Kalkine has a fully transformed New Avatar.

Company Overview: Wesfarmers Limited is one of Australia’s leading retail groups with principal activities revolving around retailing of home improvement and outdoor living products and supply of building materials; retailing of office and technology products; gas processing and distribution; and manufacturing of chemicals and fertilisers. The company owns an industrials division with businesses in chemicals, energy and fertilisers, and industrial as well as safety products. The headquarter of Wesfarmers is located in Western Australia.

.PNG)

Wesfarmers’ Businesses Continues to Deliver Strong Performances: Wesfarmers Limited (ASX: WES) is a diversified industrial company which is involved in the retailing of home improvement and office supplies, general merchandise and specialty departments stores, gas processing and distribution, chemicals and fertilisers, etc. As at 19th March 2020, the company had a market capitalisation of ~$43.04 billion. For the half-year ended 31 December 2019, Wesfarmers reported a net profit after tax (NPAT) of $1,142 million (pre AASB 16), up 5.7% on previous corresponding period (pcp), as a result of strong performance of the Group’s largest businesses, Bunnings and Kmart, and ongoing solid performance in WesCEF. Over the period, revenue for Bunnings increased by 5.3% to $7,276 million while revenue from Kmart Group increased by 7.6% to $4,990 million. Officeworks’ revenue increased by 11.9% to $1,231 million while its business continues to witness strong revenue growth in both stores and online as a result of continued investment in the customer experience.

In the long run, the company has favorable outlook on the back of enhancing e-commerce offer and digital capabilities, diversified business model, and synergistic acquisition with Kidman Resources Limited and Catch Group Limited. Hence, considering the group’s strong balance sheet, decent fundamentals, robust credit metrics and cash flow generation, decent dividend history, we have valued the stock using a relative valuation method, i.e., price to earnings multiple and arrived at a target price of lower double-digit upside (in % terms)..png)

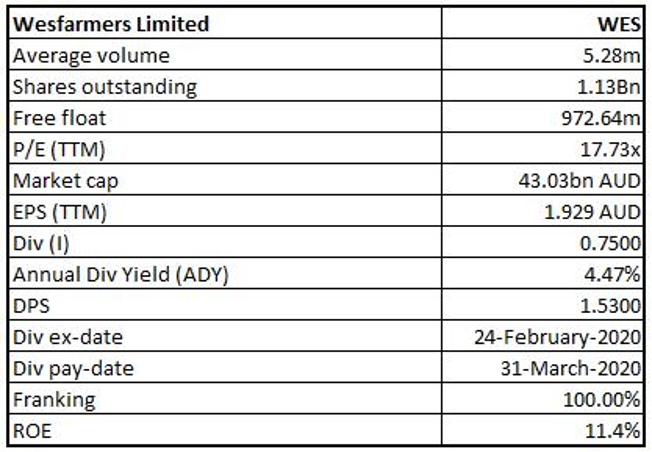

Key Financial Highlights (Source: Company Reports, Thomson Reuters), *Includes Special Dividends

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Wesfarmers Limited:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Overview of Key Margins: In H1FY20, the company’s EBITDA margin stands at 15.2%, up 3% on pcp, demonstrating group’s improved profitability over the period. The company’s operating margin has also improved to 11.4%, up from 9.8% on previous half. The company’s RoE rose during the period to 11.4%, up 5.1% on pcp. Therefore, it can be said that WES has been focusing towards delivering returns to its shareholders..png)

Key Metrics (Source: Thomson Reuters)

Changes to Leadership Structure: On 19th March 2020, Wesfarmers Limited announced changes to the leadership structure of its industrial businesses, as per which, David Baxby is going to step down as Managing Director of Wesfarmers’ Industrials division and Tim Bult, the current Director of Associate Businesses and Corporate Projects, will take the position of Managing Director of Wesfarmers Industrial & Safety to continue to support each of the CEOs of the respective businesses. The changes in the leadership structure reflects the respective scale and opportunities of Wesfarmers Chemicals Energy and Fertilisers (WesCEF) and the Industrial & Safety businesses.

Sale of 4.9% of Coles Group: During the last financial year, the demerger of Coles was a major accomplishment for the group as Coles (as a separate entity) is expected to deliver greater shareholder value than the value attributed by the market to the combined Group, owing to different growth outlooks. Wesfarmers recently sold 4.9% of the issued capital of Coles Group Limited (ASX: COL) for total pre-tax proceeds of $1,050 million, reducing its current interest in Coles to 10.1%. Wesfarmers still has the right to nominate a director to the Coles Board. This divestment is expected to recognise a pre-tax profit on sale of approximately $160 million, demonstrating Wesfarmers continued confidence in Coles’ future as a stand-alone listed company.

Enhancing Value Through Acquisitions: In H1FY20, the company completed the acquisition of Kidman Resources Limited and Catch Group Holdings Limited, both of which are going to benefit from the Group’s existing capabilities and will support shareholder returns over the long term. The acquisition of Kidman, which owns 50 per cent of a major lithium deposit and project in Western Australia, will allow the group to leverage its deep expertise in chemical processing into the growing market for high quality lithium hydroxide.

Focused on Dividends and Capital management: During the period, with the help of strict working capital management and disciplined capital expenditure, the group was able to generate strong cash flow across operating divisions and was able to retain a strong balance sheet with net financial debt of $2,317 million at the end of the period. As a result of decent earnings from continuing operations and its dividend policy, Board has decided to pay interim dividend of $0.75 per share in 1H FY 2020. While deciding for the dividends, the Board has taken into the consideration, the group’s strong balance sheet, robust credit metrics, cash flow generation, and available franking credits. The dividends will be payable on 31st March 2020. The group has a decent track record of paying dividends to its stakeholders. In the second half of FY19, it had declared a fully-franked final dividend of 78 cents per share, bringing the full-year ordinary dividend to $1.78 per share. The group had paid a special dividend in April 2019 of $1.00 per share, including which, the total fully franked dividends for the year were $2.78 per share..png)

Dividend History (Source: Company Reports)

What to Expect: The group’s portfolio of cash-generative businesses with leading market positions is well-placed to deliver satisfactory shareholder returns over the long term and its retail divisions intends to make investments in the offers to deliver greater value, quality and convenience. The digital offer in the company’s businesses including Bunnings, Kmart Group and Officeworks will be enhanced further to meet the changing needs of customers while expanding addressable markets and improving operating efficiencies. As per the 1HFY20 report, the group has not experienced any material impact on its businesses from Coronavirus outbreak, and the situation is being monitored closely. In order to create value for shareholders over the long term, the group will continue to develop and enhance its portfolio of businesses and will leverage its unique capabilities and platforms to take advantage of growth opportunities within existing businesses.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Earnings Based Relative Valuation.png)

Price to Earnings Based Relative Valuation (Source: Thomson Reuters)

Stock Recommendation: The Board considers the Group to be well positioned for future growth in its existing businesses, with the balance sheet capacity to expand its operations and move into new fields where the potential returns justify investment. The stock is trading towards the lower band of its 52-week trading range of $31.73 to $47.415. The stock has fallen ~24.42 per cent in the past one month as at March 18, 2020 and is trading at a reasonable P/E level of 17.73x with annual dividend yield of 4.47%. On the face of decent fundamentals and no material impact from COVID-19 as indicated by the company on February 19, 2020, we presume that the recent price correction can be considered an opportunity to invest in the stock. Considering the aforesaid parameters, long-term growth opportunity, decent dividend history, and current trading levels amid a cautious view on Coronavirus outbreak, we have valued the stock using price to earnings multiple based relative valuation and have arrived at a target price of lower double-digit upside (in percentage terms). Thus, we give a “Buy” rating on the stock at a current market price of $34.890, up 2.018% on 19 March 2020.

WES Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...