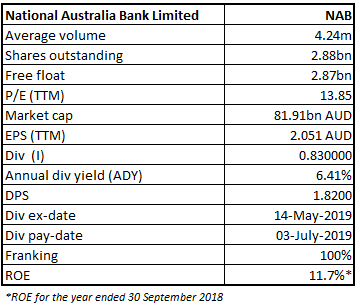

National Australia Bank Limited

NAB Details

Reduction in 2H19 Expected Cash Earnings Due to Additional Costs:National Australia Bank Limited (ASX: NAB) is engaged in the provision of banking services, including credit and access card facilities, leasing, housing and general finance, wealth management services, etc. The bank recently updated the exchange that it became a substantial shareholder in Nine Entertainment Co. Holdings Limited with a voting power of 5.161%.

S&P Credit Profile and Hybrid Ratings: Recently, S&P confirmed the standalone credit profile of NAB, improving the rating from ‘a-’ to ‘a’. The change in SACP (stand-alone credit profile) raised the rating on Additional Tier 1 capital instruments from ‘BB+’ to ‘BBB’. The rating on Tier 2 capital instruments raised to ‘BBB+’ from ‘BBB’. Long-term and short-term issuer credit ratings for NAB stood at ‘AA-’ and ‘A-1+’, respectively.

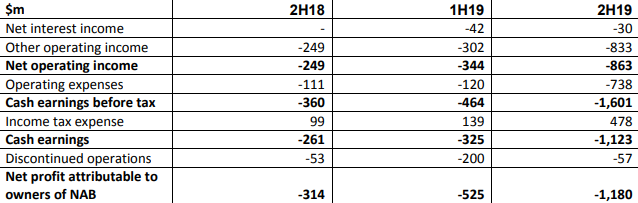

Additional Costs for Remediation and Software: The bank recently updated the exchange on additional charges of $1,180 million after tax, with respect to increased provisions for customer-related remediation and change in the application of the software capitalisation policy.The additional charges came in as a result of provision for potential customer refunds of adviser service fees paid to self-employed advisers. As a result, cash earnings in the 2H19 are expected to witness an approximate reduction of $1,123 million after tax. In addition, earnings from the discontinued operations are expected to see an estimated fall of $57 million after tax. As per the report, 2019 full-year results will be released on 07 November 2019.

Impact of Additional Charges on Full Year Results (Source: Company Reports)

Stock Recommendation: The stock generated negative returns of 4.34% and 0.80% over a period of 1 month and 3 months, respectively. Currently, the bank has a market capitalisation of $81.91 billion and a price to earnings multiple of 13.850x. Despite a challenging operating environment during the June 2019 quarter, the company reported a decent performance in comparison to the quarterly average for 1H19. SME lending growth over the quarter was a highlight with better customer outcomes. Simplification of services to customers led to 27% reduction in over-the-counter transactions and 18% reduction in call centre volumes. Considering the aforesaid factors along with the current trading levels,we give a “Buy” recommendation on the stock at the current market price of $27.690, down 2.534% on 04 November 2019.

NAB Daily Technical Chart (Source: Thomson Reuters)

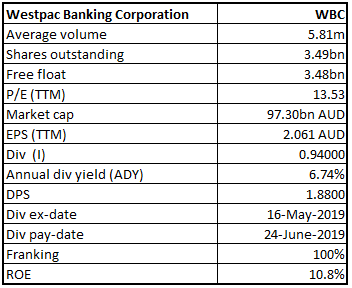

Westpac Banking Corporation

WBC Details

Recent Capital Raising to Enhance Balance Sheet Flexibility:Westpac Banking Corporation (ASX: WBC) is a provider of financial services, including lending, payments services, investment portfolio management and advice, superannuation and funds management, deposit taking, general finance, etc.

The bank recently announced the distribution of $0.3100 per security for SFI (Self-Funding Instalments) over securities in Bank of Queensland Limited (BOQ) as mentioned in PDS (Product Disclosure tatement) and dividends will be applied to reduce the Completion Payment of the SFIs and will be paid on or about 27 November 2019 with the ex-dividend date of 06 November 2019.

Capital Raising:As per another update, the bank launched a capital raising through a fully underwritten institutional share placement worth $2 billion and a non-underwritten share purchase plan to raise an approximate amount of $500 million. Pursuant to the announcement, trading in the shares has been put on halt and are expected to commence trading on 05 November 2019.

FY19 Financial Highlights:During the year ended 30 September 2019, the company reported cash earnings of $6,849 million, down 15% on prior corresponding year. The decline in cash earnings was due to higher costs associated with exiting financial planning, increased regulatory and compliance costs, lower interest margins & decline in wealth management and insurance revenue. Customer deposits for the year amounted to $525 billion, up 1% on pcp. Total business lending in Australia and New Zealand amounted to $152 billion and $32 billion, respectively. Total home lending at the two locations amounted to $449 billion and $52 billion, respectively. The 2019 Annual General Meeting for the bank will be held on 12 December 2019. During the year, the bank’s reported net profit amounted to $6,784 million, down from $8,095 in 2018. The number of customers on the bank’s platform went up by 1% to 14.2 million.

FY19 Highlights (Source: Company Reports)

The recent capital raise of $2.5 billion is expected to enhance the balance sheet flexibility and will provide increased buffer above the Australia Prudential Regulation Authority’s common equity Tier 1 (CET1) capital ratio benchmark of 10.5%.As per the bank, the additional capital will add approximately 46 -50 basis points to Level 2 CET1 capital ratio. The bank’s stock is currently on a trading halt on account of the capital raising announcement. In the last one month and three months, the stock generated negative returns of 6.13% and 3.19%, respectively, and has a market capitalisation of $97.3 billion. Price to earnings multiple for the stock currently stands at 13.530x at the market price of $27.88.

.jpg)

WBC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...