Company Overview - WDS Limited is engaged in the provision of specialist services to the underground coal mining industry and to the infrastructure, oil, gas and water pipeline construction and maintenance sectors in Australia. The Company operates in two segments: Mining and Energy and Infrastructure. Mining segment is engaged in the provision of skilled labour and specialist mining equipment to the underground mining industry. Energy and Infrastructure segment is engaged in the provision of specialist design, construction and maintenance services to the oil, gas and water sectors. WDS is a specialist EPC provider of engineering, fabrication and installation services across the energy sector. WDS is particularly well placed to provide pipeline and other infrastructure services to the growing Coal Seam Gas (CSG) industry in Queensland and currently provides infield services under term contracts to GLNG, QCLNG, APLNG and Arrow.

Analysis – WDS is in the right space (Coal Seam Gas). We believe that CSG field development offers strong long term potential and WDS generates 85% of EBITDA from its energy business, the bulk of which is exposed to all the CSG proponents in Australia. WDS doubled net profit after tax to $7.4m for the six months ended 31 December 2013, a result almost entirely driven by the strength of its Energy Division. Their backlog of work grew by 35% in 1H14 vs FY13 to $376m, winning the $143m Eagle Downs project was key to giving the mining division visibility. WDS has most of the ingredients that we like in a good contractor: management, track record, conservatism, balance sheet, backlog and manageable commercial risk profiles.

APLNG Stores - Reedy Creek (Source - Company Reports)

APLNG Stores - Reedy Creek (Source - Company Reports)

WDS is a quality, niche exposure to the CSG developments in Queensland and would be geared to any recovery in on-mine production development expenditure in the coal sector. Besides FY10 in which the group reported its first loss, it has had a good track RECORD. The issues in FY10 were substantially caused by delays in CSG field development, flooding and then a resultant restructuring in the group and a sharpened focus on risk management. Better risk management together with more buoyant market conditions aided the performance of the energy business in particular which is currently carrying the group through ebb in its mining business. The recent winning of a $143m job at Eagle Downs should stimulate some recovery in the mining business in the next two years. The movements in the group’s order book are quite indicative of the volatility experienced in the mining space. Given the group’s exposure in production driven expenditure one would expect a recovery in this order book in time.

Eagle Downs Project (Source - Company Reports)

Eagle Downs Project (Source - Company Reports)

We also think that the commercial risks are pretty well managed. As an example the group’s recent win at Eagle Downs is on a schedule of rates basis, having avoided the obvious pitfalls of lumpsum, turnkey work. While a schedule of rates based contract still has risk associated with it, the group’s experience in doing this type of work is an important mitigant. In general commercial risk management at WDS seems to be in good shape.

Austar Project (Source - Company Reports)

Austar Project (Source - Company Reports)

The Energy Division recorded a 19% increase in revenue to $144.2m, on the previous corresponding period, and almost tripled its earnings before interest and tax to $15.2m. This was due to significant scope extensions and expansion of the client base across the major CSG/LNG proponents. WDS has signed a master service agreement for field development and operations construction with Arrow energy. The anticipated value of contract is $40 - $80 Million and shared 50:50 with JV partner China Petroleum Engineering & Construction Corp over FY15 and FY16 with a 1 year option to extend. The JV will fabricate and install wellheads, gas distribution and water gathering lines, undertake power works and civil construction/maintenance work. Contract win with Arrow further deepens WDS spread of work amongst the four major CSG proponents in QLD.

Coal services remain tough with little improvement expected for the remainder of FY14. Contraction in coal sector is expected to stabilise around current levels for the remainder of this financial year. While it is still difficult to gauge when the next phase of this cycle will commence, WDS remains confident about the medium term growth profile for the coal industry with production forecasts predicted to increase. Eagle down contract will improve margins and equipment utilisation however this is not expected to impact the division’s result significantly until FY15. Despite the state of market, Mining is experiencing significant tendering activity and increased enquiry levels; Previous cyclical events have resulted in an increased contractor demand as mines return to full production, due to cost and efficiency.

Energy and infrastructure represents around 60% of the total order book. CSG is the primary commodity exposure as WDS primarily undertakes gas gathering, mechanical and electrical instrumentation services. Staff numbers including contractors and sub-contractors increased by 30% to about 805 people during the first half vs 616 at June 2013. Sales are up 20% in the first half compared with the previous corresponding period. There is strong margin improvement up 5.4 points driven by APLNG work and a 12 month contract on GLNG appraisal works. Strong pipeline of tenders already submitted and we expect activity in the gas gathering area to remain plentiful. Works with CSG/LNG proponents continued to provide strong growth including an extension of the Santos GLNG contract and the APLNG project moving into full production. WDS delivered a stellar 1H14 result driven by margin improvement in upstream coal seam gas services. We believe FY14 NPAT guidance of $12-14 Million is achievable given the strong 1H14 performance.

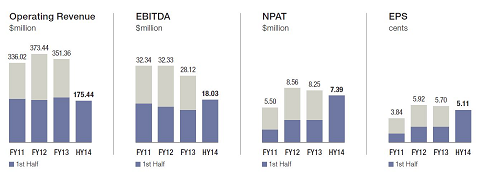

Financial highlights (Source - Company Reports)

Financial highlights (Source - Company Reports)

WDS Daily Chart (Source - Thomson Reuters)

WDS Daily Chart (Source - Thomson Reuters)

WDS provides engineering services to the energy, infrastructure and underground coal mining sectors. WDS is one of the few small cap stocks with exposure to upstream coal seam gas activity in QLD with a solid net cash balance sheet and pays quarterly fully franked dividends. We estimate WDS has an order book of around $400m split 60% CSG work and 40% coal mining work. We also see potential valuation upside for WDS coal mining business which although facing weak demand at present has represented the bulk of group’s order book historically. When coal markets eventually turn WDS should be a beneficiary of increased demand for its underground coal mining services. We like the WDS story and would be putting a BUY at the current price of $1.09.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...