Company Overview -

Woolworths Limited is a retail company. The Company's segments include Australian Food and Liquor, which includes procurement of food, liquor and petroleum products, through the brands Dan Murphy's and BWS; New Zealand Supermarkets, which includes procurement of food and liquor products, through approximately 200 Countdown Supermarkets; General Merchandise, which includes procurement of discount general merchandise products, through the brands BIG W and EziBuy; Hotels, which is engaged in the provision of leisure and hospitality services, including food and alcohol, accommodation, entertainment and gaming, and Home Improvement, which includes procurement of home improvement products. It operates over 3,700 stores across Australia and New Zealand, which span food, liquor, petrol, general merchandise, home improvement and hotels. It also operates Cellarmasters, Langtons and winemarket.com.au online platforms. Its brands include Woolworths Supermarkets, Countdown and Thomas Dux.

.png)

WOW Dividend Details

Targeting China opportunity:

Woolworths Ltd (ASX: WOW) recently launched its products Tmall Global, an overseas platform of Alibaba Group’s B2C Tmall business in China, to capture the huge potential opportunity in China, especially from the rapidly growing middle class who are seeking for high quality Australian products. As per a South China Morning report from Hong Kong, the Chinese mainland is estimated to comprise around half of the global retail e-commerce market by 2018 driven by the rising middle class coupled with increasing nationwide adoption of smart mobile devices. eMarketer, a New York-based research firm estimates that the China’s total retail e-commerce sales might surge over 133 per cent to US$1.568 trillion in 2018, as compared to an expected US$672 billion in 2015. This move by WOW would add support to the group’s performance, which has been struggling over the past few periods in the domestic market on the back of rising competition and market slowdown. The group chose eCargo Holdings to support its service operations in the China consumer market.

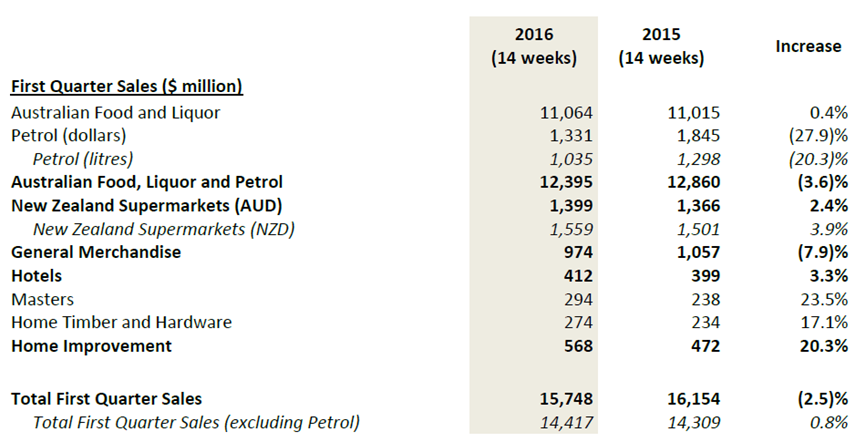

Restructuring Supermarkets business: Woolworths Ltd is making efforts to revamp its Supermarkets business, which comprises over 70% of the group’s profit. The group reported that they infused over $300 million in prices till date (as of November 26, 2015 report) to decrease its prices further to regain its competitive position in the market. Accordingly, WOW launched a new marketing campaign ‘Low Price, ALWAYS’ to attract and retain their customer base as well as relaunched ‘Woolworths Rewards’ to add more value to its loyal shoppers. WOW is enhancing its service level in stores by increasing staff availability and levels of stock availability, having shorter checkout times and upgrading their stores. The improving customer metrics indicate that the group’s efforts started paying off. During the first quarter, the average prices decreased by 1.8%, which includes groceries, produce, bakery and general merchandise items. The group’s Australian Food and Liquor sales segment rose by 0.4% year on year (yoy) during first quarter of 2016 to $11.1 billion. WOW opened six new store openings during the first quarter leading to a total to 967, three (total) Dan Murphy’s reaching to an overall of 199 and seven (net) BWS stores leading to a total of 1,254 (including both standalone and supermarket attached BWS stores). As per New Zealand Supermarkets, division sales rose 3.9% yoy to NZ$1.6 billion during the first quarter, with comparable sales growth increasing to 2.5% yoy in the period driven by the group’s ‘Price Drop’ and ‘Price Lockdown’ programs coupled with Domino Stars collectables Promotion.

.png)

Average price changes (Source: Company Reports)

Exit from the Masters Business: The company announced its intention to exercise its call option over 33.3% interest in Hydrox Holdings Pty Ltd (operates Masters and Home Timber & Hardware) post Lowe’s notice to exercise its put option under the JV. This step comes as a way to resurrect the profits of the group while avoiding any further losses from said business. WOW has been recently focusing on its Master business in order to leverage the highly fragmented growing home improvements market. As a result, WOW delivered a 20.3% yoy rise in its home improvement segment in first quarter of 2016, driven by its Masters as well as Home Timber and Hardware segments. Masters sales surged by 23.5% during the period to $294 million as compared to the earlier year. In fact, this outstanding performance in Master’s earlier raised excitement among investors, as speculations over the segment’s acquisition has been going around. WOW opened four stores in the new format during the quarter in this segment as well as finished the revamp of one store in Victoria. Consequently, the group intended to have around half of its network in the new format by the end of the fiscal year of 2016, as new stores in FY15 continued to deliver better average sales per store of greater than 30%, as compared to its traditional formats. WOW launched several new products in its stores like Honda mowers, Sherwin Williams paint and Loctite adhesives. The group started four Masters Stores in the first quarter of 2016 resulting to the total stores of 62. Meanwhile, the Home Timber and Hardware sales also grew by 17.1% in the first quarter of 2016 to $274 million as compared to the prior corresponding period boosted by store acquisitions’ contribution. Home Timber and Hardware store numbers were maintained at 44 during the quarter.

Focusing on General Merchandise segment: General Merchandise sales reduced by 7.9% during the first quarter of 2016 to $974 million, as compared to $1,057 million in the first quarter of 2015. The comparable sales declined by 8.1% during the period, even though the sales trend improved by the end of the quarter. However, the group reported that their in-stock position became stable during the quarter as their BIG W business transformation and systems implementation issues were resolved. Categories like Party, Books, Baby Consumables, Sleepwear and Underwear have delivered a strong performance while sales of new season fashion also added support. Woolworths made decent efforts in rolling out visual merchandising enhancements to its core destination categories like Party, Toys, Apparel and Children’s wear by launching a refreshed brand campaign with focus on value. Meanwhile, the group’s efforts to clear unproductive inventory is finished during the first quarter, which is well before the original schedule, enabling a free store for inventory aligned to the segment’s new customer strategy. Overall, BIG W and EziBuy stores during the first quarter of 2016 reached 185 and five, respectively.

.png)

New Stores and refurbishments across all the segments (Source: Company Reports)

Outlook: With the group’s strong revamping efforts during the fiscal year, management estimates a strong impact on its margins during the year on the back of huge investments in price and service in the Australian Supermarkets division. As a result, WOW estimates a Net Profit after Tax in the range of $900 million to $1 billion in the first half of 2016, which is 28% to 35% lesser as compared to the WOW’s first half of 2015 Net Profit after Tax before significant items. On the other hand, management is positive over the long term benefits of its growth efforts and expects a major transformation of its business. Meanwhile, the group is also interviewing, for a replacement of CEO for the group. Ralph Waters, Dave Mackay and Christine Cross are also retiring from the group. Recently, Holly Kramer joined WOW, who was the CEO of Best and Less. Roger Corbett is also joining WOW as an advisor adding his strong retail expertise in the Australian market.

First quarter of 2016 performance (Source: Company Reports)

Stock Performance: Woolworths stock has been under pressure since last year, generating a decline by 25.09% (as of January 15, 2016) impacted by the rising competition from its peers especially in pricing coupled with the ongoing tough market conditions. Therefore, the group was able to deliver a sales rise (excluding Petrol) of only 0.8% yoy to $15.7 billion during the first quarter of FY16. On the other hand, WOW is investing to improve its pricing, service, stock availability as well as the format of the stores to regain its customer base as well as drive more value to the group’s loyal shoppers. Woolworths China e-commerce entry might also add support to this struggling retailer. Despite the management’s weak outlook for FY16, WOW’s growth efforts across all of its businesses are expected to be paid off in the long term. Further, the update on the Masters business has lifted the stock performance to some extent. Moreover, the stock is also trading at a relatively cheaper valuations, with a relatively low P/E as compared to its competitors and has a strong dividend yield. Long term investors seeking for bargain dividend opportunities can leverage the recent correction of over 19.93% in the last six months (as of January 15, 2016) in WOW stock. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $23.65

.png)

WOW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...