Company Overview: Westgold Resources Limited is engaged in exploration of minerals. The principal activity of the Company is operating gold mines in Australia. The Company’s projects include Central Murchison Gold Project (CMGP), South Kalgoorlie Operations (SKO), Fortnum Gold Project (FGP), Tuckabianna Project and Rover Project. The CMGP is located in the Murchison Goldfields of Western Australia around the regional towns of Cue and Meekatharra. SKO includes the HBJ underground mine, a number of open pits and the Jubilee Mill. The FGP is located in the western Bryah Basin approximately 150 kilometers northwest of Meekatharra with approximately 1 million tone-per-annum carbon-in-leach (CIL). The Rover Project is a postulated undercover repetition of the prolific Tennant Creek goldfield located 80 kilometers to the north-east.

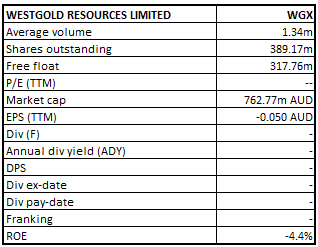

WGX Details

Buldania Lithium Project acquired by Liontown Resources Ltd: Westgold Resources Limited (ASX: WGX) has an engagement in the exploration, development, and operation of gold mines, primarily in Western Australia. The company recently informed the market that Liontown Resources Ltd had inked a formal sale agreement with Westgold Resources Limited to acquire the revenue and production royalties relating to lithium and related minerals over its 100%-owned Buldania Lithium Project in Western Australia. The royalties comprise production royalty of A$2 per tonne of ore mined and/or processed from three key tenements (E63/856, P63/1977 and M63/647) and 1.5% gross revenue royalty and are being acquired for a total consideration of $2 Mn in cash. The location of Buldania is around thirty-kilometre east of Norseman, which is Liontown’s 2nd Western Australia lithium project and is being progressed alongside its flagship Kathleen Valley Lithium Project, where substantial resource spudding program is in progress.

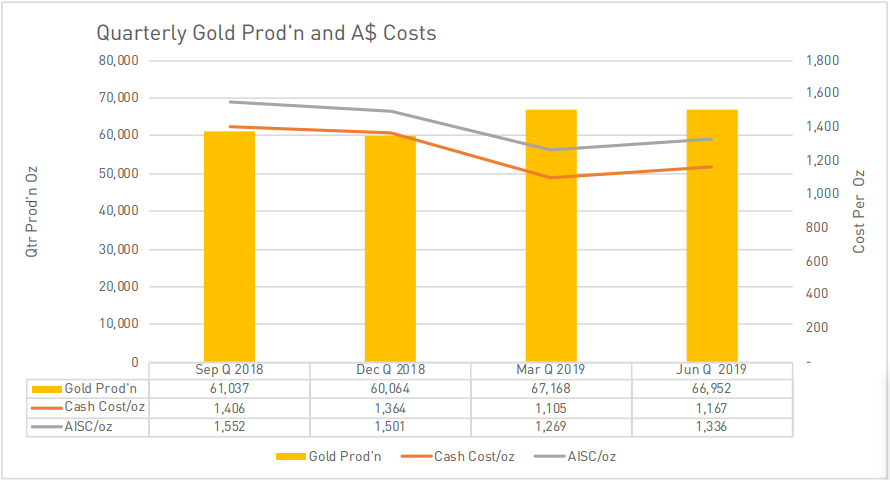

Company’s gold production has increased in the June quarter as compared to the December and September quarter, along with a decrease in C1 cash cost and AISC cost. In the coming times, it is expected that production would increase and AISC cost would decline further, which would help the company in delivering sustaining value to its shareholders. Moreover, present geopolitical tensions are expected to push the gold prices further up in the coming times, helping the gold explorers to improve their margins.

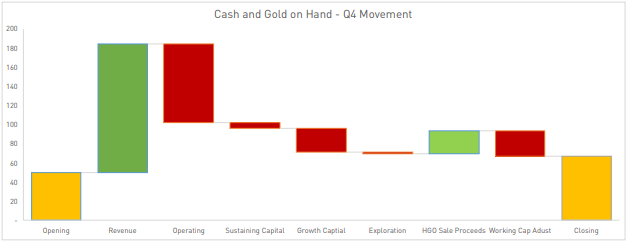

Q4FY19 Cash & Bullion Position (Source: Company Reports)

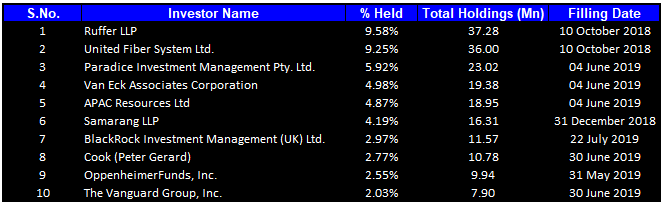

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 49.11% of the total shareholding. Ruffer LLP and United Fiber System Ltd hold maximum interest in the company at 9.58% and 9.25%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

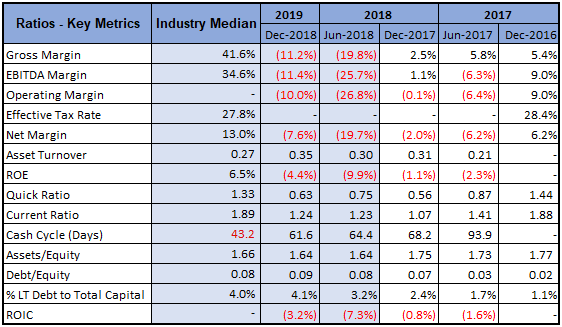

A Quick Look at Key Metrics: Its current ratio for H1FY19 stood at 1.24x, better than the result of 1.07x in the previous corresponding period, which implies that the company is improving its liquidity position to address its short-term obligations. Its debt to equity ratio and Long-term debt to total capital for H1FY19 indicates that company is less leveraged with long term debt, and it utilizes its own funds to fuel its operations.

Key Metrics (Source: Thomson Reuters)

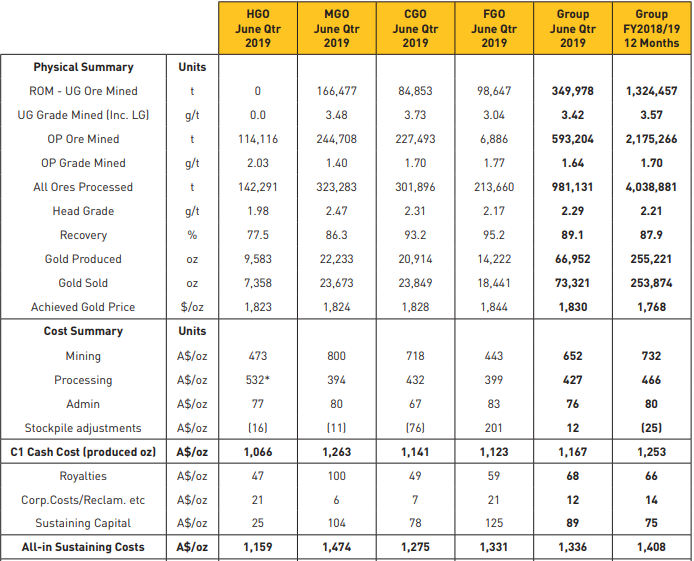

June ’19 Quarter Key Highlights: Westgold Resources Limited’s operates three important processing plants at three Murchison Region which are southern, northern, and central part of a major aggregation play which dominates the Central Murchison goldfields. The company completed its Higginsville Gold Operations (HGO) sale to RNC Minerals and exited from its Eastern Goldfields (Kalgoorlie Region). The gold sales for the June ’19 quarter was reported at 73,321 oz with a cost of $1,830/ounce. The company produced 71,374 oz of gold, of which 4,422 oz was attributable to 3rd party ore processing for the June ’19 quarter. The cash cost (C1) and All-In-Sustaining Cost for the quarterly consolidated gold operation were reported at $1,167 per oz and $1,336 per oz, respectively. WGX’s gold operations reported a mine operating cash flow of $46.3 Mn along with a net mine cash flow of $22.1 Mn for the quarter.

Operating Performance of all Projects (Source: Company Reports)

The Cue Gold Operations continued their ramp-up with production output of 20,914 oz, which was driven by a minor contribution from Big Bell. The Cash Cost (C1) and All-In-Sustaining Cost were reported at A$1,141/oz and A$1,275/ounce, respectively. Around 14,222 oz of Gold was produced at the Fortnum Gold Operations at a Cash Cost (C1) of $1,123 per oz and All-In-Sustaining Cost of $1,329 per oz. The Meekatharra Gold Operations reported gold production of 22,233 oz with All-In-Sustaining Cost and Cash Cost (C1) of A$1,474/oz and A$1,263/oz, respectively.

The overall performance during the June quarter reflected a large turnaround in operating fortunes as it begins to complete its transition to steady state operations. The full year Mine Operating Cashflow generated was reported at $86.9 million of which more than half, i.e., $46.4 million came in the present quarter. The net mine cash flow for the full year was reported as negative of $8.4 million, which reflected the massive investment phase of the Company and the impact of its underperforming (now divested) HGO operations on the group. Again, the current quarter was a dramatic improvement with a positive Net Mine Cash Flow of $22.1 million. At the end of the quarter, WGX reported cash and bullion of $67.3 Mn.

Quarterly Performance (Source: Company Reports)

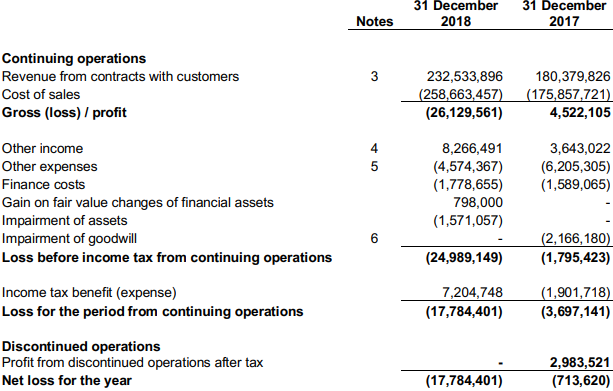

H1FY19 Financial Performance: The revenue from contracts with customers for the half-year period was reported at $232.53 Mn as compared to $180.38 million in the previous corresponding period. The EBITDA for the period was reported at $29.5 million, which can be split into various operations i.e. $14.8 million from Meekatharra Gold Operations, negative of $0.5 million from Cue Gold Operations, $10.1 million from Fortnum Gold Operations, $1.6 million from Higginsville Gold Operations, and $3.5 million from ACM external works.

During the period, capital investment and re-investment in the segments totalled $71 million,where capital investments at Meekatharra Gold Operations, Cue Gold Operations, Fortnum Gold Operations, Higginsville Gold Operations and ACM external works were reported at $24.5 million, $30.8 million, $8.8 million, $5.6 million and $1.3 million, respectively.

In the next half-year periods, the company is poised to improve its bottom line by focusing on its core areas, which are expected to be supported by the recent update where Liontown Resources Ltd has signed a formal sale agreement with Westgold Resources Limited to acquire the revenue and production royalties relating to lithium and related minerals over its 100%-owned Buldania Lithium Project in Western Australia.

1HFY19 P&L Statement (Source: Compnay Reports)

Key Risks: The company is exposed to interest rate risk, credit risk, equity price risk, liquidity risk, and commodity price risk. It usually undertakes ageing analysis and monitoring of receivables to manage credit risk, liquidity risk, through the development of future rolling cash flow forecasts.

What to expect: Westgold Resources Limited continued to upscale its hedge book to be 183,500 ounces at an average price of A$1,828/oz per ounce at the end of the June ’19 quarter. As per the report, deliveries of 10K ounces of gold per month planned over the coming 18.3 months and provides solid margin-locking for the group’s output during the remainder of this capital-intensive phase whilst giving it significant short-term and long-term exposure to higher gold prices.

WGX continued to reduce its gold pre-pay by a further 3,750 ounces during the quarter, essentially repaying about $6.0 million in debt. The gold pre-pay debt has been planned to be reduced by 1,250/oz per month and should be eliminated by the end of the 2019/2020 financial year. The contract mining business of Australian Contract Mining Pty Ltd (ACM) operated steadily keeping pace with the group’s internal growth projects. Internal revenue is consolidated back into the group’s operations. The small external contract at the Frog’s Leg Mine scaled down at the end of the quarter in anticipation of completion in the coming quarter.

At the Murchison Gold Operations, around $256 million of capital investment from FY17-FY19 has been set to lift the operations up for a long and profitable future. Sustaining capex is expected to be around $50 Mn per annum and forward-looking free cash generation at $500 per ounce margin for FY20.

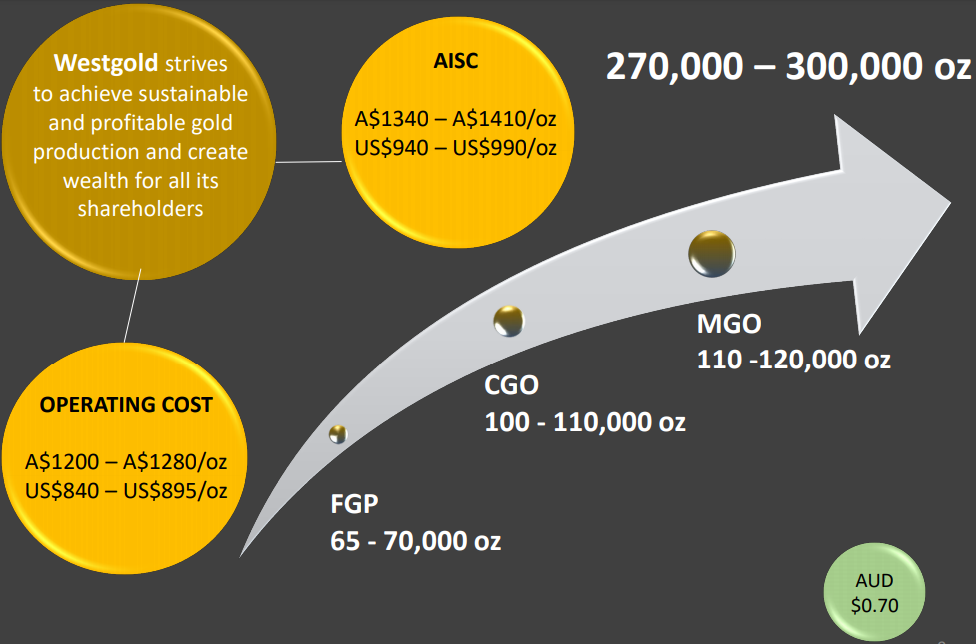

FY20 Guidance: Total production has been estimated at 270,000 – 300,000 oz with All-In-Sustaining cost at A$1340 – A$1410/oz and operating cost at A$1200 – A$1280/oz. Production at projects Fortnum Gold Operations (FGP), Cue Gold Operations (CGO) and Meekatharra Gold Operations (MGO) has been estimated at 65 - 70,000 oz, 100 - 110,000 oz and 110 -120,000 oz, respectively.

FY2020 Guidance Data (Source: Company Reports)

Gold Outlook: Gold Spot (XAU/USD) at the time of writing(July 30, 2019, 4:57 AM (UTC-4 New York)), was trading at US$1425.93, which is ~4.20% above the important support level of US$1366.43. Present geo-political concerns are yet to moderate, and therefore, uncertainty surrounding equity and bond market investments still prevails. Gold investments presently are being looked as a safe-haven investment by the investors and central banks of various countries, which is expected to act as a tailwind for the gold price in the forthcoming time (short to medium term).

Gold Spot (XAU/USD) Chart (Source: Thomson Reuters)

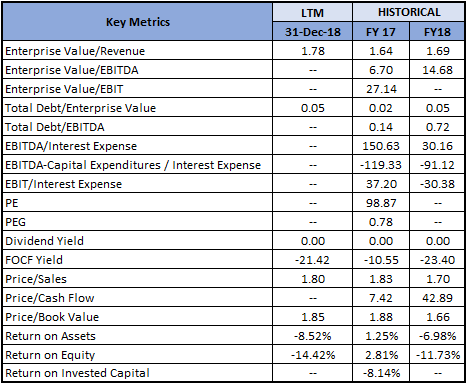

Key Valuation Metrics (Source: Thomson Reuters)

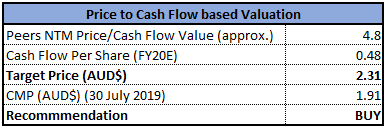

Valuation Methodology 1: Price to Cash Flow Multiple Approach (NTM):

Price to Cash Flow Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

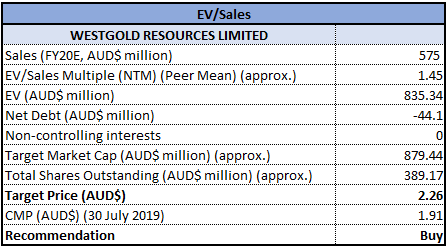

Valuation Methodology 2: EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: WGX stock generated an excellent return of 101.03% in the span of 6 months, while in the span of one-year, it generated a decent return of 25.64%. The company has performed well on its top line and expected to improve its bottom line in the coming years due to its focus on its core operations following the formal sale agreement with Liontown Resources Ltd for Buldania Lithium Project in Western Australia. On the backdrop of decent cash position and ongoing projects, it is expected that the company would be emphasizing over improving its bottom-line performance. Considering the present scenario, decent outlook for gold is expected to help the company to improve its margins further. Looking at the prospects of the company over the long-term, we have valued the stock using two Relative valuation methods, Price/Cash flow and EV/Sales multiple and have arrived at the target price upside of lower double-digit growth (in %). Hence, considering the aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $1.910 per share, down 2.551% on July 30, 2019.

.png)

WGX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...