Viva Energy Group Limited

Decent Increase in Total Volumes: Viva Energy Group Limited (ASX: VEA) is engaged in manufacturing, distribution and supply of petroleum products to retail and commercial customers. As on 11th December 2019, the market capitalisation of the company stood at $3.76 billion.

For the quarter ended 30th September 2019, the company reported the actual GRM (or Geelong Refining Margin) for 3Q2019at US$8.8/Barrel with refining intake of 9.7MBBLs. The GRM for 3Q2019 includes the effect of higher crude premiums and the planned maintenance of the Platformer. The company also announced that it has received final regulatory approval to acquire the remaining 50% interest in wholesale business of Liberty Oil.

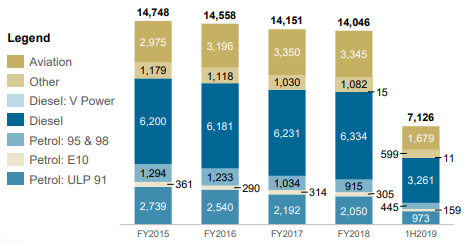

During the first half of 2019, total volumes stood at 7,126 million litres, up by 2.5% over 1H2018 volume of 6,955 million litres. During the period between 2015 to 2018, the total market volume growth was driven by diesel and aviation, partially offset by decreased demand for gasoline.

VEA volumes sold by product (Source: Company Reports)

What to Expect: The company has recently released its unaudited financial guidance for the year ending 31 December 2019 wherein it expects sales volumes for FY2019 to increase by around 4.3% and lie in between 14,600 to 14,700 million litres. This was mainly due to restoration of growth in the retail Alliance channel, continued growth in the Liberty and wholesale businesses, and strong sales performance in commercial segments. It also expects the total group underlying EBITDA (RC) to be in around $625 million to $655 million.

Valuation Methodology:

P/E Based Valuation:

.png)

P/E Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock of VEA gave a return of 10.89% on the YTD basis but a negative return of 1.28% in the past 3 months. In the time span of 4 years from FY14 to FY18, the company witnessed a CAGR of 27.29% in total revenue. During the year, gross margin witnessed an improvement 9% in 1HFY19 from 8.1% in 1HFY18. EBITDA margin also went up to 3.8% in 1HFY19 from 2.9% in 1HFY18. This indicates that the company is efficiently managing its costs and capable of generating respectable return ratios. Thus, considering trading levels, CAGR in revenue and improvement in gross margin and EBITDA margin, we have valued the company using relative valuation method (P/E valuation multiple), and arrived at the target price which is giving an upside of mid-single-digit (in percentage terms). Taking the backdrop of above factors, we recommend a “Buy” rating on the stock at the current market price of $1.995 per share, up by 3.101% on December 11, 2019.

Senex Energy Limited

Senex and Orora Long-Term Gas Sales Agreement: Senex Energy Limited (ASX: SXY) is engaged in oil and gas exploration and production. As on 11th December 2019, the market capitalisation of the company stood at $487.78 million.

The company has recently announced an expansion plan of its natural gas sales agreement with Orora Limited, wherein it has agreed to supply 13.2 petajoules of natural gas from Project Atlas over six years period from 2022 to 2027. This brings the total contracted volume under this gas sales agreement to 13.2 PJ.The company also announced that Project Atlas has achieved its first gas sales into the east coast market to Queensland power generator CleanCo.

Increase in Production and Sales Volume: During the quarter ended 30 September 2019, production went up by 9% to 337 kboe as a result of strong oil production from the Growler field and a material increase in Surat Basin gas production. Sales revenue of $23.9 million witnessed a marginal rise of 2% on Q-o-Q basis against prior quarter revenue of $23.5 million. The net sales volumes stood at 319 kboe in Q1 FY 2020, which was up by 6% than the prior quarter. During the year, reported NPAT went up to $3.3 million from a loss of $94 million in FY18.

Financial Performance (Source: Company Reports)

What to Expect: The company expects to bring new wells online and ramp up production towards its initial target of 18 petajoules a year, which is expected to reach by the end of the FY2021. In the upcoming year, the company will start to reap the rewards of the execution of its strategy as its partner Jemena completes construction of the Project Atlas processing facility and pipeline. SXY will focus on core assets with a strict capital allocation framework centred on disciplined investment and production growth both in the near and longer-term.

Valuation Methodology: EV/Sales Valuation Multiple

EV/Sales Valuation Multiple (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: During the year, gross margin of the company stood at 56.1%, higher than the industry median of 44.3%. Current ratio of the company was 3.61x as compared to the industry median of 1.21x.This indicates that the company is sufficiently liquid and is capable to pay its liabilities and fund its growth plans, using its current assets. As per ASX, the stock of SXY gave a return of 11.67% in the past 6 months but a negative return of 4.29% in the past one month. We have applied EV/Sales Valuation multiple and have arrived at the target price, which is offering a target price of lower double digit (in percentage terms).Considering the high gross margin, current ratio, decent outlook, and favourable valuation metrics, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.350 per share, up by 4.478% on December 11,2019, owing to the extension in agreement with Orora Limited.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...