Company Overview - Western Areas Limited is an Australia-based producer of nickel. It is engaged in mining, processing and sale of nickel sulphide concentrate, the continued assessment of the feasibility and development of nickel mines and the exploration for nickel sulphides, other base metals and platinum group metals. It operates the Forrestania project, which consists of Flying Fox and Spotted Quoll nickel mines and the Cosmic Boy Concentrator, which treats the high grade ore and produces nickel concentrate for sale. Its project portfolio includes Carbon Disclosure Project, Mt Gibb Project (joint venture with Great Western Exploration Limited), Lake King Joint Venture and Musgrave Nickel-Copper Joint Venture. The Company’s subsidiaries include Western Platinum NL, Australian Nickel Investments Pty Ltd, Bioheap Ltd and Western Areas Nickel Pty Ltd.

Analysis - Today’s report brings the latest updates on Western Areas Limited (WSA) with regards to the 1HFY15 profit for period ending 31 December 2014. Primarily, the results entailed sales revenue of A$164.9m as opposed to A$143.4m of previous corresponding period (pcp), i.e., 1HFY14. The EBITDA was reported to be A$74.9m which is an increase from A$65.4m of pcp. The Company reported for NPAT of A$23.6m indicative of an immense surge of about 782% compared to the pcp value of A$2.7m. This growth was driven by increased realised nickel price and continual positive operating cost results based on productivity and efficiency improvements.

Highlights (Source – Company Reports)

The operating cashflow was reported to be of the order of A$52.9m which was a 175% rise over A$19.3m of pcp and is after capital expenditure. Pre-financing cashflow has been reported to be 20% above that of the preceding half which was even characterized by higher nickel prices. This is with respect to the gains attained from cost reduction and good working capital management. The Company also stated that it has a net cash of A$53.7m following debt retirement of A$95.2m. The Company also seems to be performing well to recognize additional savings of the order of A$12m per annum in reduced debt costs from 2 July 2015. The unit cash costs of nickel in concentrate has been reported to be A$2.37/lb as opposed to A$2.41/lb in pcp. Primarily, quotational pricing adjustment of $17m before tax reduced realised nickel prices. WSA’s operating cost initiatives have led to the reported profit outdo the A$22.8m of the prior six-month period to 30 June 2014 (2HFY14) irrespective of the previous period having a higher realised nickel price.

WSA’s declaration of the fully franked interim dividend of 3 cents per share as opposed to 1 cent of 1HFY14 looked better although not very appealing. This interim dividend has led to a payout ratio of about 30%. It is expected that the Company may increase the final dividend from the interim declaration if the nickel price are found to be around the current Australian dollar realised price and the key business aspects remain the same.

Income Statement (Source – Company Reports)

We understand that factors that may impact nickel price include global nickel supply, Chinese nickel pig iron (NPI) production, Indonesian nickel laterite export ban, stainless steel demand and various political factors. The Company believes that the Chinese ore stocks may run out mid?year with ore stocks on the decline. Further, the NPI producer stockpiles seems to be greater than anticipated while ore blending has extended life. Further, the stainless steel demand on balance remains strong in China. Overall, the Company expects nickel price rally late Q2 in CY15 given the market conditions and forecasts.

Nickel Price Movements (Source – Company Reports)

With regards to mine operations, the Company also announced for reserve upgrade for the Flying Fox Mine with added 7,572t nickel grading 6.5%. The high Grade (excluding disseminated sulphide) mineral resource was reported to be 1.72Mt @ 5.2% Ni containing 89,328 Ni Tonnes. The ore reserve was identified to be 1.44Mt @ 4.1% Ni containing 58,533 Ni Tonnes. The Company’s recent exploration highlights at T5 entails 3.3m @ 9.5% nickel and at T6 entails 3.5m @ 5.6% nickel.

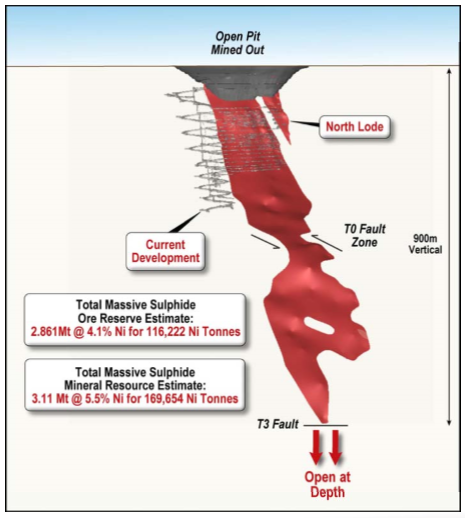

Spotted Quoll Mine (Source – Company Reports)

At Spotted Quoll Mine, the Company reported for the mineral resource to be 3.11Mt @ 5.5% Ni containing 169,654 Ni tonnes and the ore reserve to be 2.86Mt @ 4.1% Ni containing 116,222 Ni tonnes. As per the production, 1HFY15 was found to be characterized with 136,770t @ 4.9% Ni for 6,759t Ni along with efforts with regards to top?down mining using paste fill. Forrestania Nickel Concentrator illustrated the current nameplate capacity of 550,000tpa of ore while achieving throughput 9% above capacity. In fact, concentrate grades of around 14.0% Ni with premium blending product (Fe/Mg ratio >15:1) which seem to be desirable to smelters have been reported. The Company also conveyed about the shipping contract in place with regards to the FOB Esperance Port.

The mill recovery enhancement project is progressing well with the feasibility studies with increase average nickel recoveries reported from 89% up to 93%. The Company has indicated about 6 month construction time and an early indicative capex of around A$20m. This opportunity seems to be a quick payback one with expectation of being potentially operational early FY16.

The updates with regards to New Morning which is 2.5km from Flying Fox and 2.8km from Spotted Quoll, include, material approvals in place, potential major capex savings, commencement of open Pit and shallow underground studies and massive sulphide indicated resource of 321.8kt @ 3.7% nickel. Further, significant intersections were reported to be 4.4m @ 7.4% nickel including 3.6m @ 8.7% nickel, 3.0m @ 6.3% nickel including 2.4m @ 7.6% nickel, and 1.5m @ 5.6% nickel including 0.7m @ 10.2% nickel. The recent shallow hit of 54m @ 1.7% nickel from 38m has also been a highlight. However, a higher nickel price is needed to lower the cut-off grade and expand resource base. WSA reported for two farm-in agreements for Western Gawler Joint Ventures with Gunson Resources Ltd and Monax Mining Ltd with A$0.8m on each to earn 75% over 2 years and further A$0.4m on each for 90% over additional 18 months. The Company expects these to give the first mover advantages targeting massive high grade poly?metallic mineralisation and is eying on the targeted and basement lithology drilling program mid-2015. About the Finnaust mining projects, recent drilling at the Hammaslahti Project reported for 5.6m at 3.2% Cu, 2.7% Zn, 0.7% Pb, 71gpt Ag and 0.76 gpt Au from 196.80m downhole while including 8.65m at 2.2% Cu, 2.0% Zn, 0.5% Pb, 47gpt Ag and 0.50 gpt Au.

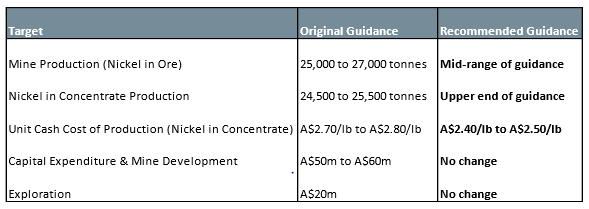

FY15 Guidance (Source – Company Reports)

With regards to the FY15 guidance, the Company has provided a substantial improvement in unit cash cost guidance from the previous range of A$2.70/lb to A$2.80/lb down to A$2.40/lb to A$2.50/lb. Basically and as per the Company, the A$0.30/lb saving equates over the year to an absolute saving in operational costs of A$17m. This saving is further ascribed to absolute cost out program over all main cost drivers (such as mining costs); the mines (primarily Flying Fox) attaining higher nickel grade and nickel tonnes but with less ore tonnes moved; and upgraded recovery from the mill through efficiency gains, improved mill utilisation and lower reagent consumption. Efforts such as those directed towards electricity consumption and commuter flight contracts, have been continually being pursued with regards to the several cost reduction programs. The Company also anticipates to produce to the upper end of guidance for nickel in concentrate reflecting mill throughput of about 10% above nameplate capacity and better nickel recovery. A few aspects to consider include the fact about WSA’s mentioning that the FY15 guidance does not take into account the ongoing cost efforts around contractor rates. Then, mining rates are also expected to surge in 2H FY15 and thus Ni grades are expected to be monitored. At the same time, positive grade reconciliation is anticipated to continue.

WSA Daily Chart (Source - Company Reports)

The increased profitability along with probable increased shareholder dividends appear to be the showstoppers. Overall, the picture with high grade nickel exposure, free cashflow generation, robust capital position looks appealing. Mine life extensions and additional cost cuts and exploration are expected to boost the growth.

Accordingly, we put a BUY recommendation for this stock at the current price of $3.88.

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...