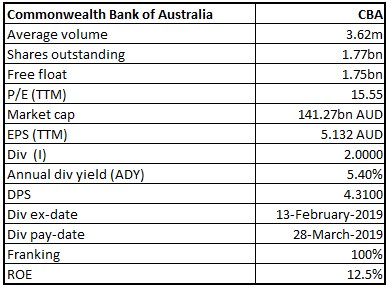

Commonwealth Bank of Australia

CBA Details

Report of Independent Reviewer: Commonwealth Bank of Australia (ASX: CBA) is involved into the business areas such as retail banking services, business and private banking, institutional banking and markets, wealth management, ASB New Zealand and international financial services. On 7th August 2019, Commonwealth Bank of Australia updated the market with the Independent Reviewer’s third and fourth reports into the progress of CBA’s Prudential Inquiry Remedial Action Plan. The bank stated that the reports provide an update on actions taken by the CBA in order to deliver against the Remedial Action Plan from 1 December 2018 to 30 June 2019.

The Independent Reviewer has noted the ‘solid progress in executing a necessarily ambitious plan’ in its fourth report. As per the release dated 7th August 2019, the bank stated that it has decided to cease providing the licensee services through Financial Wisdom by June 2020 and will proceed with an assisted closure. However, the bank will support advisers through an orderly transition to alternative arrangements, which includes self-licensing or joining another licensee.

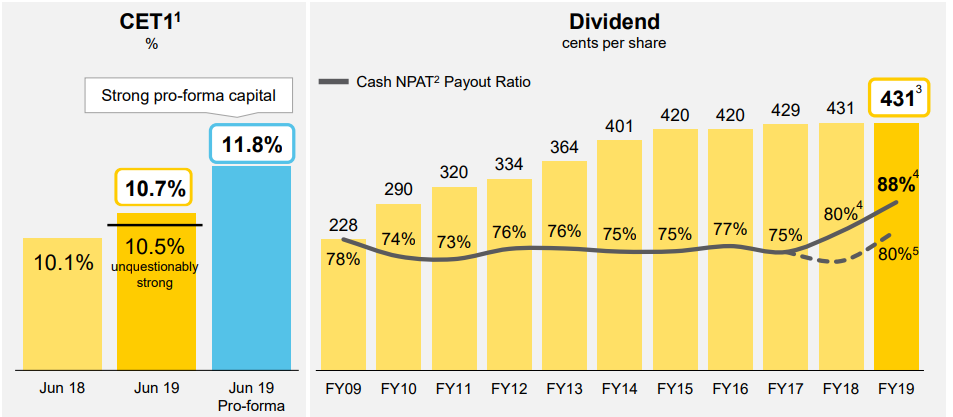

The estimated pre-tax costs of supporting Financial Wisdom and CFP-Pathways businesses, their advisers, as well as their customers through the transition, and other internal project costs, happens to be around $26 million. The Bank is going to conduct its Annual General Meeting on 16th October 2019. In FY19, CBA's Statutory NPAT stood at $8,571 million while its Cash NPAT stood at $8,492 million. The following picture provides a broader idea of CET1 ratio and dividends of the bank:

CET1 and Dividend (Source: Company Reports)

Further, ASB reported a statutory net profit after taxation amounting to $1,274 Mn for the year ended 30th June 2019, which reflects a rise of 8% on the previous year. The cash net profit after tax for FY19 stood at $1,191 Mn with a rise of 4% on the previous year. ASB witnessed continued momentum in funds management with 13% growth in income.

What to Expect: The bank is anticipating its operating context to remain challenging as it is adapting to heightened regulatory change, evolving customer preferences, and intense competition. However, the Bank is well-placed to navigate this changing landscape on the back of resilient balance sheet, leading distribution and digital assets and a strong customer base.

Stock Recommendation: The bank is driving strong capital generation, and it is investing for long-term. On the stock performance front, it provided returns of 6.49% and 9.92% in the time period of three months and six months, respectively. As per ASX, the stock is trading closer towards 52-weeks high price of $83.990, which increases the probability for a correction in the near term. Hence, we have a watch view on the stock at the current market price of $78.700, down 1.378% on 07 August 2019 and suggesting that investor should wait for better entry levels.

CBA Daily Technical Chart (Source: Thomson Reuters)

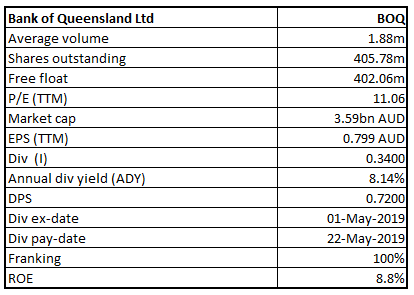

Bank of Queensland Limited

BOQ Details

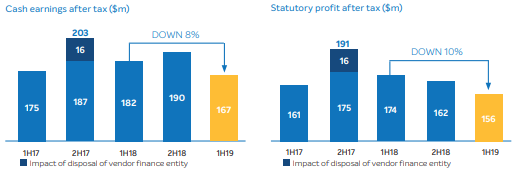

Disclosures Under APRA: Bank of Queensland Limited (ASX: BOQ) provides banking, financial and related services. Recently, the bank added that its capital management strategy aims to ensure adequate capital levels are maintained in order to protect deposit holders. The bank posted a CET1 capital ratio of 8.9%, and total capital ratio stood at 12.3% as at 31st May 2019. In the 1H FY19, the bank reported cash earnings after tax amounting to $167 Mn and cash operating expenses of $268 Mn. Bank of Queensland Limited’s funding strategy and risk appetite reflects the Group’s business strategy, adjusted for the current economic environment. Adding to that, it was stated that funding is managed to allow for various scenarios that might impact bank’s funding position.

Key Metrics (Source: Company Reports)

In 1H FY19, the bank posted Cash basic earnings per share of 41.8 cents per share, reflecting a fall of 10% from 1H FY18. The cash net interest margin of the bank stood at 1.94% in 1H FY19, which can be considered at respectable levels. Based on the portfolio repricing, which was wrapped up in January, the bank expects a further 3 to 4 basis point benefit from this element in 2H FY19. The bank would continue to manage its liability base in order to optimise margin.

Coming to the stock’s performance, it produced returns of -6.36% and 0.23% in the time span of one month and three months, respectively. As per ASX, the bank’s annual dividend yield is 8.14%, which might attract the attention of dividend-seeking investors moving forward. Currently, the stock is trading at close to its 52-week low levels of $8.700 with reasonable PE multiple of 11.06x, proffering a decent opportunity for accumulation. Hence, considering the above-stated facts and decent outlook, we give a “Buy” recommendation on the stock at the current market price of A$8.930 per share (up 1.018% on 7th August 2019).

BOQ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...