Company Overview - Woodside Petroleum Ltd (Woodside) is an oil and gas company. The Company is engaged in hydrocarbon exploration, evaluation, development, production and marketing. It operates in three segments: Producing comprising North West Shelf (NWS) Project, Pluto Liquefied Natural Gas (LNG) and Australia Oil; Development comprising Browse floating liquefied natural gas (FLNG) and Wheatstone LNG, and Other. Its Other segment comprises the activities undertaken by trading and shipping, the United States, Exploration, International, Canada and Sunrise Business Units. Its North West Shelf Project is engaged in the exploration, evaluation, development, production and sale of liquefied natural gas, pipeline natural gas, condensate, liquefied petroleum gas and crude oil from the North West Shelf ventures. Its Pluto LNG project is engaged in exploration, evaluation, development, production and sale of liquefied natural gas and condensate in assigned permit areas.

.png)

WPL Details

Acquisition of half of BHP Billiton’s Scarborough area assets: Woodside Petroleum Limited (ASX: WPL) has entered into binding sale and purchase agreements with BHP to acquire half of BHP Billiton’s Scarborough area assets in the Carnarvon Basin, located at offshore Western Australia. The deal would complement WPL’s growth strategy and would leverage the company’s deep water production and LNG capabilities. The acquisition includes a 25% interest in WA-1-R for which ExxonMobil is the operator and a 50% interest in WA-62-R, which together would comprise the Scarborough gas field. The group would also acquire a 50% interest in WA-61-R and WA-63-R which contain the Jupiter and Thebe gas fields. Meanwhile, WPL has agreed the deal for $400 million which consists of US$250 million on completion of the transaction and a contingent payment of US$150 million upon a positive final investment decision to develop the Scarborough field.

The Scarborough area assets including the Scarborough, Thebe and Jupiter fields are estimated to contain the gross 8.7 trillion cubic feet of gas resources at the 2C confidence level. WPL’s net share of the resources is estimated to be 2.6 trillion cubic feet of gas. The group is targeting completion of the transaction by the year-end 2016. However, the acquisition is subject to the pre-emption rights, FIRB clearance and NOPTA approval and registration. The resources would then be booked by WPL as contingent resource after the completion.

.png)

Asset Overview (Source: Company Reports)

Financial Performance of 1H 2016: WPL has reported a net profit after tax which was 50% lower to US$340 million in the first half 2016 as compared to the first half of 2015. This decline in bottom line was mainly due to lower prices, with benchmark oil prices falling 46% from 1H 2015 to 1H 2016. The Brent oil price reached cycle lows of US$28/bbl at the start of 2016. The lower sales revenue is partly offset by lower production costs. The first half sales revenue was 22% lower than in 1H 2015 to $1.8 billion mainly due to lower average realized prices, partly offset by higher sales volumes and favorable price review outcomes. WPL has reported a 9% increase in the production volume to 45.9 MMboe in the 1H 2016 against first half of 2015, primarily due to higher LNG capacity and availability. Pluto LNG annualized loaded production rate was of 4.9 mtpa (total project), which was 14% higher than expected at FID in the 1H 2016.

Additionally, WPL average realized LNG price of the portfolio was US$7.66/MMbtu in the first half of 2016. WPL’s half-year unit production costs were 38% lower than 1H 2015 to US$5.2/boe. Meanwhile, WPL has executed major North West Shelf (NWS) Project with planned onshore and offshore turnaround ahead of the schedule and this is as per the budget. WPL has delivered the NWS Train 4 turnaround in 23 days which is 8 days ahead of the schedule.

.png)

1H 2016 Financial Performance (Source: Company Reports)

WPL’s Strategy to fight the ongoing tough market conditions:WPL is operating in a challenging low commodity price environment; therefore, WPL has increased the liquidity, improved the debt maturity profile flexibility, reduced their cost structure and has concluded numerous price reviews. WPL is progressing the term sales while growing the business through exploration and acquisitions.

Moreover, WPL has increased the 2016 production guidance to 90–95 MMboe. WPL has de-risked their 2017 to 2018 revenue stream with 85–90% of the expected production while their under term contract is subject to finalization of sale and purchase agreements. In addition, WPL has secured over $600 million in funding at competitive rates. The group does not have near-term debt maturities and has a liquidity of $2 billion.

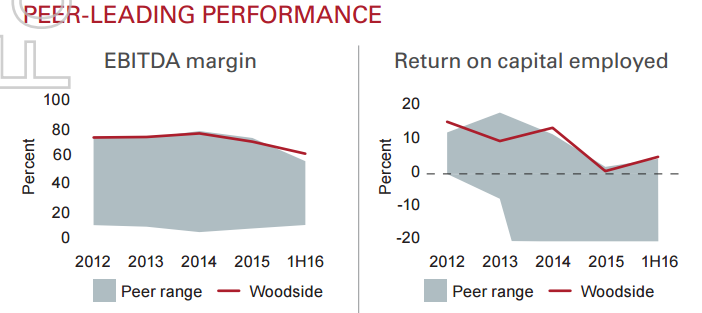

Peer-leading Performance (Source: Company Reports)

Developments in WPL’s Projects till date:The Wheatstone Project in which WPL is 13%, non-operator is on track for the first LNG from Train 1 in mid-2017. The first LNG production from Train 2 is expected 6-8 months later. The Julimar Project in which WPL has 65% stake is as per the budget and is on schedule to be ready for start-up in the second half of 2016. The North West Shelf plateau extension work is progressing well. The Persephone Project is as on track with the budget with a revised earlier start-up expected in 2H 2017 and GWF-2 is on track for start-up in 2H 2019. Additionally, WPL has approved the Greater Enfield Project for developing oil reserves (2P) of 41 MMbbl (Woodside share) as a tie-back to the Ngujima-Yin FPSO, targeting the first oil mid-2019. The discoveries at offshore Myanmar in the Block A-6 (Shwe Yee Htun-1) and the Block AD-7 (Thalin-1A) have enhanced the contingent resources by 83 MMboe (Woodside share, 2C). In addition, WPL has agreed to acquire ConocoPhillips Senegal B.V., a company that holds a 35% interest in the 560 MMbbl SNE deep water oil discoveries (100%, at the 2C confidence level). WPL has entered into an agreement to acquire a 65% participating interest and operatorship of AGC Profond Block in Senegal – Guinea-Bissau.

WPL has expanded the acreage position offshore Gabon by acquiring a 40% interest in the Luna Muetse Block. Moreover, WPL has continued progressing work on reducing the capital cost at the Kitimat LNG Project in British Columbia. The appraisal drilling of the Liard resource has continued with well’s performance exceeding the initial expectations. WPL is successful in rebalancing the global exploration portfolio and plans to drill a series of wells in 2017.

Expanding pipeline: WPL has

signed a heads of agreement with Pertamina for the supply of 0.5 to 1.0 mtpa of LNG starting in 2019 for a period of 15–20 years. The heads of agreement is conditional on the negotiation and execution of a fully termed LNG sale and purchase agreement (SPA). WPA has executed ten additional NWS LNG contract price reviews and continues to work with customers to achieve mutually beneficial outcomes. The price review outcomes have maintained strong oil price linkage and WPL has achieved about US$50 million in additional reconciliation payments and other commercial benefits. Moreover, WPL has executed agreements necessary to enable equity lifting of NWS uncommitted LNG and domestic gas volumes. The uncontracted LNG and domestic gas volumes have been equity lifted from 1

st July 2016 which provides additional portfolio scale and flexibility. The existing sales contracts would continue to be managed jointly on behalf of the NWS Project participants.

Additionally, WPL has added one LNG carrier to the shipping fleet in the first quarter 2016, increasing it to four comprising of two portfolio vessels and two dedicated Pluto vessels. The expanded shipping fleet provides additional capacity and flexibility to manage a diversifying customer base including in Egypt and India. On the other side, WPL has also affirmed investment grade credit ratings. Therefore, the credit ratings of Baa1 and BBB+ were reaffirmed by Moody’s and Standard & Poor’s, respectively.

Stock Performance:The shares of WPL stock rose over 6.1% in the last three months (as of September 06, 2016). The group has declared an interim dividend of 34 cents per share while the Dividend Reinvestment Plan has been suspended for the interim dividend by WPL. We believe that the stock would continue to rise given its LNG production consistently exceeding the original design capacity.

WPL’s low cost of the operations and the continued focus on cost reduction together positions them to sustain the volatile oil market. WPL has a strong balance sheet and is in a robust position to leverage the better oil price forecasts for 2017. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $28.46

WPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...