Company Overview - Whitehaven Coal Limited (Whitehaven Coal) is an Australia-based company engaged in coal mining industry. The Company is a coal producer in New South Wales' Gunnedah Basin. Whitehaven Coal owns three operating open cut mines at Werris Creek, Tarrawonga and Rocglen, the Narrabri North underground mine and Maules Creek Project. The Company also has interests in Vickery open cut project near its other open cut mines. The Company also has various exploration assets in New South Wales and Queensland. The Company's projects include Canyon, Maules Creek Project, Narrabri North, Rocglen, Sunnyside, Tarrawonga, Vickery Project and Werris Creek. The Company's other projects include Ferndale Project, Dingo Project, Sienna Project and Ashford project (Bonshaw). The Company operates in two reportable segments: Open Cut Operations and Underground Operations.

Analysis - WHITEHAVEN COAL LIMITED(ASX:WHC) has recently reported that its Coal Resources improved by 182Mt or 4.7% to 4037Mt in August 2015, as compared to 3855Mt in the corresponding period of last year. But the coal Reserves declined to 874Mt in August 2015 while the Marketable Reserves for Group reduced by 12Mt to 789Mt as compared to August 2014 Coal Resources and Reserves. Meanwhile, the total open cut Coal resources were stable at Vickery but the resource categories were upgraded on the back of revised geological model as well as a thorough assessment of historical drilling data. The Vickery Project’s Underground Coal Resources rose by 201Mt driven by the granting of EL8224 and the addition of results from drillings conducted during 2014. However, the Coal Reserves at Narrabri, Maules Creek, Tarrawonga, Rocglen and Werris Creek decreased impacted by the mining depletion.

2015 Operation and Financial Performance

-

Solid ROM and Saleable coal production in FY15: Whitehaven’s ROM coal production witnessed a strong increase to 12.21 Mt during the 2015 fiscal year as compared to 9.2 Mt in 2014 fiscal year, driven by Maules Creek and Narrabri mine’s rise in productions. The Maules Creek project delivered 1.96 mt during the year, while the Narrabri witnessed several production records in FY15 and hence generated an increase of 36% in the production, reporting a 5.4 mt ROM coal production for FY15, as compared to 3.9 mt in FY14. However, the open cuts production declined 7% on a year over year basis to 4.9 mt. As per the coal sales highlights, the group’s coal sales improved by 24% on a year over year basis to 10.9 mt in FY15, against 8.7 mt in FY14, driven by the first pre-commercial ROM coal production from Maules Creek. Narrabri Coal sales increased 37% to 4.95 mt in FY15 as compared to 3.6 mt in FY14. But, the open cuts coal sales plunged 11% on a year over year basis to 4.5 mt. This decrease in in line with the group’s estimations. Meanwhile, WHC undertook some procurement benefits, new rosters and operating initiatives for the open cuts during the year.

.PNG)

Production highlights by segments (Source: Company Reports)

-

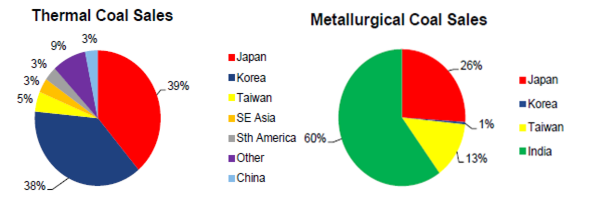

Financial Highlights: Whitehaven reported a revenue increase of only 1% to $763.3million in FY2015, as compared to $755.4m in FY14 in spite of solid production. The falling average realized selling prices (which decreased 7% on a year over year basis) impacted by the declining world crude oil prices had offset the increasing volumes. The average realized selling prices decreased to $80 per tonne in FY15 against $86 per tonne in FY14, while the average USD coal prices fell 16%, but the AUD by USD exchange rate improved by 8%. The group sold around 82% of the thermal coal to Asian markets, while Japan and Korea represented 39% and 38% of the overall thermal coal sales in FY15 respectively. WHC improved its revenue mix of higher margin metallurgical coal product to 35% against 20%, driven by the higher thermal coal quality from Maules Creek production. Korea and India continue to be the target markets by WHC for its metallurgical coal in the future.

Coal Sales by region (Source: Company Reports)

-

Cash flow highlights: Whitehaven improved itsoperating cash flowsby 97% yoy to $213.4 million in FY15, driven by improving EBITDA before significant items by $39.9 million to $130.3 million in FY15 as compared to $90.4 million in FY14. Moreover, WHC also received a refund of $42 million of income taxes on the back of positive resolution of a claim for accelerated deductions at Maules Creek, and $25 million refund related to similar deduction for Narrabri. On the other hand, the Investing cash outflows rose $116.5 million to $436.4 million as at June 30, 2015, due to construction expenditures incurred for Maules Creek project, Narrabri development costs and longwall second shearer as well as BSL deposit payments. The Werris Creek and Gunnedah rail loops upgrade to cater 30 tonne axle loads also added to the expenditure. On a lighter note, around 50% of the group’s cash investments were funded through cash generated by operations. Meanwhile, WHC used $275 million from the senior debt facility in FY15.

WHC Daily Chart (Source - Thomson Reuters)

Outlook

WHC Daily Chart (Source - Thomson Reuters)

Outlook

-

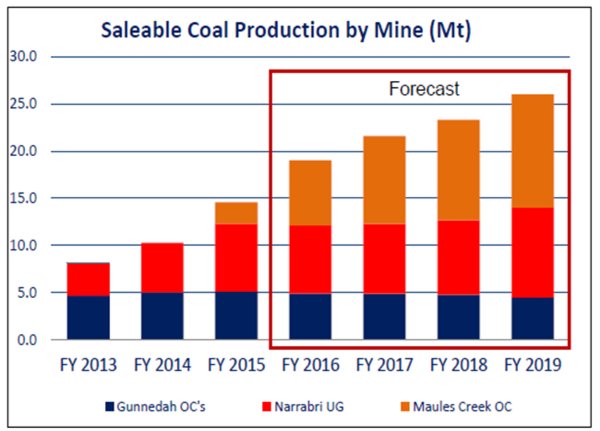

Maules Creek, Narrabri and open cut Outlook: Maules Creek project started delivering coal in December 2014, and has the capability to generate an annualized design capacity of 13mtpa saleable coal when fully operated, which would subsequently double Whitehaven’s coal production to over 23Mtpa by 2018, enabling the group to become the major independent coal producer in Australia. Whitehaven intends to steadily add employees and equipment’s like excavators and trucks at Maules, to gradually improve its mining production to an annualized rate of around 8.5Mt for the December half of FY2016, from an annualized rate of 6Mt production during the June half of FY15. The group also saved around $27 million during the construction phase, against the initial forecast of $767 million. Meanwhile, WHC’s Narrabri production was also 30% more than the design capacity of 6Mtpa during FY15, which delivered 7.7Mt ROM coal and 19,800 meters respectively. Improved productivity from employees, software upgrades to the longwall has helped the group to reduce production costs, placing it among the lowest cost mines. As a result of record production rates during FY15, WHC estimates two full longwall changeouts for FY16 and hence expects FY16 production to be less than FY15 production for Narrabri. The group would take a verdict to widen the longwall face to 400 meters, against the present 300 meters, in September quarter 2015. Meanwhile, open cuts production is expected to be at present levels in the coming three years before Reserves at Rocglen are exhausted in FY19. On an overall note, WHC expects its total production from all the mines to reach over 19.4Mt ROM coal in the next two fiscal years.

Coal Production estimates by segment (Source: Company Reports)

-

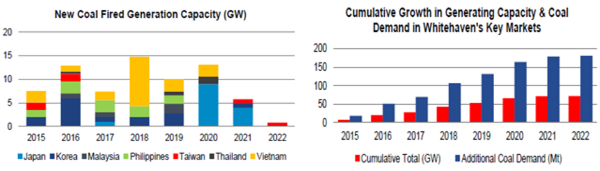

Market Opportunity: WHC wants to become the premier independent coal company in Australia. Accordingly, the solid production growth, underlying cost reductions as well as productivity enhancements led the group to achieve the lowest cost quartile of the current coal industry cost curve. The restricted product availability in the higher quality segment of the seaborne thermal coal market is also adding price support to the group, and WHC expects this price support to continue. Overall, we believe that Whitehaven is well positioned to address the demand for high quality coal requirement, wherein around 180Mtpa of high quality coal should be supplied to address around 70 GW of new capacity which would be added by 2022.

Whitehaven’s market opportunity (Source: Company Reports)

-

Stock Performance: The shares of WHC had recently touched its multi-year low levels as investors were not able to digest just 1% yoy revenue growth during fiscal year of 2015. Moreover, the stock has been under pressure from quite some time now, posting a negative year to date returns of around 23.6%, and fell more than 40% over the last fifty two weeks owed to the falling commodity prices. However, we believe that the ramping up production from Malules Creek project, cost optimization and focus on high quality coal would drive the stock higher in the coming months. Moreover, the stock is already oversold and offers attractive levels to risk taking investors. Accordingly, we give a “BUY” recommendation on WHC at current price levels of $1.25.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...