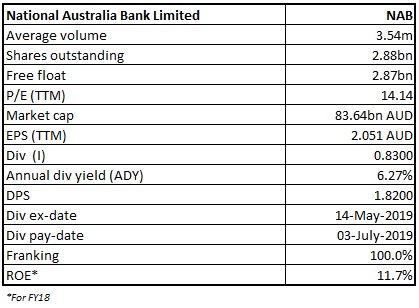

National Australia Bank Limited

NAB Details

Decent Performance Despite Macro Challenges: National Australia Bank Limited (ASX: NAB) operates in a wide range of financial products and services, namely banking, loans, credit and debit card services, investment banking, wealth management, leasing, housing and general finance, funds management, etc. On 25 October 2019, NAB S&P Global Ratings (S&P) has revised its view on its standalone credit profile from 'a-' rating to 'a' rating. S&P affirmed the 'AA-' long-term and 'A-1+' short-term issuer credit ratings for NAB with a 'stable’ outlook. Additionally, S&P confirmed Basel III compliant Tier 2 capital instruments to 'BBB+' from 'BBB' and Basel III compliant Additional Tier 1 capital instruments to 'BBB-' from 'BB+'. NAB will release its 2019 full-year results on 7 November 2019.

3Q FY19 Performance Highlights for the year ended 30 June 2019: NAB declared its third quarter results for FY19, wherein the bank reported unaudited statutory net profit at $1.70 billion and 1% growth in cash earnings on pcp. The business reported a growth of 1% in revenue, aided by growth in SME lending and slight improvement in the Banks’s overall margin. During Q3FY19, NAB witnessed 10% growth in credit impairment at $247 million compared with the 1H19 quarterly average. Common equity Tier 1 (CET1) ratio remained at 10.4%, excluding $1 billion of 1H19 Dividend Reinvestment Plan. On an APRA basis, leverage ratio during the quarter came in at 5.4%, and liquidity coverage ratio (LCR) stood at 128%. The business reported a net stable funding ratio (NSFR) at 113%.

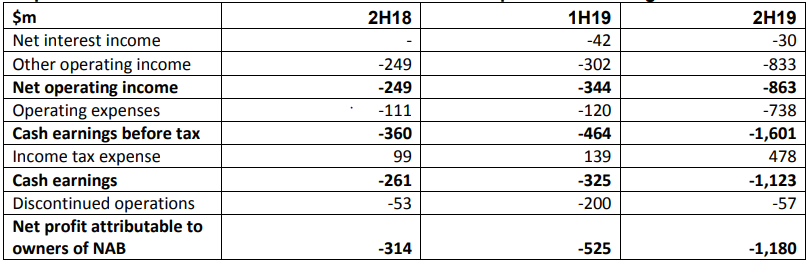

Guidance: The Management has guided that the H2FY19 result will include a cost of $832 million after tax, related to additional customer-related remediation. The Management informed that the key driver of these additional charges is the inclusion of a provision for potential customer refunds of adviser service fees paid to self-employed advisers.

Impact of Customer related remediation and Software Expense (Source: Company Reports)

Stock Recommendation: The stock of NAB is quoting at $29.180 with a market capitalization of $83.64 billion. 52-week trading range of the stock stood at $22.52 to $30.00 and currently, the stock is trading at the upper band of its 52-week trading range. The stock has delivered returns of 2.40% and 13.06% during the last three months and six-months, respectively. The stock is available at a price to book value multiple of 1.5x on trailing twelve months (TTM) basis as compared to the industry median of 1.6x. Despite a tepid macro environment and a subdued home lending growth, NAB showed a decent performance in 3QFY19. Considering the aforesaid facts, price movement and current valuation, we recommend a ‘Hold’ rating on the stock at the current market price of $29.180, up 0.586% on 25 October 2019.

NAB Daily Technical Chart (Source: Thomson Reuters)

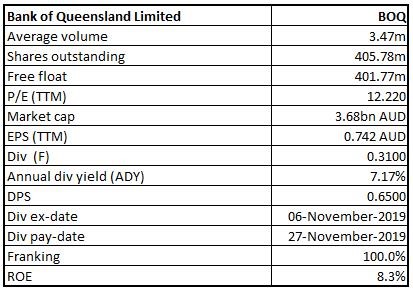

Bank of Queensland Limited

BOQ Details

Decent Year-on-year Lending Growth:Bank of Queensland Limited (BOQ) operates in banking and financial activities and has subsidiaries such as Virgin Money Australia, BOQ Finance, BOQ Specialist, and St Andrew’s.On 25 October 2019, BOQ informed that one of its directors named Richard Hairewill be retiring from the Board following the release of FY20 second-half results. Further, the company informed that Chief Financial Officer and Chief Operating Officer, Ewen Stafford will commence his service on 11 November 2019.

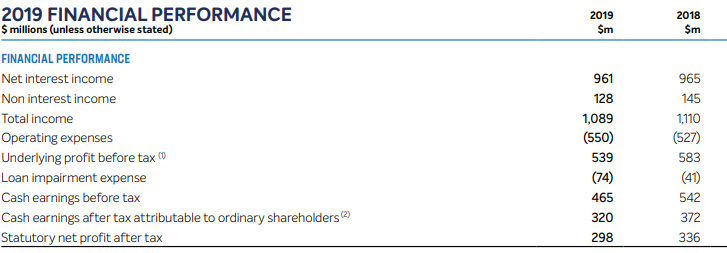

FY19 Operating Highlights for the period ending 30 June 2019: BOQ announced its FY19 full-year financial results, wherein the company reported a statutory net profit after tax at $298 million, down 11% on y-o-y basis and 14% decrease in cash earnings at $320 million. BOQ reported total income at $1,089 million as compared to $1,110 million on the previous financial year. The business saw cash return on equity at 8.3% and common equity tier ratio at 9.04%.Net interest margin during the year came in at 1.93% as compared to 1.98% during FY18. Cost-to-income ratio during the year stood at 50.5% as compared to 47.5% in FY18. Total lending grew by $937 million, or 2% during the year. As per the Management, this was primarily driven by the Business Bank, with mortgages underperforming.

FY19 Financial Performance (Source: Company Reports)

The company has declared fully franked dividend ofAUD 0.310000 per ordinary share, payable on 27 November 2019.

Outlook: For FY20, BOQ expects the front to back book dynamic to be continued, providing a headwind of around 4 bps per half. The management expects a benefit to NIM of 5-6 basis points in the first-half of FY20.

Stock Recommendation: The stock of BOQ is trading at $9.080 with a market capitalization of $3.68 billion. The stock is quoting near the lower band of its 52-week trading range of $8.70 to $10.77. The stock has generated -1.31% and -2.68% return during the last three-months and six-months, respectively. The stock is available at a price to book value multiple of 1.0x on TTM basis as compared to the industry median of 1.6x. BOQ enjoyed a decent balance sheet during FY19, and the Management is paying significant attention to retain it. BOQ has delivered 2% loan growth during FY19 despite a challenging scenario. Considering the above factors, we recommend a ‘Buy’ rating on the stock at the current market price of $9.080, up 0.11% on 25 October 2019.

BOQ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...