Company Overview: Westpac Banking Corporation is a banking organization. The Company provides a range of banking and financial services in markets, including consumer, business and institutional banking and wealth management services. The Company is engaged in the provision of financial services, including lending, deposit taking, payments services, investment portfolio management and advice, superannuation and funds management, insurance services, leasing finance, general finance, interest rate risk management and foreign exchange services. The Company's segments include Consumer Bank, Business Bank, BT Financial Group (BTFG), Westpac Institutional Bank (WIB) and Westpac New Zealand. The Company has branches throughout Australia, New Zealand, Asia and in the Pacific region. The Company through its division offers its services under various brands, such as Westpac, St.George, BankSA, Bank of Melbourne and RAMS brands.

.png)

WBC Details

Decent Fundamentals on Track Amidst Certain Challenges: Westpac Banking Corporation (ASX: WBC) is one of the leading banks in Australia with a market capitalization of ~$89.29 Bn as of April 11, 2019. It is engaged in the business of providing a range of consumer, business and institutional banking and wealth management services. The bank saw robust 1H FY18 performance while 2HFY18 was somewhat soft due to weaker market condition. In the full year, the bank’s balance sheet happens to be in great shape across all dimensions, and its New Zealand as well as business bank delivered strong results. However, its Westpac Institutional Bank business got affected by the lower markets income while BT and Consumer business got impacted by the customer remediation and margins. The bank witnessed challenges in terms of regulatory actions, increased cost of funds as well as full year impact of the bank levy, customer remediation and slowing system credit growth. The bank’s balance sheet remains robust throughout all dimensions of asset quality, capital, and liquidity. The bank made substantial progress on its service-led strategy and digital transformation program. Apart from this, the bank’s mortgage book was fundamentally sound. The bank’s common equity Tier 1 capital ratio stood at 10.6% in FY18 which is above the APRA industry guideline of 10.5%. The bank’s total dividends for 2018 amounted to 188 cents per share which represents a pay-out ratio of 80% of cash earnings which can be considered at decent levels considering the industry-wide challenges. At CMP of $25.570, the stock of the bank is trading at P/E multiple 10.91x of FY20E EPS and P/BV multiple of 1.34x of FY20E BVPS. Keeping the view of decent outlook in the long run backed by good financials, reducing regulatory uncertainty, resetting wealth and insurance business strategy, strong capital & liquidity position, paying regular dividend to its shareholders, maintaining Common equity Tier 1 capital ratio as per Australian Prudential Regulation Authority benchmark, and focusing on simplifying the Group structure & unlocking the value by exiting a high cost & loss-making businesses, we have valued the stock using 1-year forward P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of $19.55; and 5-year average P/E multiple to FY20E consensus EPS of $2.34 and have arrived at the target price upside of lower double-digit growth (in %). Key risks related to rating include regulatory risk, intense competition, and changes in macroeconomic factors such as interest rate, inflation, monetary supply, unemployment, etc.

.png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

Resetting Westpac’s Wealth Strategy: Westpac Group had made an announcement of the changes to the way the bank supports the customers’ wealth and insurance needs. The group’s wealth and insurance businesses would be moving into the expanded business and consumer divisions. The bank stated that private wealth, platforms & investments and superannuation businesses would be moving into the expanded business division while insurance business would be moving into consumer division. The group would be exiting provision of personal financial advice by Westpac Group salaried financial advisers and authorised representatives. The management stated that exiting BTFG’s financial advice business reflects changing external environment. The group is moving towards referral model for financial advice by utilising the panel of advisers or adviser firms and is entering into sale agreement as part of the exit with Viridian Advisory. Also, the group is simplifying the structure and is re-organising the executive responsibilities and would be investing towards the BT brand, demonstrating its strength and market position, although BTFG would no longer be a standalone division. Additionally, the group is unlocking value by exiting the high cost, loss-making businesses.

.png)

Ongoing impacts (from the exit of advice and reducing operating divisions) (Source: Company Reports)

The changes which have been announced are anticipated to be EPS positive in 2020 because of exiting a high cost, loss-making business and the one-off impacts from the transaction and implementation would be spreading over FY 2019 and FY 2020. The initial estimates include one off costs in the range of $250 million-$300 million. The group stated that exiting advice business and moving the wealth businesses into consumer and the business divisions would be resulting in removing cash earnings loss from advice business and $20 million (pre-tax) of the productivity savings from operating one less business division.

Provisions For Customer Payments Update: Westpac Banking Corporation had made an announcement that the cash earnings in 1H FY19 would be reduced by estimated $260 million because of the provisions from further work on the customer remediation programs. The bank stated that, of estimated $260 million impact on the cash earnings, around 90% is related to the issues identified in the previous financial years, approximately half of the provisions is related to financial advice business while the remaining is related to the business and consumer banking and the $260 million also includes the costs which are associated with implementing the remediation programs along with the interest on fees to be refunded.

In FY18, the bank stated that they are working to estimate the potential remediation costs where the customers of authorised representatives gave ongoing service fees, but services were not provided. WBC is focused towards the identification and making refunds to the customers and would commence remediation in 2H FY19 for the customers of authorised representatives still operating under the BT Financial Group’s licences. The bank stated that total fees which were received by the authorised representatives from their customers between 2008 to 2018 amounted to around $966 million. Within this total, the fees received from the customers by authorised representatives which are still operating under BTFG’s licences between 2008 to 2018 amounted to around $437 million.

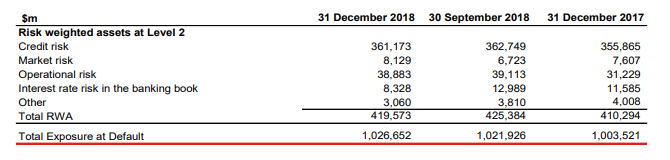

A Look at Critical Metrics of Westpac Banking: The common equity Tier 1 (or CET1) capital ratio of Westpac Banking Corporation stood at 10.4% at 31 December 2018 which is consistent with the normal quarterly trend and broadly in-line with the APRA benchmark. The ratio was lower than the 10.6% reported for September 2018 after payment of Westpac’s final dividend (net of DRP), which reduced the CET1 capital ratio by 69 bps. In the December 2018 quarter, total RWA witnessed the fall of $5.8 billion or 1.4%. The primary components of $1.6 billion reductions in the credit risk RWA include the adoption of AASB 9 (The Australian Accounting Standards Board) accounting standard which reduced the RWA by $3.9 billion and regulatory modelling updates for the corporates which reduced RWA by $1.0 billion. These impacts got partly offset by the portfolio growth which increased the RWA by $2.0 billion and foreign currency translation impacts which increased the RWA by $1.9 billion from the NZ$ appreciation. However, non-credit RWA witnessed a decline of $4.2 billion which was mainly because of $4.7 billion reductions in the interest rate risk in the banking book driven by lower interest rate risk exposure. Also, at December 31, 2018, the bank’s leverage ratio stood at 5.7%. The bank’s liquidity coverage ratio (or LCR), as at December 31, 2018, stood at 128% while, as at September 30, 2018, it was 133%. The average LCR for the quarter ending December 31, 2018 stood at 133%.

Total RWA (Source: Company Reports)

WBC Provided Update for 1Q FY 2019: Westpac Banking had made an announcement that unaudited statutory net profit for the quarter ended December 2018 (or 1Q19) amounted to $1.95 billion while unaudited cash earnings for the same period amounted to $2.04 billion. As per the release, the primary trends within the cash earnings over December 2018 quarter, relative to quarterly average of 2H FY18, includes net interest margins which, excluding Treasury and Markets, were higher following some repricing late in financial year 2018, the contribution from the treasury and markets which was lower because of weaker trading conditions, impairment charge amounting to $204 million, expenses which were lower given the exit of Hastings business and absence of the additional costs related to remediation and $30 million (pre-tax) with respect to insurance claims for the Sydney hailstorms. However, the bank’s asset quality and capital remained strong during Q1FY19. Besides this, the bank is expected to release its 1HFY19 results on 6 May 2019 which will provide further details of its ongoing changes along with some other accounting and divisional changes.

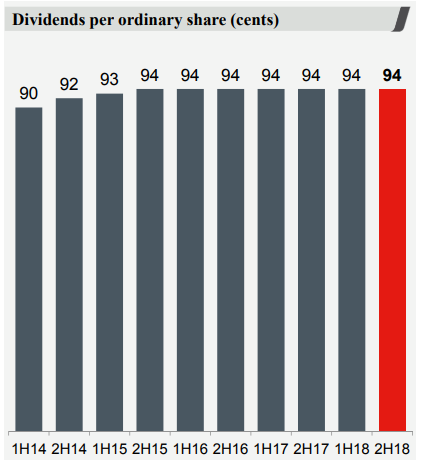

Decent Dividend Pay-outs Further Builds Confidence in Fundamentals: In FY 2018, the bank had declared dividends amounting to 188 cents per share which remains unchanged from FY 2017. The annual dividend yield of the bank is about 6.2% on a five-year average basis (FY14-18). Currently, the annual dividend yield of the bank happens to be at 7.26% which is higher than the industry median of 6.7%. Further, the bank is seeking to maintain a pay-out ratio which is sustainable over the long term. That is, they are aiming to retain sufficient capital for the growth and to maintain unquestionably strong capital position. The dividends for FY 2018 reflect the pay-out ratio of 79.3% which is slightly above the longer-term dividend pay-out ratio of 70% - 75% and the bank managed to achieve this amidst the challenging environment which highlights that WBC is possessing decent fundamentals.

Dividends per Ordinary Share (Cents) (Source: Company Reports)

What To Expect From WBC: Moving forward, Westpac Banking Corporation is expected to be aided by deployments towards the technology. Its plans to make these deployments to improve the service to customers. The bank expects that its service-led strategy would be beneficial for the shareholders. The bank stated that the combination of building great service culture, simplification of the business and utilising the digital technology in order to deliver the innovative services at significantly lower costs would be an increasing differentiator. The priorities for FY 2019 include dealing with outstanding issues, maintaining momentum in the customer franchise as well as structural cost reduction.

The bank is focused on the core markets, including Australia and New Zealand, where they provide a comprehensive range of financial products and services. The bank has been focusing on organic growth, growing customer numbers in the chosen segments as well as building stronger and deeper customer relationships. There are expectations that Westpac’s focus towards maintaining the high level and quality of capital, towards the improvement of funding and liquidity position and towards maintaining a high level of asset quality and appropriate provisioning might support it moving forward.

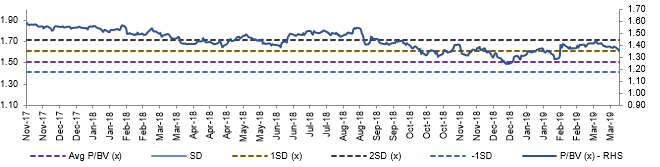

Historical P/BV Band (Source: Company Reports)

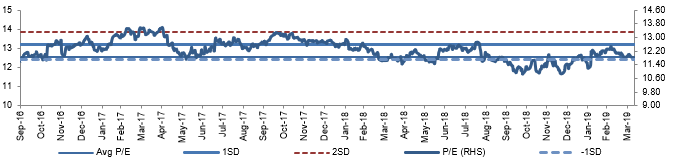

Historical P/E Band (Source: Company Reports)

Stock Recommendation: Westpac Banking Corporation has been maintaining its net interest margin in the range of 2.06%-2.13% from the past five years (i.e. FY 2014-FY 2018) which can be considered within respectable limits and this might attract the interest of the shareholders. Also, the bank’s NIM has improved from 2.09% in FY 2014 to 2.13% in FY 2018 which builds confidence in the bank’s fundamentals. Also, the bank’s efficiency ratio stood at 43.8% in FY 2018 which is lower than the industry median of 51.2% reflecting that WBC has been effectively generating revenues with the help of its assets. At CMP of $25.570, the bank’s annual dividend yield stands at 7.26% which is higher than the industry median of 6.7%. Additionally, decent CET1 ratio coupled with robust fundamentals might act as a long-term growth catalyst. Keeping the view of decent outlook in the long run backed by good financials, reducing regulatory uncertainty, resetting wealth and insurance business strategy, strong capital & liquidity position, paying regular dividend to its shareholders, maintaining Common equity Tier 1 capital ratio as per Australian Prudential Regulation Authority benchmark, and focusing on simplifying the Group structure & unlocking the value by exiting a high cost & loss-making businesses, we have valued the stock using 1-year forward P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of $19.55; and 5-year average P/E multiple to FY20E consensus EPS of $2.34 and have arrived at the target price upside of lower double-digit growth (in %). Given the backdrop of aforesaid parameters, we give a “Buy” recommendation on the stock at the current market price of A$25.570 per share (down 1.274% on 11 April 2019).

.png)

WBC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...