Bank of Queensland Limited

Completion of Capital Raising to Strengthen Balance Sheet:Bank of Queensland Limited (ASX: BOQ) is one of Australia's leading regional banks with more than 180 branches across Australia. On 30 December 2019, BOQ announced the successful completion of the Share Purchase Plan (under the SPP), which is a part of BOQ’s fully underwritten $250 million institutional placement. Under the SPP, BOQ raised around $89.7 million, with approximately 12.3 million ordinary shares to be issued on 2 January 2020 and to commence trading on ASX on 3 January 2020. It is expected that the capital raising will help the bank in improving its financial strength by further strengthening the balance sheet. In addition to this, the capital raising will create additional capacity for the bank to implement its strategic priorities.

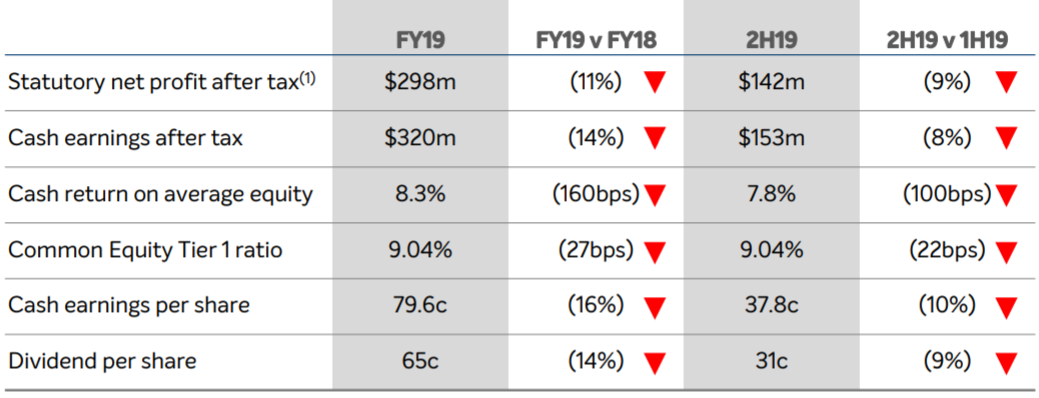

Key Highlights of FY19 Results:FY19 proved to be a challenging year for the bank. As a result, BOQ’s statutory net profit after tax and cash earnings after tax declined by 11% and 14%, respectively, as compared to the previous year. For the full year 2019, BOQ declared a dividend per share of 65 cents, which is 14% lesser than last year. BOQ currently has an annual dividend yield of 8.81%.

FY19 Results Summary (Source: Company Reports)

Outlook:BOQ anticipates FY20 to be a difficult year with lower year-on-year cash earnings, higher post-Hayne regulatory and compliance costs. In FY20, the company also expects to incur increased operating expenses due to investment in technology.

BOQ Recognizes Areas that require Attention:In order to return to profitability, BOQ has recognized areas, which require attention so that it could improve its overall performance. BOQ is focussed on turning around the retail bank’s performance, fixing its onerous lending processes, addressing its rising costs, and closing the digital gap between itself and its peers. BOQ also intends to improve its data platforms as well as building on its people’s skills and capability, particularly when it comes to execution.

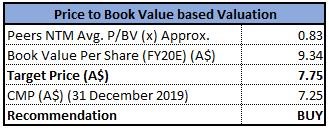

Valuation Methodology:Price to Book value Multiple Approach

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: In the last six months, BOQ’s stock price has declined by 22.4% and is currently trading near to its 52-week low of $7.110. We have valued the stock using Price to Book Value based relative valuation method and arrived at a target price of single-digit upside (in % terms). Considering BOQ’s current trading levels, its recent capital raising and valuation, we recommend a “Buy” rating on the stock at the current market price of $7.250, down by 1.762% on 31st December 2019.

Boral Limited

Q1FY20 Trading Update:Boral Limited (ASX: BLD) is a construction material and building supplier, operating three key divisions: Boral North America; USG Boral; and Boral Australia. In the first quarter of FY2020 or quarter ending 30 September 2019, Boral witnessed a slight decline in the earnings of all its three divisions. On the one hand, Boral Australia earnings were affected by the softer housing market and delays in infrastructure projects, and on the other hand, USG Boral earnings were impacted by the slowdown in residential construction in Australia and continued downturn in South Korea.

Steady Dividends:In FY19 or year ended 30 June 2019, Boral Group witnessed a 4% rise in revenue and a 2% rise in EBITDA. During the year, the company delivered USD 32 million of synergies from the Headwaters acquisition and is on track to achieve its four-year synergy target of USD 115 million in FY21. Boral paid a final dividend of 13.5 cents per share cps, taking the full-year dividend for FY19 to 26.5 cents per share, in line with FY18.

.png)

FY19 Results Summary (Source: Company Reports)

Guidance FY2020:Boral recently affirmed its FY20 guidance provided in August 2019. The company anticipates its FY20 NPAT (before significant items) to be around 5% to 15% lower than FY19, due to higher depreciation charges and reduced earnings. Further, the group expects its Property earnings to be in the range of $55 million-$65 million. The group expects its EBITDA in the first half of FY2020 to be around 5% lower than the prior year and EBITDA in the second half to be broadly similar to the reported second-half EBITDA last year. In Boral Australia, the company expects several major projects to ramp up in the second half and in Boral North America both volume and price growth is anticipated to improve the second-half earnings.

Recent Update:The company recently identified certain financial irregularities in its North American Windows business, due to which it is undertaking a comprehensive and urgent investigation and implementing immediate steps to bolster the management and controls within this business.

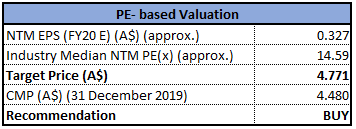

Valuation Methodology:Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: In the last six months, BLD’s stock price has declined by 11.28%. The stock is currently trading on the lower band of its 52-weeks trading range of $3.930 - $5.735. We have valued the stock using PE based relative valuation method and arrived at a target price of single-digit upside (in % terms). Considering the BLD’s expecting earnings growth in H1FY20, current trading levels and valuation, we recommend a “Buy” rating on the stock at the current market price of $4.480, down by 1.754% on 31st December 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.opriate for your personal financial situation, with a professional licensed financial planner and adviser.

AU

AU

Please wait processing your request...

Please wait processing your request...