Sydney Airport

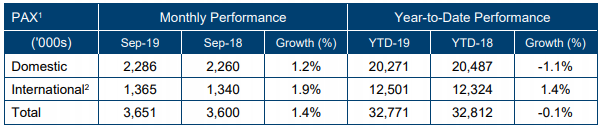

Airport’s Traffic Performance for September 2019:Sydney Airport (ASX: SYD) is engaged in the business of airport operations and has a market capitalisation of $19.88 billion as on 11th November 2019. Sydney Airport reported its traffic performance for September 2019, with the growth in international passenger traffic in-line with August. The second consecutive month of double-digit growth was reported by arrivals from India with yoy growth of 11.2% on September 2018 and 8.4% growth on YTD basis.

Indonesian passenger growth was recorded at 16.1% over the previous corresponding period. Domestic traffic grew by 1.2% over September 2018, and international passenger numbers were up by 1.9%.

September 2019 Performance (Source: Company Reports)

Changes To The Compliance Committee: The Trust Company (Sydney Airport) Limited, part of Perpetual Limited, which is the responsible entity for the Sydney Airport Trust 1 has advised that Michelene Collopy has retired as Chairman and member of the Compliance Committee of the responsible entity and Johanna Turner has been appointed as Chairman and member of the Compliance Committee of the responsible entity.

The current members of the compliance committee of the responsible entity are Johanna Turner, Virginia Malley and Simone Mosse.

Stock Recommendation: Total revenue of SYD has witnessed a CAGR growth of 8.03% over the period of FY 2014 - FY 2018. Thus, it can be said that SYD is possessing respectable capabilities to garner revenues.The company’s EBITDA margin stood at 81.4% in the first half of 2019, which is above the industry median of 51.8%. The stock has a price to earnings multiple of 49.830x, which is higher than the industry average of 16.6x on a TTM basisindicating that the stock is overvalued at the current juncture. As per the ASX, the stock of SYD is trading close to its 52-week higher levels. Thus, we have a watch stance on the stock at the current market price of $8.890 per share, up 1.023% on 11th November 2019 and suggest investors to wait for further catalysts to support the valuation.

Auckland International Airport Limited

Highlights of AGM:Auckland International Airport Limited (ASX: AIA) is the third busiest international airport in Australasia as more than 75% of all international visitors to New Zealand arrive here. In the past 12 months, more than 20.5 million passengers have travelled through the airport’s terminals. The market capitalisation of the company stood at $10.52 billion as on 11th November 2019.

2019 was a solid year for Auckland Airport as it reported revenue of $743.4 million, up by 8.7%. The total number of travellers increased to 21.1 million, up by 2.8% on the previous year. Company’s operating EBITDA before fair value adjustments and investments in associates went up by 9.6% to $554.8 million. However, the company reported PAT of $523.5 million, which declined by 19.5% as the prior year’s result was boosted by profit on the sale of 24.6% shareholding in North Queensland Airports.

The company declared a final dividend of 11.25 cents per share, up 2.3% on the prior year as underlying EPS rose 3.6% to 22.8 cents per share.

Recently, Elizabeth Savage became part of the company’s Board as an independent non-executive director, following a go-ahead for her nomination during the AGM.Christine Spring was also appointed as an independent non-executive director of the company, after approval at the AGM.

Outlook for 2020: The company is expecting underlying NPAT (excluding any fair value changes and other one-off items) to be in between $265 million to $275 million for the FY20. The company expects total capital expenditure to be between $450 million to $550 million.

Airport’s Monthly Traffic Update for August 2019: The total number of passengers decreased by 0.1% in the month of August 2019 as compared to the last year.International passengers were flat with the pcp, while domestic passengers were down by 1.4% and transit passengers were up by 11.8%.

.png)

August 2019 Performance (Source: Company Report)

Stock Recommendation: The top-line of the company witnessed a CAGR growth of 9.96% over the period of FY15-19, indicating strong revenue-generation capabilities of it. The stock has gained ~26.42% on YTD basis. The company’s EBITDA margin stood at 74.7% in FY19, well-above the industry median of 48.1%. The stock has a price to earnings multiple of 20.880x, above as compared to the industry average of 16.6x on TTM basis. This shows that the company is overvalued as compared to its peers. Based on the mixed scenario, like higher PE multiple and good CAGR growth, higher returns on YTD, etc., we have a wait and watch stance on the stock at the current market price of $8.600 per share, down by 0.693% on 11th November 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...