Australia and New Zealand Banking Group Limited

.png)

ANZ Details

Improvement in Capital Ratios – ANZ otherwise known to build on its turnaround strategy, had reported underlying profit of $3.3 billion for half year 2018 with bad and doubtful debts remaining at low levels. This resulted in rise of cash earnings to about $3.5 billion. The bank is also lately emphasising on coming up with buybacks and relevant capital management initiatives post the sale of non-core assets. ANZ has applied the Standardised approach to some portfolio segments (mainly retail and local corporates in the Asia Pacific) where currently available data does not enable development of advanced internal models for PD, LGD and EAD estimates. Recently, the Group announced Shane Buggle as its Group General Manager for Internal Audit and will be reporting to the Chairman of the Audit Committee Paula Dwyer. Mr. Buggle has spent more than 20 years in senior finance roles at ANZ and has been Deputy Chief Financial Officer since 2012. The appointment will be effective from 1 July 2018. The Group recently issued 2,894,309,399 fully paid Ordinary Shares. ANZ entered into an agreement to sell its 55% stake in Cambodian JV ANZ Royal Bank to J Trust, a Japanese diversified financial holding company listed on the Tokyo Stock Exchange. The JV otherwise proved to be beneficial to both ANZ and to the Royal Group over the past 13 years. The move was now in line with ANZ Group’s ongoing strategic review of international partnerships so that it will help in simplification of the business and the bank can operate its wholly-owned Institutional businesses in the region.

.png)

CET1 Ratio (Source: Company Reports)

The Group announced the sale of its stakes in Metrobank Card Corporation in the Philippines and Shanghai Rural Commercial Bank in China. ANZ will continue to own its 55% stake and manage the ANZ Royal business for up to 12 months and will work closely with J Trust so that a smooth transition of ownership happens. The transaction was approved by the Royal Group but remains subject to final regulatory approval from the National Bank of Cambodia and the Ministry of Commerce. It was noted that Capital ratios had increased in the half to March 2018 mainly due to cash earnings generation and benefits from the settlement of asset disposals. Currently, its CET1 ratio is in excess of APRA’s ‘unquestionably strong’ benchmark and is well ahead of the 2020 implementation date. In addition to this, further cost reductions are expected to support its improving returns. Since the start of the year, the shares have been declining by 2.97 per cent and were down by 4.5 per cent in last three months. The stock started recovering in the past one month and rose up by 3.3 per cent despite the Royal Commission. The Group is trading at a reasonable price with a decent dividend yield (fully-franked) of about 5.7 per cent. We give a “Buy” recommendation at the current market price of $27.72.

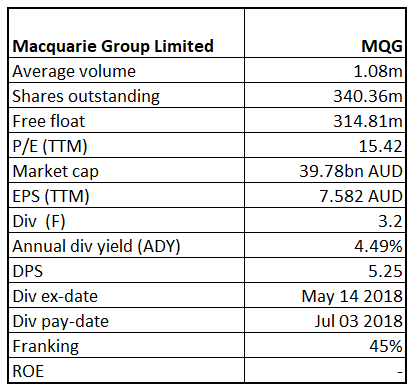

Macquarie Group Limited (ASX: MQG)

MQG Details

An increase in Operating Expenses – When compared to investment banks at global level, Macquarie Group Limited (ASX: MQG) seems to be trading at a higher side. While listed in Australia and regulated by the Australian Prudential Regulation Authority (APRA), as a non-operating holding company of Macquarie Bank Limited (MBL), the Group announced that it will suspend its Capital Notes (ASX Code: MQGPA) from quotation at the close of trading on Monday, 28 May 2018. The Group announced that these suspensions of Capital Notes will be applicable only for Macquarie Group Capital Notes and not for any other quoted securities of the Company. The Group recently announced the initial allocation of $A650 million of Macquarie Group Capital Notes 3 (“MCN3”) to Syndicate Brokers and Institutional Investors under the Institutional Offer and the Broker Firm Offer, pursuant to its offer of MCN3 which was announced to the Australian Securities Exchange on 7 May 2018. The Margin has been set at 4.00 per cent per annum, which was at the bottom of the expected Margin range of 4.00-4.20 per cent per annum. MGL intends to redeem the MCN on 7 June 2018 and will replace them with MCN3. This means that any MCN not reinvested under the Reinvestment Offer may be redeemed on this date and MCN Holders will receive $100 per MCN.

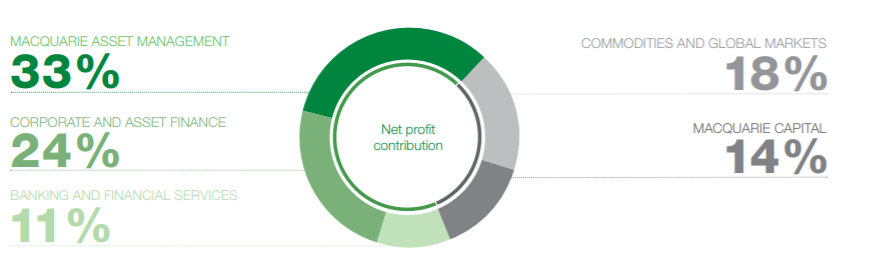

FY18 Net profit contribution (Source: Company Reports)

It is worth noting that the Net operating income of $A10,920 million for the year ended 31 March 2018 increased by 5 per cent from $A10,364 million in the prior year and on the other hand total operating expenses of $A7,456 million for the year ended 31 March 2018 increased by 3 per cent from $A7,260 million in the prior year. Total fee and commission income of $A4,670 million for the year ended 31 March 2018 increased by 8 per cent from $A4,331 million in the prior year largely due to higher performance fees from MIRA-managed funds and assets outperforming their respective benchmarks. The Group is also planning to merge its private bank and wealth division which will result in exit of about a dozen of advisers as the Group is looking forward to focussing on high net worth (HNW) investors that will enable them to better deliver on this commitment, with a comprehensive and tailored wealth and banking offering. In last one year, the stock has been rising up by 31.9 per cent and by 16.3 per cent in last six months. The stock prices climbed up by 6.5 per cent in last one month. The stock now looks “Expensive” at the current market price of $116.1 and it might be better to wait and watch for the impact of its new strategy.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...