Company Overview: Worley Limited (ASX: WOR) is mainly involved in providing engineering design and project delivery services, including maintenance, reliability support services and advisory services to energy, chemical and resources sectors. In energy space, the company is responsible for extraction and processing of oil and gas as well as projects related to all forms of power generation, transmission and distribution. Besides that, the company is also involved in the extraction and processing of mining, mineral and metal resources, and resource projects related to water, the environment, transport, ports and site remediation and decommissioning..jpg)

WOR Details

.png)

Enhanced Earnings Diversification and Resilience: Worley Limited (ASX: WOR) provides engineering, procurement and construction expertise to the upstream, midstream, chemicals, power, and mining and minerals sectors. The company follows the strategy of diversifying earnings by growing in the Chemicals and Mining, Minerals & Metals sectors. In-line with this strategy, last year, the company completed the acquisition of the Energy, Chemicals and Resources division of Jacobs Engineering Group Inc. or “ECR”. As a result of this acquisition, the company has become a pre-eminent global provider of professional projects and asset services in energy, chemicals and resources. Further, the company has enhanced the diversity and resilience of its earnings. From 2016-2019, the company’s aggregated revenue has increased at a CAGR of 3.99%. During the same period, EBITA has increased at a CAGR of 27.66%. .png)

Five-year performance (Source: Company Reports)

Looking forward, the global energy transition is expected to open opportunities across all markets that Worley Limited serves. As a result of the company’s deep domain knowledge and expertise in the power and new energy space, Worley Limited is well-positioned to support its customers in leading and navigating this new world.

FY19 Performance Highlights: In FY19, Worley Limited reported an underlying net profit after tax (post-tax impact of amortization on intangible assets) of $259.8 million and delivered a positive operating cash flow of $236.3 million. During the year, the company’s aggregated revenue increased by 35.6% to $6,439.1 million. For FY19, the company paid a total dividend of 27.5 cents per share, representing 52.2% of full-year underlying profit after tax. The most notable achievement in FY19 was the acquisition of ECR, which is expected to deliver enhanced earnings diversification and resilience and bring significant value upside through cost and revenue synergies.

H1 FY20 Results Highlights: In H1FY20, the company’s profit after income tax expense was $115 million, up $33 million on pcp, underpinned by the aggregated revenue of $5,998 million, up 134% on pcp. During the period, the company saw more consistent earnings through increased proportion in opex, chemicals and North America and Europe.

In Energy & Chemicals Services business, the company reported aggregate revenue of $2,605 million in H1FY20, up 134% on pcp. For the same period, the aggregate revenue for Mining, Minerals & Metals Services, grew by 489% to $636 million. The aggregate revenue for Major Projects & Integrated Solutions increased by 133% to $2,432 million and for Advisian, the revenue grew by 26% to $325 million..png)

Line of Business Results (Source: Company reports)

Over the period, the company witnessed growth in all regions, particularly North America. Strong performance in Norway and Canada from construction and fabrication revenue was also observed. The company’s aggregate revenue in APAC region increased by 84% to $1,077 million, as compared to pcp. In AM region, the aggregate revenue increased by 286% to $3,044 million. .png)

Region-Wise Results (Source: Company Reports)

Over the period, the company continues to focus on delivering the benefits of the ECR acquisition. Worley Limited has increased the cost synergy target to $175 million in 30 months post acquisition. In-line with the ECR investment case, the company is observing more consistent earnings through increased exposure to operational expenditure and the chemical sector. The integration with ECR is substantially complete and the company is now focused on accelerating its transformation.

The company’s balance sheet remained strong with leverage ratio of 2.0x and gearing of 21.3%. As at 31 December 2019, the underlying operating cash flow was $277 million, and backlog was at $18.7 million. For the period, the Board has declared an interim dividend of 25 cents (unfranked) per fully paid ordinary share..png)

Half-Year Results’ Snapshot (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 51.88%. Dar Al-Handasah Shair and Partners Holdings Ltd. and Jacobs Engineering Group Inc. hold the maximum interest in the company at 22.78% and 9.87%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Managing Covid-19 Impacts: On 30 March 2020, the company provided an update on the COVID-19 pandemic, wherein it assured that it has entered this period of global disruption in a stable financial position. At the end of H1FY20, the company had around $580 million of working capital facilities which were scheduled to be reconfirmed or renewed in the coming six months. The company has proactively negotiated to working capital facilities and has received bank credit approval to extend around $480 million of those facilities for 12 months. As at 31 December 2019, the company had a total liquidity of $1.36 billion. There has been no significant change to this liquidity position as at 29 February 2020.

In order to manage the impacts of both the COVID-19 pandemic and the decline in oil price, the company is actively taking measures to align the cost base and deliver savings. To support the implementation of actions to protect financial and operational integrity, the company has established a task force.

Recent Contracts Win to Support Top-line Growth:

Shell Global Solutions Awarded two contracts: On 31 March 2020, the company announced that it has been awarded two contracts by Shell Global Solutions International BV for PT Pertamina EP Cepu’s (PEPC) new sulfuric acid plant in Indonesia. These contracts demonstrate the company’s commitment to providing the best technology and high value for its customers. Under these contracts, the company will supply Chemetics® proprietary Cooled Oxidation Reactor (CORE™) technology.

Contract from PT Enviromate Technology International: Worley Limited has recently been awarded a contract by PT Enviromate Technology International for PT Pertamina EP Cepu’s (PEPC) new sulfuric acid plant in Indonesia. Under this contract, the company will design and engineer a new sulfuric acid plant featuring Chemetics® proprietary Cooled Oxidation Reactor (CORE™) technology, supplying key equipment and materials, and will also provide technical services for plant erection, operator training, commissioning and testing.

Chevron awards Worley two-year Extension to Services Contract: On 31 March 2029, the company announced that it has been awarded a two-year extension to an existing services contract with Chevron Australia Pty Ltd. This contract demonstrates Worley’s global expertise and capability in the hydrocarbons and energy sectors.

Services contract in the Caspian Sea: On 5 March 2020, the company announced that it has been awarded a contract from Azerbaijan International Operating Co for engineering, procurement and construction services as part of a gas lift project. Under this contract, Worley will provide support for the production operations on the Chirag platform in the Caspian Sea.

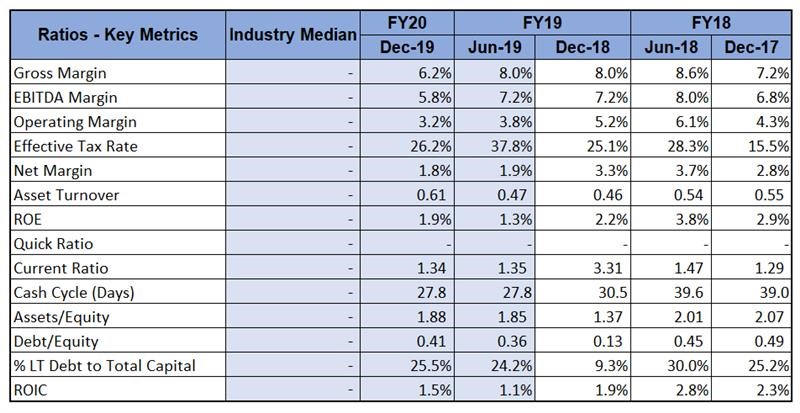

A Quick look at key Margins: For H1FY20, the company reported a gross margin of 6.2% and EBITDA margin of 5.8%. For the same period, the company has Asset Turnover ratio of 0.61x, higher than pcp. In the last one year, the company’s asset to equity ratio has increased from 1.37x in H1FY19 to 1.88x in H1FY20.

Key Metrics (Source: Thomson Reuters)

What to expect: Following the acquisition of Jacobs ECR, Worley Limited has become more resilient business with increased diversification across geographies and sectors. The company now has a lower exposure to upstream oil and gas capital expenditure which represents only 20% of its business and has increased exposure to the less cyclical chemicals sector. The current medium-term picture continues to indicate the global energy transition will open opportunities across all markets that the company serves. Going forward, the company is focused on delivering the benefits of the acquisition of ECR including the realization of cost, margin and revenue synergies.

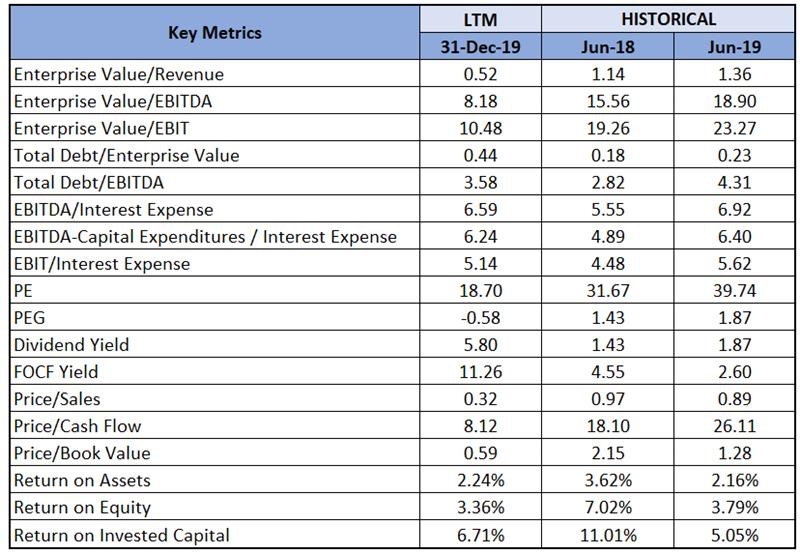

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation(40).png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the last three months, the stock of WOR has corrected by 57.04% on ASX. The stock is currently trading near to its 52-weeks low price of $4.630. In H1FY20, the company observed more consistent earnings through increased proportion in opex, chemicals and North America and Europe. We have valued the stock using EV/EBITDA multiple based relative valuation and arrived at a target upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like Beach Energy Ltd (ASX: BPT), Senex Energy Ltd (ASX: SXY) and CIMIC Group Limited (ASX: CIM), etc. Considering the company’s decent H1FY20 results, synergies expected from ECR acquisition, sector-specific outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $6.850, down by 0.725% on 8 April 2020.

WOR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...