Company Overview - Woolworths Limited is a retail company. The Company's segments include Australian Food and Liquor, which includes procurement of food, liquor and petroleum products, through the brands Dan Murphy's and BWS; New Zealand Supermarkets, which includes procurement of food and liquor products, through approximately 200 Countdown Supermarkets; General Merchandise, which includes procurement of discount general merchandise products, through the brands BIG W and EziBuy; Hotels, which is engaged in the provision of leisure and hospitality services, including food and alcohol, accommodation, entertainment and gaming, and Home Improvement, which includes procurement of home improvement products. It operates over 3,700 stores across Australia and New Zealand, which span food, liquor, petrol, general merchandise, home improvement and hotels. It also operates Cellarmasters, Langtons and winemarket.com.au online platforms. Its brands include Woolworths Supermarkets, Countdown and Thomas Dux.

.png)

WOW Details

Turnaround strategy with customer driven food innovation Centre at Bella Vista:Woolworths Limited (ASX: WOW), Australia’s leading supermarket chain has been recovering this month driven by the group’s growth efforts. The group has been under pressure this year as they have announced the bottom line loss of $972.7 million, due in part to its Masters Home Improvement debacle.

WOW has unveiled a Food Innovators Centre at its Bella Vista headquarters in Sydney’s northwest, wherein the customers could accelerate and drive its new product development. This multimillion-dollar Centre would be used primarily to develop the WOW own brand products, with consumers giving feedback from start to finish. WOW has tapped South African Bazil Stander, to oversee all new food product development in the burgeoning prepared meals market, which is seen as a key factor in the turnaround strategy. The new Woolies development Centre is attempting to recapture its dominant market share while continues to face competition from Coles, as well as German retailer Aldi and incoming chain Lidl.

Expanding product range to enhance performance:WOW has launched its own range of cheap nappies, Little Ones, recently to attract the bargain hungry shoppers, and to battle for the market share in the $90 billion supermarket industry. The Little Ones range is significantly cheaper than the market leader Huggies and was introduced to compete with the other in-house nappy ranges from Coles and Aldi.

On the other side, Woolworths has chosen Bega Cheese to manufacture and pack a range of its private label products including the cheese, UHT, adult milk powder and cream.

Corporate Restructuring efforts to start reaping benefits despite short term pressure:WOW is undergoing restructuring efforts which includes 500 job cuts, 30 stores close down comprising 17 supermarkets in Australia, six supermarkets in New Zealand, four Woolworths metro stores and three hotels. These stores are all expected to shut before the end of the current financial year. The group is also pursuing a sale of EziBuy. Companies like Metcash have been showing interest for acquiring the group’s Home Timber & Hardware Group. Australian Competition and Consumer Commission accepted the bid from Metcash to acquire rival hardware wholesaler Home Timber & Hardware. Meanwhile, WOW has identified five Big W stores that are likely to close in the next three years based on current trading performance. A further 34 stores including 15 supermarkets in Australia and five metro stores across its portfolio are rated as underperforming and there is significant uncertainty around whether WOW would renew the lease at the end of the lease term. WOW is also writing down the value of store assets at another 18 Big W stores, in part due to "onerous lease obligations". WOW has also planned to close its Home Distribution Centre in Victoria in the FY19. Additionally, a further 1,000 workers would be moved from head office directly into the company's business units for better communication between the business and corporate functions. Moreover, WOW has significantly slowed down the rollout of new supermarkets in Australia. As per WOW the cost of restructuring will be $766 million, and nearly $1 billion before tax. The shareholders were welcoming a long overdue change in strategic direction to arrest underperformance and return the business to sustainable operating performance. In addition, WOW has introduced sales per square meter and Return on Funds Employed as long-term performance indicators to drive a new level of accountability, and provide a simple benchmark for evaluating performing or under-performing stores.

On the other side, WOW has a new Group CEO, Brad Banducci who has taken tough decisions to put the company onto track to become number one.

.png)

Stores to be closed before the end of the lease term (Source: Company Reports)

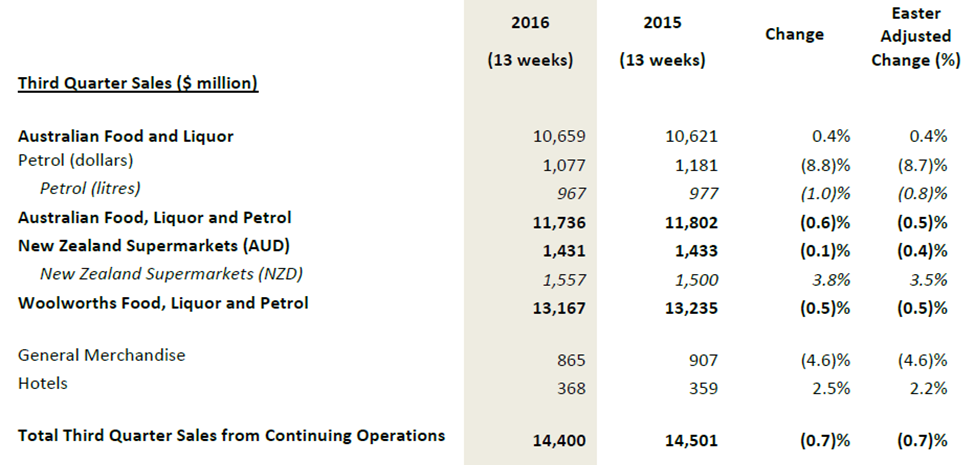

Signs of progress in Australian Supermarkets:WOW is seeing the clear signs of progress in the Australian Supermarkets. There is a record voice of the customer scores, improvement in the team engagement scores and there is a continued transaction growth, with item growth now positive. Accordingly, the group’s Australian Food and Liquor sales for the third quarter of 2016 managed to rise over 0.4% year on year (yoy) to $10.7 billion but the Easter adjusted comparable sales fell 0.9% for the quarter.

However, New Zealand Supermarkets sales for the quarter delivered a decent increase of 3.8% to NZ$1.6 billion against the previous year. Easter adjusted comparable sales increased by 0.6% during the third quarter. On the other side, the group is constantly undertaking significant cost reductions to improve base profitability whilst restructuring the business to build up the direct sourcing and design capabilities to ensure that the new ranges resonate with the customers. As a result, WOW expects a small loss in FY16 in General Merchandise as the company would aggressively clear unproductive summer and current season winter stock.

Third quarter performance (Source: Company Reports)

Credit quality: S&P downgraded its credit rating to BBB (Outlook stable)while Moody’s maintained their Baa2 rating on the stock. On the other hand, WOW is working out to enhance its investment grade credit rating and accordingly undertaking the necessary actions to support the credit profile including the sale of non-core assets, accelerating working capital initiatives and adjusting its growth capital expenditure and property leasing profile. Additionally, WOW has approximately $700m of debt maturing in the second half of FY16 and a further $400m maturing in November 2016. These refinancing requirements have been pre-funded by additional undrawn bilateral bank facilities totaling $1.2 billion with tenors of two and three years, established in November 2015.

Meanwhile, the group reported that they would abandon its Woolworths Dollars rewards scheme in a major overhaul that would bring back customers earning Qantas Frequent Flyer points. WOW is revamping its unpopular $500 million rewards scheme and the scheme is considered as the massive backlash from customer on just nine months after the launch. Under the overhauled scheme, shoppers would earn “Woolworths points”, with one point earned on every dollar spent at Woolworths, affiliated Caltex service stations and BWS bottle shops.

Forecast for FY 16:WOW expects EBIT from the continuing operations before significant items of $2,550 - 2,570 million. BIG W is expected to report a loss of $12 - 17 million and EziBuy is expected to report a loss of $13-18 million before significant items. The operating performance of Endeavour Drinks Group will be disclosed separately in the FY’16 result. ROFE for Endeavour Drinks Group will be reported separately from H1’17.

WOW is coming up with the financial performance result for FY 16 on August 25, 2016. The financials will improve in the coming years due to the corporate restructuring. WOW is expecting significant improvement in comparable sales in Australian Supermarkets in the second half FY 16.

Stock Performance:The shares of WOW rose over 7.7% in the last four weeks offsetting this year to date fall to over 1% (as of August 19, 2016). The group continues to strengthen its Food business to get Customers as well as fight competition and accordingly continues to make investments in the shopping experience, prices, customer service and the quality of its fruit and vegetable offers. WOW expects to invest a further $150 million, predominantly in price, customer service and loyalty, in H2’16. As per recent speculations, Australian Financial Review has indicated that Morgan Stanley has been mandated to sell Woolworths Petrol post news swirling around that WOW might divest businesses to boost its capital position.

Moreover, WOW has begun the implementation of a new group operating model designed to reduce costs, increase the business accountability and improve shared service delivery effectiveness. Based on the foregoing, we give a “Buy” recommendation on this dividend yield stock at the current price of $24.10

WOW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...