Cleanaway Waste Management Limited

Acquisition of SKM Recycling Assets: Cleanaway Waste Management Limited (ASX: CWY) is a waste management company operating a national network of unique collection, processing, treatment and landfill assets. The company announced that it has acquired the assets of SKM Recycling Group for approximately $66 million and expects to offer employment to the majority of SKM’s full time employees. This Acquisition will offer the company with a network of five recycling sites, including three material recovery facilities and a transfer station in Victoria & a material recovery facility in Tasmania.

Launches Plan for Energy-From-Waste Project: Cleanaway Waste Management Ltd entered into a joint venture with Macquarie Capital’s Green Investment Group and planned to develop an energy from waste project in Western Sydney, which will utilize top European technology. The project will involve conversion of waste from households and local businesses into electricity for 65,000 Western Sydney homes.

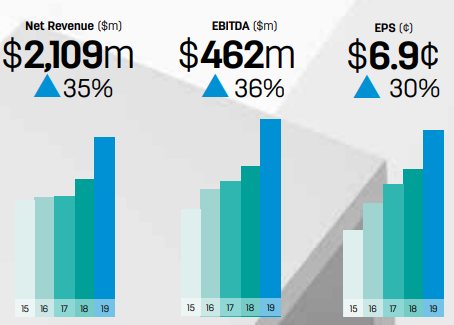

Significant Rise in Revenue: During FY19, net revenue of the company increased by 35% to $2,109 million, which led to an increase in statutory EBITDA of 34.2% to $433.7 million. The Board declared a fully franked final dividend of 1.90 cents per share, up 35.7% on pcp. Net operating cash flow from operating activities went up by 58.6% and increased to $350.8 million.

Financial Performance (Source: Company Reports)

Outlook: The Company is prioritizing to improve driver attentiveness and to maintain the momentum of growth and improvement in the businesses. Despite the outlook for general economic activity in Australia, the company expects to deliver earnings growth. Excluding the positive impact of $35 to $45 million of AASB 16, FY20 underlying EBITDA is expected to grow in slight moderation from the current market expectations. Post adoption of AASB 16 Leases standard change, NPAT is expected to decrease by $2 - $5 million and net interest expense is expected to increase by $8 - $12 million.

Stock Recommendation: Net margin of the company stands at 5.4% in FY19 as compared to the industry median of 9.9%. ROE and EBITDA margin of 4.9% and 19.9% is also lower than the industry median of 22.8% and 22.4%, respectively. As per ASX, the stock of CWY witnessed a fall of 26.29% in the past three months and 3.65% in the last one month as at 25 October 2019. Taking into the consideration of above-mentioned parameters, we advise investors to avoid the stock at the current market price of A$1.780 per share, down 3.784% on 28 October 2019.

Sims Metal Management Limited

Annual General Meeting is to be held on 14th November 2019: Sims Metal Management Limited (ASX: SGM) is engaged in buying, processing, selling of recycled metals and provision of environmentally responsible solutions for the disposal of post-consumer electronic products, including IT assets recycled for commercial customers. The company recently announced that 2019 Annual general meeting will be held on November 14, 2019 in order to discuss the Financial Reports, change of Company’s name, etc.

Trading Update:Considering the deteriorating market conditions, the company expects to report an underlying EBIT loss in the range of A$20 – A$30 million in 1HFY20. Full year FY20 will witness an underlying EBIT profit in the range of A$20 – A$50 million.

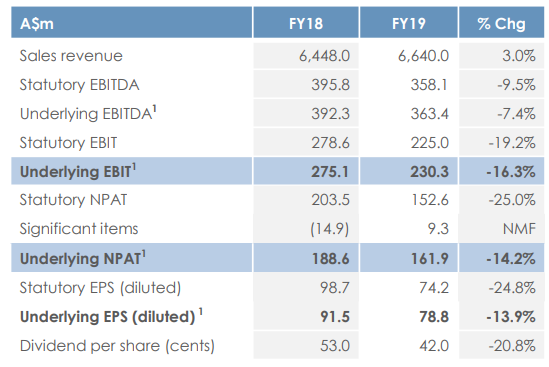

Strong Cash Flow: During the year ended 30 June 2019, sales revenue of the company went up by 3% to $6,640 million from $6,448 million in FY18. SGM finished FY19 with a strong net cash position of $347.5 million as at 30 June 2019 with an underlying EBIT of $230.3 million, which was down by 16.3% over the prior year. The company declared a fully franked final dividend of 19.0 cents per share, taking the total dividend for FY19 to 42.0 cents per share, representing a 53% underlying payout ratio.

Financial Performance (Source: Company Reports)

Outlook: The company expects to have an uncertain macroeconomic environment from increasing escalation of trade wars. It also anticipates that the domestic demand for Turkish steel will remain low, which will further compel Turkish mills to export in a soft global environment. SGM doesn’t expect the category 6 quotas in China to materially impact the non-ferrous business. It also believes that the Quality investments and strategy execution will allow the company to deal with the above market conditions.

Stock Recommendation: The stock of the company generated negative returns of 1.94% and 7.43% over a period of 1 month and 3 months, respectively. Gross margin of the company stands at 13.1% in FY19 and ROE at 7%. The stock of SGM is trading towards its 52-week low levels of $8.530. Despite the challenging market conditions and an expected underlying EBIT loss in 1HFY20, the company is optimistic about a recovery in the second half. The second half is expected to report a positive underlying EBIT. Moreover, the business will further improve on the back of a strong balance sheet and a disciplined approach to capital expenditure and cost management. Considering the above points and current trading levels, we recommend a “Hold” recommendation on the stock, which is currently trading at $9.200, down 8.821% on October 28, 2019, owing to the release of 1HFY20 trading update.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...