Company Overview - Woodside Petroleum Ltd (Woodside) is an oil and gas company. The Company is engaged in exploration, development and production of hydrocarbons. The Company operates in five segments: North West Shelf Business Unit, Pluto Business Unit, Australia Oil Business Unit, Browse Business Unit and Others. North West Shelf Business Unit segment develops, produces and sales liquefied natural gas (LNG), pipeline natural gas, condensate, liquefied petroleum gas and crude oil. Pluto Business Unit segment develops, produces and sales liquefied natural gas and condensate in assigned permit areas. Australia Oil Business Unit segment evaluates, develops, produces and sales crude oil in assigned permit areas. Browse Business Unit segment evaluates and develops liquefied natural gas and condensate in assigned permit areas. Other segment consists of activities undertaken by the trading and shipping, United States, exploration, International and Sunrise Business Units.

.png)

WPL Dividend Details

Improved production driven by Balnaves oil asset: Woodside Petroleum Ltd (ASX: WPL) reported a fourth quarter production volume rise by 6.4% as compared to the prior corresponding period (pcp) driven by Balnaves oil asset production, which was started in April 2015. Pluto LNG’s enhanced contribution of LNG and condensate volumes also drove the overall production on the back of better plant reliability. Sales volumes also improved by 4.6% year on year (yoy) during the quarter indicating the timing of shipments. On the other hand, sales revenues fell by 37.3% during the fourth quarter against pcp impacted by the ongoing decrease in realized prices across the portfolio. Moreover, the group’s production volumesfell by 1.6% during the quarter against the previous quarter on the back of natural reservoir decline impact on the volumes from the Balnaves oil asset. Nonetheless, sales revenue increased by 1.7% yoy to $ 1,105 million during the fourth quarter of 2015 over the previous quarter as better LNG and condensate sales volumes had partially offset the oil prices pressure and Balnaves oil asset contribution.

.png)

Fourth quarter production (Source: Company Reports)

Focusing on costs savings while maintaining the value for development activities: Woodside Petroleum is focusing to achieve cost efficiency in order to offset the ongoing commodity prices pressure on its revenues. Accordingly, for its Browse FLNG project, WPL was able to enhance the project value despite costs reduction while developing its front-end engineering and design (FEED) phase. On the other side, the estimated final investment decision (FID) is due on second half of 2016, and the FLNG development and commercialization related activities are on track. As per the group’s Wheatstone highlights, this project includes Wheatstone and Iago fields, an offshore platform and a pipeline to shore and the onshore plant. This project’s progress is also on track with the development being finished > 65%. The forecast for first LNG from Wheatstone has been indicated to be mid-2017 (about six-month delay). The Julimar Project, operated by WPL is also more than 80% complete and on track to start by the second half of this year. With regards to the Greater Enfield Development progress, the initial Field Development Plan was given to the government for approval during the quarter while the offshore geophysical, geotechnical and environmental surveys were finished. Based on the development proposal, the tie-back of the Laverda Canyon, Norton over Laverda and Cimatti oil accumulations are involved via a 31 km flowline to the Ngujima-Yin floating production storage and offloading (FPSO) vessel, targeting a gross (100%) contingent resource (2C) of 70 MMboe (net Woodside share of 42 MMboe). The group started drilling at Persephone in North West Shelf project during fourth quarter of 2015 while Platform modifications and fabrication of key subsea infrastructure at the North Rankin Complex were also performed in the fourth quarter. This project’s development activities were on track to start by early of 2018. Recently,NWS Project participants received approval for US$2.0 billion project (100%) for the development of the Greater Western Flank Phase 2 Project, targeted to progress a gross (100%) proved plus probable (2P) reserves of 1.6 Tcf raw gas (net Woodside share ~270 Bcf) from the combined Keast, Dockrell, Sculptor, Rankin, Lady Nora and Pemberton fields via subsea infrastructure and a 35 km pipeline linking to the present Goodwyn A platform. Gas delivery from this project is forecasted to start by second half of 2019 from five wells in the Lady Nora, Pemberton, Sculptor and Rankin Fields, while the rest of the three wells in the Keast and Dockrell fields are projected to begin production from the first half of 2020. Woodside’s international development activities at the Kitimat LNG Joint Venture delivered its first development scale appraisal well (D-A28-B) into production during the fourth quarter while the second development scale appraisal well (B-B03-K) was finalized and would be brought into production by early 2016.

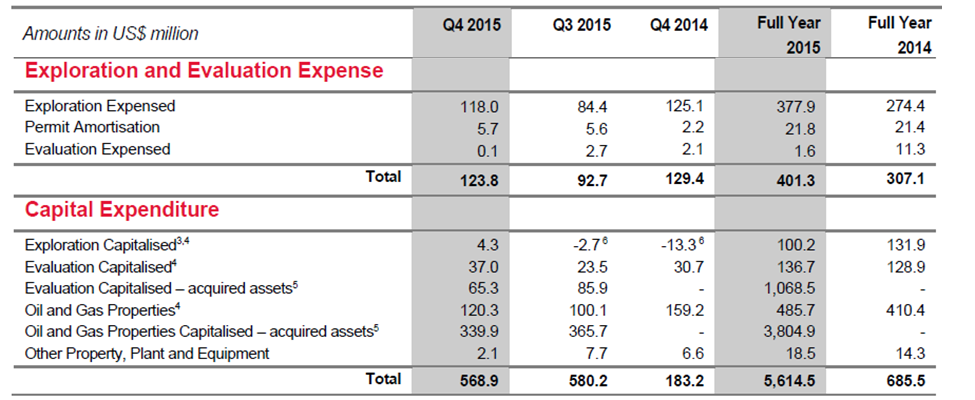

Exploration expense and capital expenditure in fiscal year of 2015 (Source: Company Reports)

Positive exploration activities contributing to the group’s strong asset base:WPL has been generating positive exploration results leading to a potential boost of its assets in the long term. Recently, the group reported that they found gas at the Shwe Yee Htun-1 exploration well located in the Block A-6 in the Rakhine Basin, Myanmar. The discovery of gas and reservoir quality rock significantly de-risks the petroleum system, as well as identified leads in the block and in the group’s adjacent acreage. Around 15 m of net gas pay was interpreted within the principal target interval, while the net gas pay rose to over 32 m post the completion of nuclear magnetic resonance and resistivity image logging, formation fluid sampling and pressure testing. In January of this year, Thalin-1 well in Block AD-7 was spudded and the group conducted wide 2D and 3D seismic surveys (with gravity and magnetic data acquisition) over Blocks A-4, A-7, AD-2 and AD-5 commenced during the second half of 2015 and intends to continue the program in the second quarter of 2016. Programs of wide seabed coring in these blocks were also estimated to begin this year. Moreover, the AD-7 Production Sharing Contract was revised during the quarter aiming for the expansion of Block AD-7, adding 1,100 km

2 (70%) to the Block’s area. On the other side, as per the Australia exploration activities, WPL intends to drill two oil targets in permit WA-472-P in the Beagle Sub-basin and is planning to spud the Skippy Rock-1 well during the first quarter of 2016 to aim a lesser Triassic structure. Meanwhile, Woodside acquired 1,074 km of 2D seismic data at the Rabat Ultra Deep Offshore Reconnaissance License (at Morocco) during the third quarter of 2015 and estimates the final data delivery by first quarter of 2016. Processing of the Tangiers 3D marine seismic survey (over 7,000 km

2) at Canada (Nova Scotia) was on the verge of completion by fourth quarter of 2016. With regards to the Republic of Korea exploration highlights, the Hongge-1 exploration well was spudded during September 2015 leading to an overall depth of 3,900 m. Therefore, based on the drilling results, the presence of a petroleum system with a substantial gas column within the primary target was confirmed.

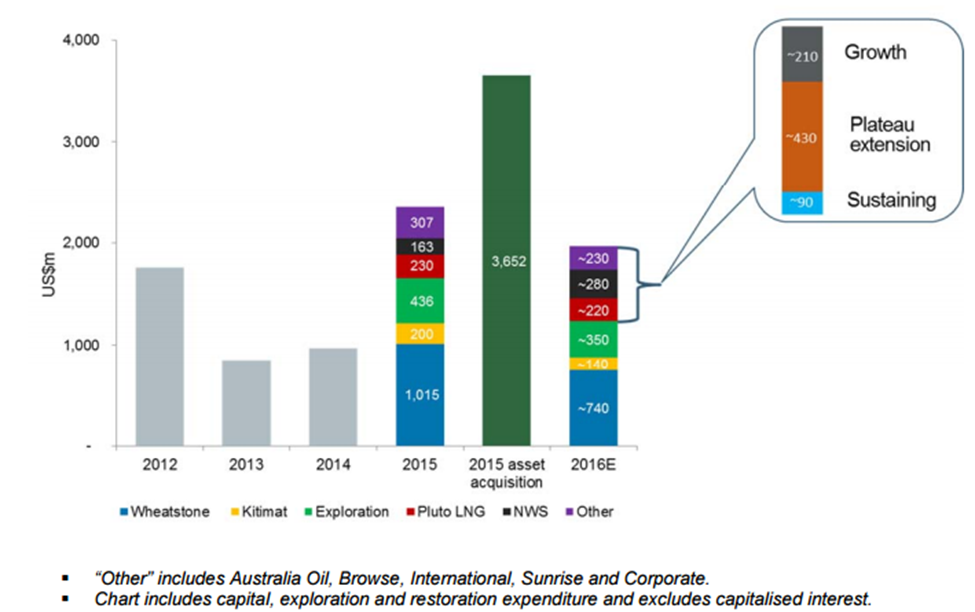

2016 Investment Expenditure Outlook (Source: Company Reports)

Guidance: The group forecasts a lower production during 2016 fiscal year which is in the range of 86 to 93 mmboe as compared to the 2015 fiscal year.The forecasted production comprises over 42% contribution from Pluto LNG, followed by 25% contribution from NWS LNG, 14% contribution from NWS pipeline natural gas, 18% from condensate, oil and LPG, and finally just 1% contribution from Canadian pipeline natural gas. This production estimate in 2016 includes no planned turnaround from Pluto LNG during 2016. Meanwhile, the overall decrease in production was impacted by the decrease in oil assets across the field (which is a 3.8 mmboe impact). Even NWS pipeline natural gas production is estimated to be decreased by 0.8 mmboe on the back of the decrease in customer demand. On the other hand, WPL expects an overall investment expenditure forecast of over USD 1.96 billion (without post FID expenditure for Browse LNG) during fiscal year of 2016, which is much lower as compared to the pcp.

Outstanding dividend yield: The shares of WPL plunged over 21.68% (as of February 09, 2016) in the last six months due to the ongoing commodity prices pressure on the group’s top line performance. Moreover, investors are also concerned over the group’s performance due to the natural reservoir decline impact coupled with the decrease in LNG demand. On the other hand, WPL is generating positive exploration results, promising strong long prospects with regards to the group’s assets. Further, even with the delay in Wheatstone project, the upstream component that is the Julimar project is proceeding well and WPL’s share in budget increase owing to the downstream component may not be huge (13% stake in the LNG facility and in LNG sales). The budget fluctuation has more or less been shielded by the lower AUD up till now.

Woodside is also aggressively controlling its investment expenditure in 2016 as well as focusing on cost savings to offset the top line pressure to a certain extent. Meanwhile, the heavy correction in WPL placed the stock at cheaper valuations, which is trading at a low P/E while offering a very attractive entry opportunity to investors against its peers. WPL also has an outstanding dividend yield. We remain bullish on the stock and reiterate our “BUY” recommendation on WPL at the current price of $26.48

WPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...