Company Overview - Westpac is Australia’s oldest bank and financial services group, with a significant franchise in Australia and NZ, in consumer small business, corporate and institutional sectors, in addition to a major presence in wealth management. Westpac is among a handful of banks around the globe currently retaining very high credit rating and ranks third in assets across the four major Australian banks. The bank benefits from a large national branch network and significant market share, particularly in home loans and retail deposits. It operates through three divisions: Australian Financial Services, Westpac Institutional Bank and Westpac New Zealand. Australian Financial Services Consists of Westpac’s retail and business banking operations in Australia, St. George Banking Group and BT Financial Group Australia. BTFG is Westpac’s Australian wealth management division. In January 2014, the Company completed the acquisition of Lloyds Banking Group Plc’s Australian asset finance business, Capital Finance Australia Limited, and its Australian corporate loan portfolio, BOS International (Australia) Ltd.

Analysis – Australia’s competition regulator, The Australian Competition and Consumer commission or ACCC has approved Westpac’s acquisition of the A$ 8.4 Billion loan portfolio from Lloyds Banking group Australia. The regulatory green light adds to the bank’s core strengths, providing us with even more confidence in future in future earnings and dividend growth. WBC confirmed that the Lloyds deal had been completed earlier this month. We believe there is upside to the transaction both from a better than expected return On Asset outcome along with helping the cost performance of the bank this year.

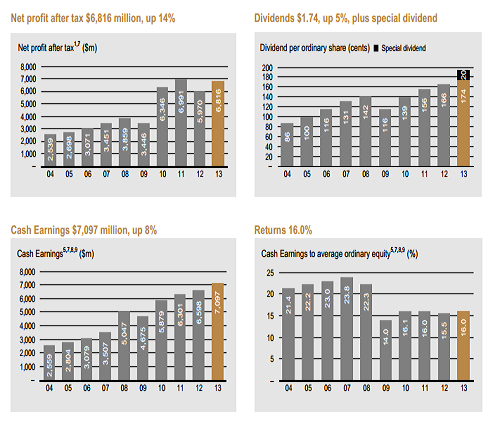

We see solid earnings upside potential, the multi brand, customer centric strategy seeks to deepen and strengthen relationships across 13 Million strong banking and wealth management customer base. A strong balance sheet, peer leading loan quality and impressive returns on equity underpin a strong earnings outlook.

Westpac benefits from the best cost to income ratio and lowest recent loan write off experience of the major banks. We expect additional cost saving initiatives to further improve operational efficiency. Solid operating momentum in core retail and business banking supports moderate earnings growth despite slowing credit growth. Strong profitability and reliance on capital light mortgage growth continue to support organic capital growth. Core tier 1 capital already exceeds Basel 3 minimum requirements and in the medium term surplus capital would be returned via share repurchases or increased dividend payout ratios.

The market remains of the view that it is only a matter of time before WBC needs to cut its standard variable rate to restore mortgage growth. We believe where WBC is underperforming the market is in the broker channel where reputation with brokers, speed of processing and the discount available are the more important factors than the standard variable rate. The recent APRA statistics showed the first signs of success from a comprehensive plan that WBC has in place to improve mortgage growth without damaging the back book margins.

Australia’s banking regulator the Australian Prudential Regulation Authority or APRA has increased the capital conservation buffer that applies to the four major Australian banks by 100 basis points (1%) effective 1

st January 2016. The APRA framework released on 23 December 2013 classifies four major banks as domestically systemically important banks (D-SIB’s) under the tough BASEL 3 rules.

The 1% surcharge to the current 2.5% capital conservation buffer for D-SIB bank takes the buffer to 3.5% in addition to the minimum capital requirement for common equity tier 1 or CET1 ratio of 4.5%. Therefore APRA will require the four D-SIB banks to hold a minimum of 8%.The previous minimum capital requirement was 7%. Westpac’s CET1 ratio of 9.1% is more than any of the other three banks.

|

WBC |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Profitability |

|

|

|

|

|

|

Net Interest Margin |

2.14% |

2.16% |

2.19% |

2.21% |

2.38% |

|

Efficiency Ratio |

42.9% |

44.1% |

43.9% |

43.8% |

43.3% |

|

Operating Leverage |

2.8% |

(0.5%) |

(0.3%) |

(1.2%) |

10.3% |

|

Risk |

|

|

|

|

|

|

Loan Loss Provision (% of Avg. Loans) |

0.16% |

0.24% |

0.20% |

0.31% |

0.83% |

|

Earning Power |

|

|

|

|

|

|

Pretax ROA |

1.4% |

1.3% |

1.3% |

1.3% |

1.2% |

|

Pretax ROE |

21.7% |

20.6% |

21.3% |

22.1% |

23.4% |

WBC’s broad product and service portfolio provides it with a competitive edge over its peers in the industry. It offers a range of business banking, consumer banking, institutional banking, insurance and wealth management services. Westpac’s major products and services include savings account, term deposits, home loans, credit cards, personal loans, business loans, insurance and superannuation plans. The broad product and service portfolio enable the company to cover diversified markets and attract customers.

Strong distribution network helps the company to retain its existing customer base and also enables to attract new clients. The company’s retail and business banking division has a network of 852 branches, 71 business banking centres and 1961 ATM’s in Australia. Westpac’s St. George Banking group serves individuals through a network of 429 branches, 988 ATM’s and various third party distributors.

Westpac is taking various strategic growth initiatives to drive its business performance. For instance Westpac Institutional Bank launched Corporate Evergreen Account, a deposit product which enables corporates and institutions flexibility in managing working capital. Westpac may also benefit from the growing insurance market in Australia. The insurance market in Australia both life and non-life is forecast to grow in the coming years. The insurance market is expected to grow at a compounded annual growth rate of 3.6% till 2016. The Australian non-life insurance market is also expected to grow at an compounded annual growth rate of 4.5% over the same period. Expanding insurance market will enhance the demand for the company’s insurance products in the coming years.

Australian superannuation is an AUD 1.6 trillion growth industry. We believe Westpac is well positioned. Westpac’s integrated business model allows for the expanded product distribution through cross selling by the frontline banking staff. Advanced technology enables banks to better identify and anticipate changing customer needs particularly in the fast growing wealth management sector. Westpac operates market leading investment platforms in BT WRAP and Asgard which include Westpac products such as BT managed funds allowing the company to get revenue at multiple levels at the adviser, platform and the fund manager level.

Good operating momentum from core retail and business banking franchises, sector leading cost to income performance and solid economic conditions underpins consistent profit growth with a lower risk domestic business model. Growing economies of scale, dominant market positions, pricing power, superior balance sheet and high credit ratings provide a strong platform to drive growth. The balance sheet is built around consumer banking and provides the retail orientated bank with earnings diversity to complement the more volatile returns generated from business and wholesale banking activities. Westpac easily exceeds BASEL 3 minimum capital requirements and special dividends were paid in fiscal 2013. We will be putting a BUY on Westpac at current price of $30.87.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...