ResMed Inc

ResMed Settles Patent Dispute with Fisher & Paykel: ResMed Inc (ASX: RMD) and Fisher & Paykel Healthcare had made an announcement about an agreement to settle all the outstanding patent infringement disputes between the companies in all venues around the world.The settlement involves no payment or admission of liability by eitherside, and each party will bear its own attorney fees and costs incurred in the global proceedings.This will help ResMed to focus more on delivering the best services to its customers and value to its shareholders.

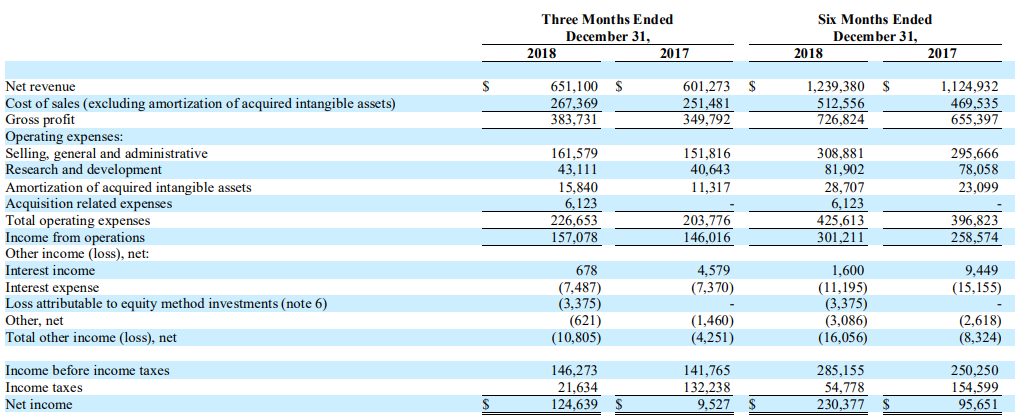

In its financial report release, it reported an increase in its net revenue by 8.3% pcp to US$651.1 million in Q2FY19, and by 10.17% pcp to US$1.23 billion in H1FY19. This can be attributed to the increase in revenues from all the product & service segments such as devices, masks & other, total sleep and respiratory care, and software as a service.

The board of directors announced unfranked dividend/distribution on security “RMD - CDI 10:1 FOREIGN EXEMPT NYSE” of USD 0.037 and payment date was March 14, 2019 and record date was February 7, 2019. A 30% of the withholding tax rate would be applicable to the dividend/distribution.

Q2 & H1 FY19 P&L Statement (US$ 000’) (Source: Company Reports)

What to expect from the company: ResMed has completed the acquisition of MatrixCare, a leader in software solutions. The company completed the acquisition of assets in Apacheta and has announced a joint venture with Verily.

It has also announced the acquisition of Propeller Health which happens to be a digital therapeutics company giving connected health solutions for people living with chronic obstructive pulmonary disease and asthma. The company is expected to be helped by these recent developments moving forward.

Stock Recommendation:ResMed’s share generated positive 1 year return of 12.40%. Also, from the valuations perspective, the company’s stock seems to be undervalued which represents a decent opportunity to buy. The company’s P/B ratio stood at 0.7x which is lower than the industry median (Healthcare equipment & supplies) of 3.6x.

As a result, we give a “Buy” rating on the stock at the current market price of A$14.410 per share (up 0.628% on 28 March 2019).

Treasury Wine Estates Limited

Decent Top-Line & Bottom-Line growth in 1HFY19: Large-Cap company, Treasury Wines Estates Limited (ASX: TWE) is involved in wine production and wine selling within Australia and New Zealand. Its wine portfolio includes Commercial, Masstige, and Luxury wine brands.

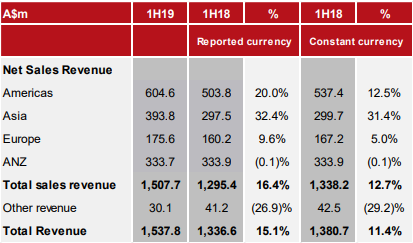

In its interim result for FY2019, it reported an increase in its net sales revenue by 16.4% pcp to $1507.7 Mn in H1FY19 on reported currency basis. It was majorly driven by a 1.4% increase in volume, portfolio premiumisation and price realisation on Luxury and Masstige wine.Its EBITS increased by 19.4% pcp to $338.3 Mn, driven by TWE’s premiumisation, continued strong momentum in Asia and above category growth in ANZ. The company declared an interim dividend of 18.0 cents per share (fully franked). The payment date for the dividend is April 05, 2019.

Region-wise Sales Metrics (Source: Company Reports)

What to expect from the company: The company has reiterated its guidance of around 25% reported EBITS growth in FY19, with a balanced earnings outcome across the fiscal year to reflect the even phasing of Luxury shipments between H1FY19 and H2FY19. It expects growth in FY20 reported EBITS in the range of around 15% to 20% broadly in line with consensus.

Its maintenance and replacement capex expected to be in line with guidance, in the range of $130 Mn to $140 Mn (including oak barrels) for FY 2019.

Stock Recommendation: Treasury Wine’s share has generated a positive YTD return of 1.91%. Its EBITDA margin and Net margin stood at 23.8% and 14.3%, respectively at the end of December 2018 which are better than the industry median of 22.1% and 12.2%, respectively which indicates decent fundamentals of the company. Its current ratio for the same period stood at 2.55x better than the industry median of 1.52x which implies the better liquidity position of the company to address its short-term obligations, as compared to its peer group. Hence, we recommend a “Buy” rating on the stock at the current market price of $14.930 per share (down 0.201% on 28 March 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...