Company Overview - Western Areas Limited, formerly Western Areas NL, is an Australia-based nickel mining company. It is engaged in mining, processing and sale of nickel sulphide concentrate, the continued feasibility and development of the high grade nickel mines and the exploration for nickel sulphides, and platinum group metals. The Company mainly operates in nickel mining and exploration in Australia, and exploration in Finland. The Company’s core asset is Forrestania Nickel Project, which is located 400 kilometers east of Perth. Western Areas has a joint venture with Mustang Minerals to explore the East Bull Lake Project. Its other portfolios include Koolyanobbing, Sandstone, Lake King, Mt Alexander, Southern Cross Goldfields, Mt Jewell, Kawana and East Bull Lake.

Analysis – WSA’s Forrestania Project (which comprises the Flying Fox and Spotted Quoll mines) is a low quartile cash cost nickel operation. As a result despite weak nickel prices over the last few years, WSA has been in a relatively strong position consistently producing positive operating cash flows. WSA also provides a reasonable generous mine life supported by current reserves (Flying Fox 5 years, Spotted Quoll 10 years) with a reasonable likelihood of reserve expansion.

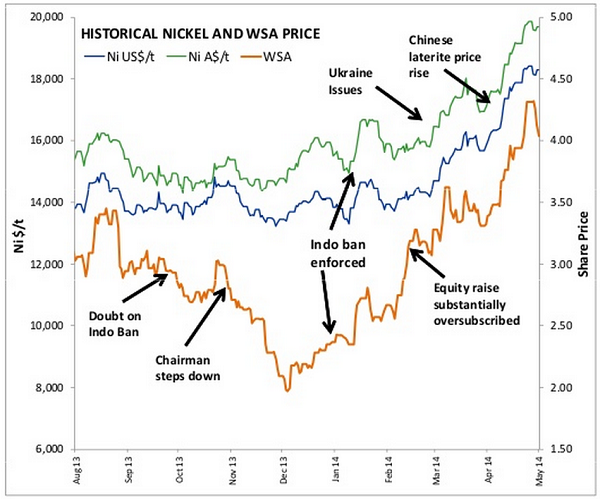

WSA Share Performance (Source - Company Reports)

WSA Share Performance (Source - Company Reports)

WSA is one of the relatively few opportunities to gain significant pure nickel exposure on theASX. The nickel market is looking increasingly tight with impacts already being felt in the upstream markets as a result of the Indonesia ore export ban. This has led to the recent run in nickel prices, the result of speculation in anticipation of future nickel shortfall rather than a result of any current supply shortfall. WSA has a considerable exploration portfolio and with its strong financial position it is well poised to capitalize. The most exciting prospect appears to be the New Morning prospect. At depth they have made significant intersections of massive nickel sulphide. This zone is located between the spotted Quoll and Flying Fox mines and so if an economic deposit is discovered then WSA would use this as a new mine after the exhaustion of Flying Fox (or sooner as the third mine in operation). Further drilling is underway to determine the extent of mineralization.

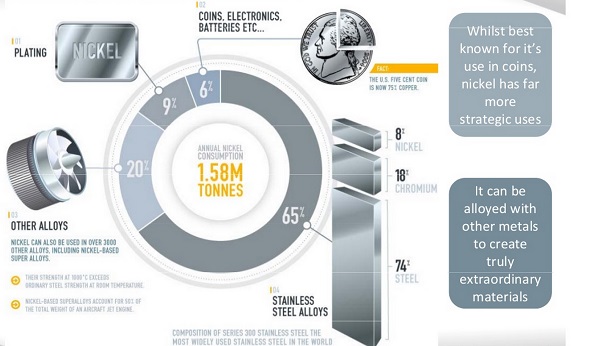

Uses of nickel (Source - Company Reports)

Uses of nickel (Source - Company Reports)

The two key properties of nickel are: 1) It is highly resistant to corrosion and rusting – so is an ideal ingredient in the manufacture of stainless steel and 2) It is harder than iron. In addition nickel is also a good conductor of heat and electricity can be easily magnetized, is ductile and malleable. Nickel is largely used as an alloy with other metals. Around three quarters of total use of nickel is in the form of stainless steel. Around 50% of nickel is processed into pure nickel while a quarter of nickel is transformed into Nickel Pig Iron (NPI). NPI is used as alternative to the pure nickel in the production of the stainless steel as NPI is cheaper than pure nickel and this is why a method for producing NPI was developed. NPI consists of low grade nickel ore, coking coal, sand and gravel.

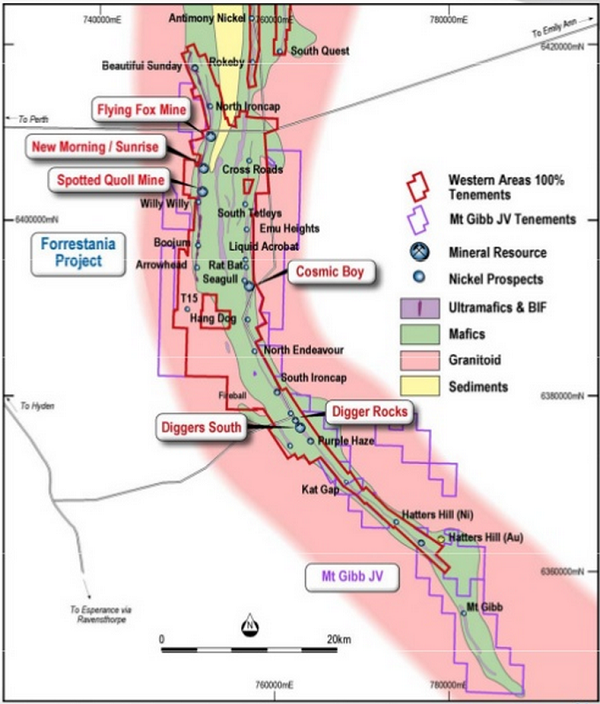

Forrestania Tenements (Source - Company Reports)

Indonesia has put in place a ban on the export of certain raw materials/unprocessed mineral ore. This especially applies to nickel and bauxite exports among others. This ban became effective on 12th January 2014. The requirement for onshore processing was first suggested in the new mining law of 2009. The rationale was that Indonesia needs to move from being an exporter of raw commodities, downstream towards generating higher value products. To date the impacts of the Indonesian ban have been in the upstream market. The volume of ore imports into China from Indonesia have fallen dramatically.

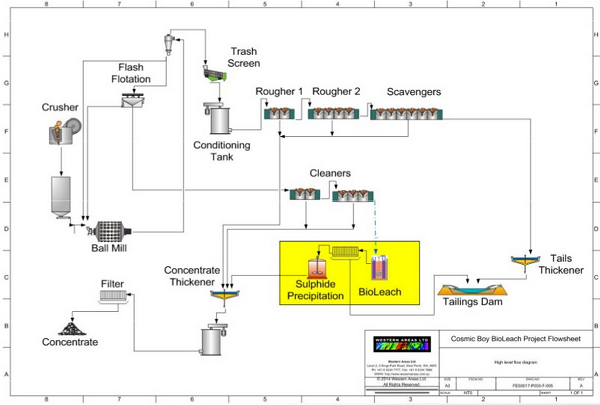

Mill Recovery Enhancement (Source - company Reports)

WSA’s June quarter production result was strong with nickel ore mined of 6.3kt beating our forecasts by 9%. The stronger result was attributable to higher average grades at both Flying Fox and Spotted Quoll. Ore at Flying Fox was primarily sourced from longhole open stopes on two levels with modest tonnes from Jumbo development and air leg mining. Decline development at Flying Fox remained on hold for the quarter, however with improving nickel prices we would expect decline development to resume. At Spotted Quoll one major stope was completed and another started in June. The top down longhole benching and paste fill mining method is now well established.

Offtake Contracts (Source - Company Reports)

Offtake Contracts (Source - Company Reports)

Nickel concentrate production for the June quarter of 6.3kt was marginally ahead of our expectations due to slightly higher mill throughput. Nickel concentrate sales were broadly in line with production. C1 cash costs of A$2.61/lb were slightly better than forecast while net cash of $10m at the end of the June was broadly in line with our expectations after accounting for mark to market adjustments for nickel prices and the A$/US$. Improving nickel prices has enabled WSA to generate sufficient cash flow to move to net cash for the first time since the development of the Flying Fox mine commenced. We note that the significant reduction in net debt was aided by a $100m equity raising and share purchase plan completed in February 2014.

WSA Daily Chart (Source - Thomson Reuters)

WSA Daily Chart (Source - Thomson Reuters)

We expect improving nickel prices will see WSA start to build on its net cash position in 2015. Our estimates suggest that WSA will generate its market capitalization in cash flow within four years, suggesting that a significant increase in dividends could occur from FY15. Our estimates indicate that WSA would generate two times its current market capitalization in cash flow over the life of the Flying Fox and Spotted Quoll mines.

WSA currently sells all of its nickel concentrate production from Forrestania tor BHP Billiton and Jinchuan via two separate offtake agreements. The BHP Billiton offtake is for 12ktpa of nickel in concentrate that expires in mid-2017. The Jinchiuan offtake is for 26kt of nickel in concentrate over a two year period, which is expected to be completed in December 2014. The company has indicated it is currently considering the re tender process for Jinchuan offtake agreement. Given the tightening Nickel market and BHP Billiton’s need for a replacement offtake for its Perseverance mine we expect the tender process to be hotly contested.

WSA has delivered a strong June Quarter production result. Improving Nickel prices has seen free cash flow generation rise to $40m for the quarter, the strongest result since 2011. Significantly the company has moved into a net cash position for the first time since 2004, raising the potential for increased dividends in FY15. We put a BUY recommendation on the stock at the current price of $4.81.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...