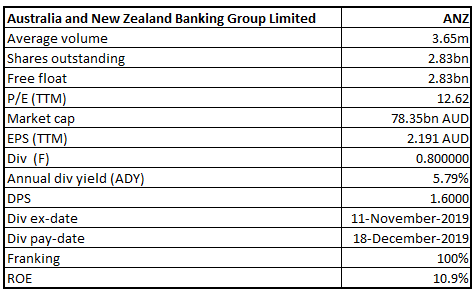

Australia And New Zealand Banking Group Limited

ANZ Details

A Look at Full-Year 2019 Results: Australia and New Zealand Banking Group Limited (ASX: ANZ) provides banking and financial products and services to individual and business customers. The market capitalisation of the bank stood at ~A$78.35 Bn as on 31st October 2019. Recently, the bank has updated the market with its results for the 12 months ended 30th September 2019, wherein it reported cash NPAT amounting NZ$1,933 Mn, reflecting a rise of 2% as compared to the previous year. It added that this has been benefited from the sales of life insurance company OnePath Life (NZ) Limited and ANZ New Zealand’s 25% share in Paymark Limited. The Acting CEO of ANZ New Zealand stated that the bank’s full-year result reflected a solid underlying performance. However, it had been a challenging 12 months for ANZ New Zealand reputationally.

ANZ announced a proposed 2019 final dividend amounting to 80 cps, partially franked at 70%. New Zealand imputation credits of NZD 9 cents per share would also be attached. The following picture provides an idea of key dates for 2019 final dividend and the associated DRP and BOP (Bonus option plan):

Key Dates (Source: Company Reports)

What to Expect:ANZ’s key personnel stated that the housing market of Australia is slowly recovering, however, it anticipates challenging trading conditions to be continued for the foreseeable future. ANZ anticipates the operational improvements made to its Australian home loans business to help restore market share in its targeted segments. Record low-interest rates and intense competition would continue to impact profitability.

Stock Recommendation:The bank is engaging with APRA and Reserve Bank of New Zealand on their announced proposals, which could lift the amount of capital that is required in order to support its New Zealand subsidiary. Onthevaluation front, the stock of ANZ is trading at a price to book multiple of 1.3x as compared to the industry average of 2.8x on TTM basis. It has EV to Sales multiple of 4.1x as compared to the industry average of 10.2x on TTM basis. CET1 capital ratio for the bank stands at 11.4%, in-line with FY18 levels. On the stock’s performance front, it produced a return of 15.84% on YTD basis and witnessed a rise of 7.72% in the time span of one year. Therefore, considering the recovery in the housing market, operational improvements, decent outlook along with a track record of paying dividends consistently (while franking has been lowered to a new base), we give a "Buy" recommendation on the stock at the current market price of A$26.740 per share, down 3.256% on 31st October 2019.

ANZ Daily Technical Chart (Source: Thomson Reuters)

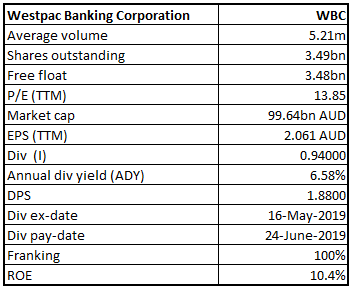

Westpac Banking Corporation

WBC Details

Ratings Upgraded by S&P: Westpac Banking Corporation (ASX: WBC) is one of the leading banks in Australia and has a market capitalisation of ~A$99.64 Bn as on 31st October 2019. As per the recent release dated 28th October 2019, WBC has acknowledged the judgment by the Full Federal Court, which is related to the provisioning of financial product advice, in which the Court allowed ASIC’s appeal and dismissed Westpac’s cross-appeal. It was also mentioned that this decision relates to a test case brought by ASIC against Westpac Securities Administration Limited and BT Funds Management Limited in relation to calls to 15 customers concerning the rollover of their superannuation accounts. However, WBC is carefully considering the judgment.

In another update, it was mentioned that S&P Global Ratings has upgraded WBC’s stand-alone credit profile as well as the rating on certain capital instruments.After a regular review of its Banking Industry Country Risk Assessment, S&P Global Ratings has raised its Economic Risk assessment of Australia to 3 from 4. Post this change S&P upgraded WBC’s stand-alone credit profile by one notch to ‘a’ from ‘a-’.

S&P also increased the rating on certain capital instruments issued by WBC by one notch. Securities impacted include (1) Basel III compliant Tier 2 instruments to 'BBB+' from 'BBB' and (2) Basel III compliant Additional Tier 1 capital instruments to 'BBB-' from 'BB+'.

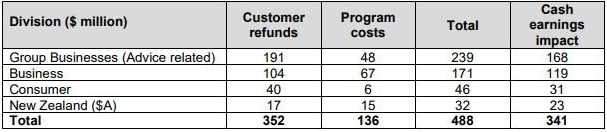

Cash Earnings Impact (Source: Company Reports)

Future Aspects:In 1H FY19 results, the bank stated that the economy would be supported by the robust government investment and exports, in resources and services. The bank also expects that its service-led strategy remains the best way when it comes to create value for its shareholders.

Stock Recommendation:As at 30th June 2019, the bank reported a CET1 capitalratio of 10.5% as compared to 10.6% in March 2019, reflecting a marginal decline. The bank is currently trading at a price to book multiple of 1.6x against the industry average of 2.8x on TTM basis. It has a price to cash flow multiple of 11.9x as compared to the industry median of 13.3x on TTM basis. The stock generated a return of 3.78% and 6.37% in the time period of six months and one-year, respectively. Currently, the stock is trading close to its 52-week higher levels of A$30.050 with a price earnings multiple of 13.85x and an annual dividend yield of 6.58%. Hence, considering the recent upgrade of ratings by S&P, decent fundamentals, and current trading levels, we reiterate our “Hold” recommendation on the stock at the current market price of A$28.210 per share, down 1.191% on 31st October 2019.

WBC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...