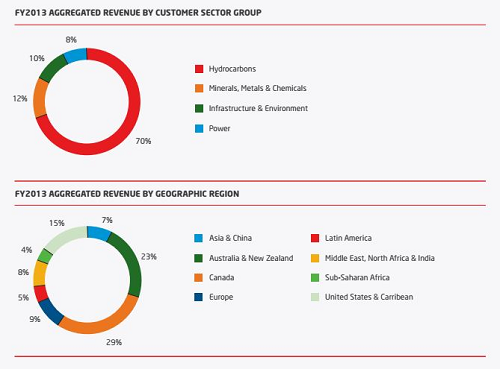

Company Overview – Worley Parsons is a leading global provider of professional services, such as engineering procurement and construction management, to the oil, gas, mining, power and infrastructure sectors. Hydrocarbons is the largest business contributing 72% of revenue. Minerals, metals and chemicals contribute 15% of revenue and infrastructure 13%. Worley Parsons has a global presence with around 38000 staff in 43 countries. It has a strong and growing presence in the fast growing developing economies with 40% of staff of staff in these regions.

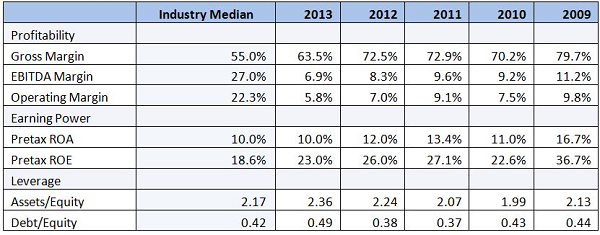

Analysis – Worley Parsons is a well-established and highly regarded provider of engineering and other professional services to the oil, gas, mining, power and infrastructure sectors. Extensive professional skill levels, solid delivery capabilities, global scale, and strong customer relationships are some of the strong points for Worley Parsons business. Cash flow and return on invested capital are high and capital requirements low. A strong growth outlook for the global oil, gas and petrochemicals sector underpins the medium term earnings outlook.

Worley Parsons Aggregated Revenue (Source - Company Reports)

Worley Parsons Aggregated Revenue (Source - Company Reports)

Worley Parsons has developed a high level of expertise in unconventional oil and gas and is well positioned to benefit from the expected strong growth in activity in this sector. With a strong balance sheet Worley Parsons is well placed to make further accretive acquisitions to help supplement organic growth. Worley Parsons reported a large drop in the first half fiscal 2014 earnings because of the Week Australia mining sector and higher costs from a Canadian fabrication contract. Underlying net profit after tax or NPAT fell 35% to AUD 100.7 million on 2% decline in aggregated revenue.

Fiscal 2014 guidance has been maintained, for NPAT in the range of AUD 260 million to AUD 300 million. This implies a much stronger second half., which we think is reasonable given lower restructuring costs in Australia and the finalisation of the underperforming Canadian fabrication contract. We retain our positive view of the medium term outlook driven by the favourable outlook for capital spending in the oil and gas sector, particularly in unconventional oil and gas sector, and offshore oil where Worley Parsons has strong capabilities.

In a difficult environment we believe the company is controlling its controllable better. WOR is getting serious on cost reductions with 500 overhead positions taken out in the last few months. We think this represents $50m of cost saves but not all of this will stick partly because WOR has a cost reimbursable model. There is more to be done given global support costs which are still running at 4.9% of sales and with 1H margins at a paltry 4.7%. WOR needs to do more on cost and is taking steps forward. There was better than expected cash flow and dividend at $230m and 34 cents per share respectively. Operating cash flow more than doubled compared to the previous corresponding period benefitting from $52m working capital release. Balance sheet is very healthy with 25% gearing sitting at the bottom of range. The core hydrocarbons business (72% of revenue) performed relatively well when excluding the underperforming Canadian fabrication contracts, with EBIT down just 3%.

WOR Daily Chart (Source - Thomson Reuters)

WOR Daily Chart (Source - Thomson Reuters)

The result benefited from the inclusion of the acquired Rosenberg Worley Parsons business and better margins on new work in the U.S. This partly offset lower performance in Australia as major projects completed and weakness in Canada with a slowdown in Oil Sands activity. Canadian oil sands is now showing signs of pick-up in activity which will help the second half. The completion of major LNG projects will continue to impact the Australian business. Despite the slowdown in activity in some Australian segments, this is a diversified global business and will benefit from the long term growth in oil and gas capital spending. We continue to see opportunities in offshore deep-water oil, liquefied natural gas and unconventional oil and gas, areas of strength for Worley Parsons. Industry conditions are changing towards lower growth and higher volatility.

We believe WOR has the tools at its disposal to make the most of this - a strong balance sheet, a capital light model, geographic and functional diversity and exposure to the key offshore and unconventional growth segments. The slowdown in Australian mining sector capital spending continues to take its toll on the infrastructure division which saw earning before interest and tax or EBIT decline 41%. In addition to the decline in resources infrastructure related work in Australia, government advisory work fell and the European division was impacted by the cancellation of a Nuclear contract. Actions taken to downsize the Western Australian business should result in an improved performance in second half fiscal 2014 and beyond.

This leading global engineering services provider is ideally positioned to benefit from increased capital expenditures in natural resources markets, particularly unconventional oil and gas, coal and iron ore. Power, infrastructure and environmental markets should all grow strongly in the medium term as developing nations seek to upgrade their population’s quality of life. Little of the company’s own capital is placed at risk and the risks of rising wages are limited because most contracts cover WOR’s costs plus a margin. With a strong balance sheet and cash flow, the company is in a strong position to undertake further acquisitions to deepen and widen capacity, skill sets and industry position.

Growth in the developing world also presents significant opportunities with rapid growth in infrastructure and power generation. While competitors may try to replicate Worley Parsons’s skills and strong client relationships, this would take some time given Worley Parson’s global reach and the strength of its existing relationships. The recent downgrades appear to be an industry wide project slippage issue rather than WOR specific and should reverse in the medium term. We like the WOR story and would be putting a BUY on the stock at the current price of $15.19.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...