Company Overview - Woodside Petroleum Ltd (Woodside) is an oil and gas company. The Company is engaged in exploration, development and production of hydrocarbons. The Company operates in five segments: North West Shelf Business Unit, Pluto Business Unit, Australia Oil Business Unit, Browse Business Unit and Others. North West Shelf Business Unit segment develops, produces and sales liquefied natural gas (LNG), pipeline natural gas, condensate, liquefied petroleum gas and crude oil. Pluto Business Unit segment develops, produces and sales liquefied natural gas and condensate in assigned permit areas. Australia Oil Business Unit segment evaluates, develops, produces and sales crude oil in assigned permit areas. Browse Business Unit segment evaluates and develops liquefied natural gas and condensate in assigned permit areas. Other segment consists of activities undertaken by the trading and shipping, United States, exploration, International and Sunrise Business Units.

Analysis - The strategy of the company, which has been effective and continues to be unchanged, is based on three prongs which are related. The first is to maximise the core business by maximising the operating effectiveness, building a culture of continuous improvement, extending the life of existing assets and developing resources for contingencies. The second is to leverage capabilities by utilising the complete value chain for LNG, deepwater drilling, FPSO's subsea technology and making the most of market relationships in Asia. The third prong is to grow the portfolio by developing opportunities to diversify and optimise as well as value chain initiatives and to aggregate positions in existing areas of focus by rebalancing and acquiring high-quality assets in the current low price oil environment.

Key Highlights (Source - Company Reports)

Key Highlights (Source - Company Reports)

The strategy is transforming business. From June 2011, the main points were focussed on North West Australia, Pluto LNG is behind schedule, safety performance which lagged industry, point to point sales strategy focused on Japan and limited activity on mergers and acquisitions. Now the highlights are an expanded portfolio of global exploration, browse FLNG approaching FEED, the best ever performance on safety, LNG reliability which is world class, enhanced capabilities for marketing and a shift to selling portfolios. More than $ 5.5 billion worth of transactions have been executed which is around 20% of market capitalisation.

There are several near-term catalysts for portfolio growth. Browse FEED entry is anticipated in the middle of 2015, Wheatstone is aiming at first gas by late 2016, the appraisal of upstream in Kitimat will be targeting cost reductions, Greater Enfield is accelerating FEED to take advantage of market conditions, exploration drilling will be carried out in the next 16 months on prospects with high potential and, finally, acquisitions are being actively sought to capitalise on the current low price environment.

The strong financial position of the company is reflected in the reaffirmation of credit ratings with a stable outlook, the unchanged target for the dividend payout ratio, the refinanced balance sheet on better terms to manage the low oil price environment and continued focus on growth and returns. The future focus will consist of aggregation of opportunities in existing focus areas, the de-risking of future growth through the acquisition of Wheatstone, the increased upside as a result of the purchase of Kitimat and organic growth through Browse and Greater Enfield. There are also additional upside opportunities through routes such as exploration and marketing.

The financial position

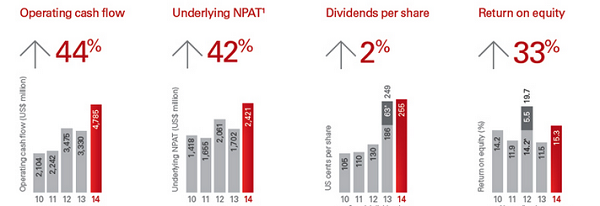

2014 was a record year in many respects. Production was a record 95.1 MMboe, reported NPAT $2.4 billion,the return on equity 15.3%,free cash flow $4.2 billion and the full-year dividend was a record use the $ 2.55 per share.Liquidity amounted to $6.8 billion cash holdings stood at $3.2 billion and undrawn debt was $ 3.6 billion. The strong operating cash flows combined with the lower investment spending put the company in a much better position to cope with the spell of low oil prices.

Strong Operating Cash Flow (Source: Company Reports)

The first-quarter returns from the world-class asset portfolio are well in excess of the cost of capital as well as the company's peers and reflect the disciplined nature of the investment as well as the high quality of the portfolio. This can be seen from the following diagram:

First quartile results from a world class asset portfolio (Source: Company Reports)

Capital management and dividend cover

First quartile results from a world class asset portfolio (Source: Company Reports)

Capital management and dividend cover

The approach to capital management remains the same and the priority is cash generation by disciplined capital management combined with cost reduction. For the foreseeable future, the dividend ratio will be maintained at 80% and liquidity will be a priority as well as access to capital to fund growth. The strong investment grade credit rating will be maintained and the target will be 25% gearing in the range of 10% to 30% throughout the investment cycle. Investment decisions will be based not merely on the growth in production but the creation of value for investors. Cash allocation will be prioritised on the basis of debt servicing, maintaining dividends, sustaining and growth of capital expenditure and the return of surplus cash to investors.

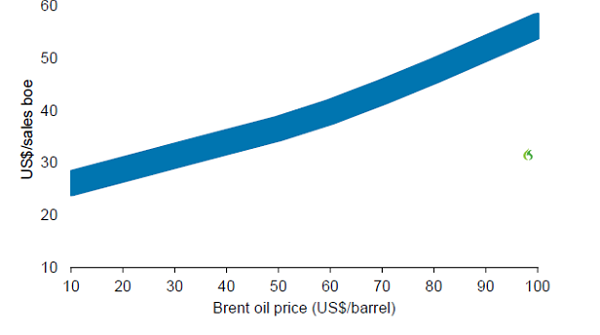

Relationship between Brent oil prices and LNG revenues

The contract portfolio provides the best possible protection in the environment of low oil prices and the LNG sales volume mix for 2015 is forecast to comprise of contract volumes in excess of 90% with spot sales making up up to 10%. The exposure to spot sales is expected to be up to 10% for 2016. The gas business is expected to remain cash positive even at low prices of oil and the gross cash costs for 2015 are expected to be in the range of $ 9 to $ 12/boe. The gas business is also expected to account for 85% to 90% by volume.

Woodside contracted LNG revenue sesitivity to Brent Price (Source - Company Reports)

Woodside contracted LNG revenue sesitivity to Brent Price (Source - Company Reports)

Consequently, cash flow generation is expected to be significant even at low oil prices such as $ 65/bbl flat nominal Brent oil prices. The operating cash flow is expected to be an average of around $ 2.7 billion for the next four years and this is adequate to finance the expected dividends as well as the investment expenditure. The low level of committed investment expenditure is expected to provide a high degree of flexibility. At less than $ 500 million annually, this flexibility will ensure that the expenditure can be controlled to meet developments and take advantage of market conditions and provide the funding for possible acquisitions. The forecast expenditure for Wheatstone is expected to remain unchanged from the economics of purchasing.

Woodside gas unit gross cash margins at different Brent prices (Source - Company Reports)

Funding and productivity

Woodside gas unit gross cash margins at different Brent prices (Source - Company Reports)

Funding and productivity

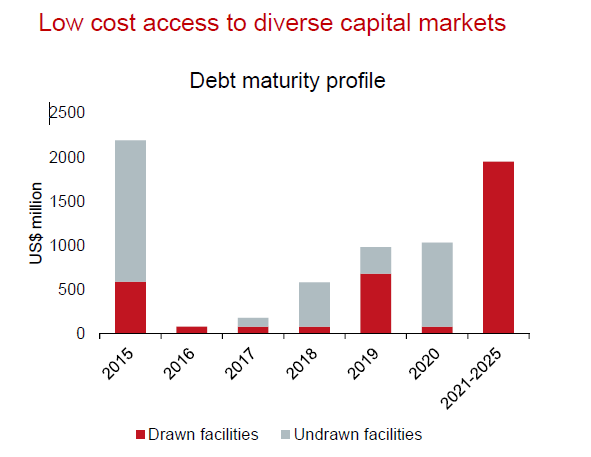

The company has the advantage of low-cost access to diverse sources of capital. There is strong continuing support from the debt markets and $ 2.75 billion have been raised from bonds and banks in the year 2015 so far. The pre-tax portfolio cost of debt has declined from 3.4% per annum in May 2014 to 2.6% per annum in May 2015. The current levels of liquidity provide plenty of options and the position as at 30 April 2015 is $ 3.5 billion made up of cash of $ 200 million and undrawn debt of $ 3.3 billion.

Debt maturity profile (Source: Company Reports)

Debt maturity profile (Source: Company Reports)

In terms of cost and reliability management to create value, the target for 2016 compared to the actuals for 2014 are volume growth of 3% to 5% compared to 5%, a reduction of 10% to 20% on spending compared to reductions of 13% and 10% respectively in operating and capital expenditure, and a reduction of 10% to 20% in process improvements compared to more than 300 in 2014. The company is on target to create benefits of $ 800 million by the end of 2016 having realised $ 560 million in 2014. The organisational savings have now reached 20% on redundancies in 2015. The low prices of oil make it critical to achieve these structural changes in overall costs.

The cost reduction program

The aggressive cost reduction program has an emphasis on accelerated delivery of reduction in external spending with sustainable outcomes. With the objective of achieving structural cost changes, the company has targeted $ 680 million in savings and, of the more than 500 initiatives, more than 100 have been delivered with a value of $ 200 million.

Cost Reduction Program (Source: Company Reports)

Cost Reduction Program (Source: Company Reports)

First-quarter report for 31 March 2015

Among the highlights of the quarter were the issue of $ 1 billion in corporate bonds from the US 144 A bond markets with a tenor of 10 years and a coupon rate of 3.65%. BROWSE completed the FEED readiness check which is an important milestone in preparing for entry.Subsequent to the end of the quarter, on 2 April, the binding transaction to acquire Apache’s Wheatstone LNG and Balnaves oil project interests closed.On 8 April, the company advised the market that the Pyxis-1 exploration well in production licence WA-34-L had intersected approximately 18.5 metres of net gas.On 10 April, the binding transaction to acquire Apache’s Kitimat LNG project interests closed.

WPL Daily Chart (Source - Thomson Reuters)

WPL Daily Chart (Source - Thomson Reuters)

The company has reported outstanding results for 2014 with record earnings which allowed the company to clear most of its debt while providing a trailing dividend yield of almost 9%. Even though we expect operating earnings to drop as a result of the impact of lower oil prices and production, operating earnings continue to remain strong and support an attractive dividend. The company has taken all the necessary steps to ensure growth despite the low oil price environment and we expect to continue to see an upside in the stock price in addition to an attractive dividend. We put a BUY recommendation on the stock at the current price of $35.83.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...