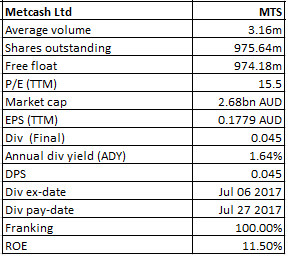

Metcash Ltd

MTS Details

Growth in all business segments in the first half of FY18: Metcash Ltd (ASX: MTS) stock rose over 9.6% on December 04, 2017 after the company reported for strong first half of FY 18 results. MTS in the first half of FY 18 has reported 7.6% growth in the sales revenue (including the acquisition of HTH) to $7.06bn and 24% growth in the reported profit after tax to $92.9m. The Group EBIT grew 18.7% to $152.0m in 1H FY 18. The Group EBIT includes the earnings from HTH (1H17: nil), growth in the underlying Hardware business, growth in Liquor and an increase in earnings from the Food Pillar. Moreover, MTS has reduced the Group debt by $94.8m and the average net debt for 1H18 is approximately $280m compared to approximately $375m in 1H17. The Group operating cash flow is of $161.4m in 1H FY 18 due to the cash generation across the pillars, tight working capital management and settlement of the Huntingwood DC insurance claim compared to $130.6m in 1H17. In 2H FY 18, there is some uncertainty over the impact of the recently introduced Container Deposit Scheme in NSW, and the roll out to other states for Liquor division. In FY 18, the Hardware business is expected to deliver between $20–$25 million of annualised gross synergies from the acquisition of HTH. In Food division, the external headwinds including intense competition, specifically in South Australia and Western Australia are continuing.

MTS will now pay FY18 interim dividend of 6.0 cents per share, fully franked. On the other hand, Group CEO will be stepping down and shortly be handing over to Jeff Adams. Meanwhile, MTS stock has fallen 0.36% in three months with a 31% rise in last six months, as on December 01, 2017, and is trading at a slightly high level. We give an “Expensive” recommendation on the stock at the current price of $3.00, and would wait and watch for any dip.

1H FY 18 Financial Performance (Source: Company Reports)

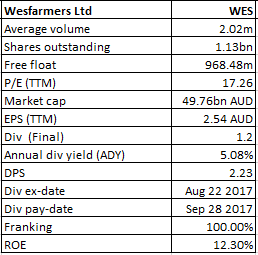

Wesfarmers Ltd

WES Details

Short term profit is limited: Wesfarmers Ltd (ASX: WES) is expecting margin pressures for Coles to continue in the short term as investments in the customer offer are not expected to be fully offset by simplicity benefits. The losses are expected to increase in FY 18 as trading remains challenging for Homebase and as the company progresses with the conversion from Homebase to Bunnings. The earnings for the Resources businesses are expected to be affected by lower coal prices and higher obligations to Stanwell resulting from higher coal prices in FY 17. As per the first quarter of FY 18, headline food and liquor sales for the first quarter were up 1.5% while total Coles Express sales, including fuel, for the quarter slipped by 9.5% over prior corresponding period. Meanwhile, WES stock has risen 3.42% in last three months as on December 01, 2017 and is trading at a high level. Based on the shortcomings, we maintain an “Expensive” recommendation on the stock at the current price of $43.92

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...