 Results: During the half year ended 31st December 2019, the company reported a profit after tax amounting to $14.3 million amid sector-based challenges, reflecting the quality of services provided. The company was focused on increasing its market share and reported occupancy levels higher than the industry averages. The company follows a disciplined approach to cost management while investing in new capacity and making appropriate divestments.

Performance Highlights (Source: Company Reports)

What Investors Needs to Know: The company remains on track to accommodate new quality standards, with increased investment in resident amenity as well as improvements in quality and safety systems. It continues to improve its strategy and focus related to occupancy, which would become even more vital in an environment of increased competition and heightened consumer expectations. Further, Estia Health Limited would be carrying out activities that will support it in the refurbishment as well as execution of expansion plans for the existing homes. However, failure to protect and provide security to customers’ data, increased government regulation and supply chain risk are potential headwinds.

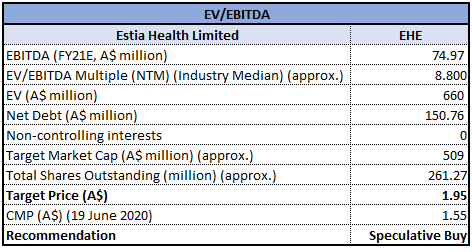

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

EV/EBITDA Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 41.67% over a period of 6 months and is currently trading below the average of its 52-week low and high level of $0.905 and $2.930. During 1HFY20, the company reported decent financial performance while continuously expanding its portfolio through the refurbishment program and the greenfield project for additional capacity. We have valued the stock using an EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of 1.55, up 5.442% on 19th June 2020.

EHE Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...