Company Overview: Volpara Health Technologies Limited (ASX: VHT) is a SaaS-based company, offering breast imaging analytics services and products. The company offers high-quality and personalised breast cancer screening software applications. The AI imaging technologies of VHT aid in the premature detection of breast cancer. Volpara Health Technologies was formed in 2009 and aims at lowering the death and cost of breast cancer via Volpara software. Volpara Enterprise software is supported by the company’s suite of market-leading clinical products i.e. VolparaDensity, VolparaDose, VolparaPressure, VolparaPositioning and VolparaServer.

.png)

VHT Details

.PNG)

VHT Rides on Higher Investments & Acquisition Synergies: Volpara Health Technologies Limited (ASX: VHT) is a New Zealand based health sector company, which is engaged in providing health solutions relating to breast cancer. The company builds digital health solutions to facilitate personalised breast cancer screening software applications. The AI imaging knowhows accessible with VHT, helps to improve clinical decision-making process and identifies early detection of breast cancer. The company is involved in research, development, and manufacturing of breast imaging analytics and analysis products. It is worth mentioning that VHT has >164 staff throughout Australia, New Zealand, France, the US, and UK. The company’s revenues went up a whopping 197% year over year and came in at NZ$6.8 million, in the first half ended 30 September 2019. Annual Recurring Revenue (ARR) for the period came in at NZ$15.7M as compared to NZ$4.8M in the prior corresponding year.

In a recent announcement, the company stated that despite global economic turbulence, it remains on track with decent fourth-quarter results. Pursuant to the conclusion of one or two major deals, the company is on track to meet the ARR outlook that it provided at the end of third quarter, to be approximately NZ$17.8 million. The company’s fourth quarter sales to date are benefitting from a favourable mix of traditional Volpara products, which the company acquired last year from MRS Systems, Inc. (MRS).

The company had entered into an agreement to buy US-based MRS Systems for a consideration of NZ$23 million. With MRS acquisition, the company will be able to develop its product portfolio and enhance its artificial intelligence and machine learning imaging algorithms. This, in turn, will aid VHT to provide high-quality breast care treatment via new technology development. The company made significant investments in R&D with the launch of a major new product suite at the RSNA trade show in Chicago in December.

The company also received a nod from the US Food and Drug Administration for the Transpara software, in order to process 3D breast images. VHT remained on track to develop a solid pipeline of leads and interest in Transpara for the last nine months, and the successful sale of its 3D software will be a tailwind, going forward. Furthermore, VHT’s large sales team will now be selling MRS’s products on a SaaS model, allowing for improved Average Revenue Per Unit (ARPU) at new and existing customer sites.

Notably, VHT continues to lessen the mortality rate and cost of breast cancer by providing clinically proven software that bolsters high-quality and personalized breast cancer screening. The company is also investing in business capabilities with the addition of 3 new officials to its executive team in Operations, People and Customer Success. The move is expected to help drive the next wave of growth and improvement for the company. Also, the company remains on track to grow the engineering team to accelerate the core functionality of VolparaDensity and VolparaEnterprise.

The company witnessed a CAGR of 82.9% in revenue in the time period of HY17-HY20. VHT has been investing in new technology and service enhancement, with enhanced focus on clinical software, quality management and personalized care systems. Subscription revenues increased from NZ$110K in HY17 to NZ$5.19 million in HY20.

.png)

.png)

.png)

.png)

Revenue, ARR, Subscription & Market History (Source: Company Reports)

1HFY20 Performance: Revenues for the period came in at ~NZ$6.8 million, up 197% year over year. The increase was primarily aided by higher subscription revenue, which soared 148% year over year. Capital revenue in 1HFY20 went up 680% and came in at NZ$1.7M. During the period, percentage of women having a Group product applied to their images and data stood at~25.8%, an increase from 5.6% reported in the year-ago period. Notably, team expansion and scaled up operations, led to an operating loss of NZ$8.4 million in 1HFY20. Loss after tax was up 55% year over year. The figure consisted of one-off acquisition costs of ~NZ$620k and other material non-cash expenses. Diluted loss per share for the period came in at NZ 4 cents per share, as compared to a loss of NZ 3 cents per share in pcp. Operating expenses for the period increased to NZ$15.4 million from NZ$5.4 million in 1HFY17, due to higher investment in the business for growing the sales, marketing and customer success teams’ capability. Moreover, adding resources into engineering for R&D and strengthening the executive team with new roles in operations, people and customer success also led to an increase in operating expenditure.

.png)

Key Highlights (Source: Company Reports)

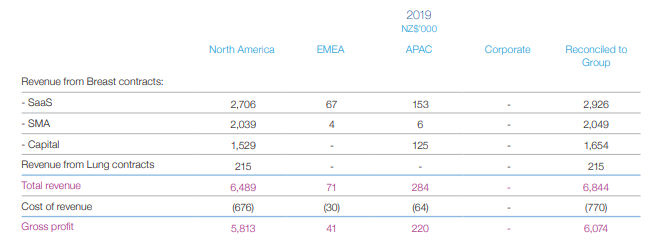

Geographical Performance: During the period, total revenues with respect to North America, EMEA, and APAC stood at NZ$6.5 million, NZ$71k and NZ$284K, respectively. This compared favourably with the year ago figures of NZ$1.98 million, NZ$147K and NZ$183K, respectively. Majority of the company’s revenue is derived from the sale of clinical functions and patient tracking software.

Geographical Metrics (Source: Company Reports)

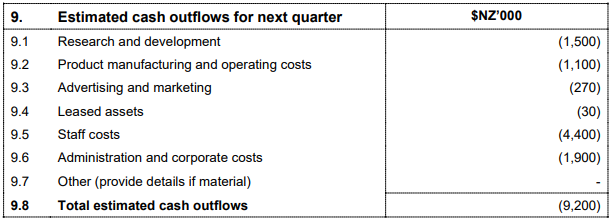

Balance Sheet & Cash Flow Details: Cash on hand at the end of the 3QFY20 came in at NZ$35.4M, down from NZ$40.2M at the end of the prior quarter. Operating cash outflow stood at NZ$4.5M as compared to a cash outflow NZ$4.2M in the prior quarter. The Group continues to hold no debt. The company is expecting NZ$9.2 million cash outflow in the coming quarter. For Q3FY20, the company’s cash receipts stood at NZ$4.5M, soaring 138% on pcp.

Estimated Cash Flow Details (Source: Company Reports)

COVID-19 Impact: We note that the novel coronavirus has been shaking most of the companies and disrupting global economic activities. In such a scenario, VHT opines that lung computed tomography will be used to screen patients to comprehend the extent of COVID-19. Hence, with MRS acquisition, VHT has entered the lung cancer screening business, and presently has ~8% of the US market. The company also updated the market with the next release of Aspen Lung, which will deal with lung nodules found by imaging the lung for other reasons, one of them being COVID-19. Given the current outbreak, this work is expected to be released in mid-2020.

Recent Updates:

1. On 13 March 2020, the company announced that Harbour Asset Management Limited and its related bodies corporate, a substantial holder of the company, has increased its voting power from 6.465% to 7.960%.

2. On 3 March 2020, the company issued 340,000 new fully paid ordinary shares under the Company’s Employee Share Option Plan (ESOP).

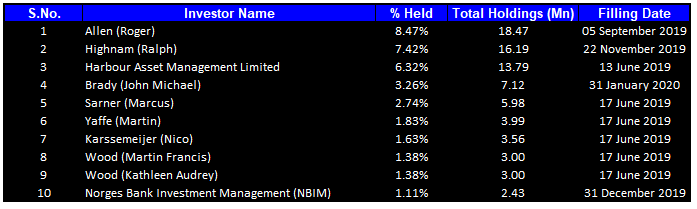

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 35.55% of the total shareholding. Allen (Roger) has the maximum shares in the company at 8.47%. Highnam (Ralph) is the second-largest shareholder, with a holding of 7.42%.

Top Ten Shareholders (Source: Thomson Reuters)

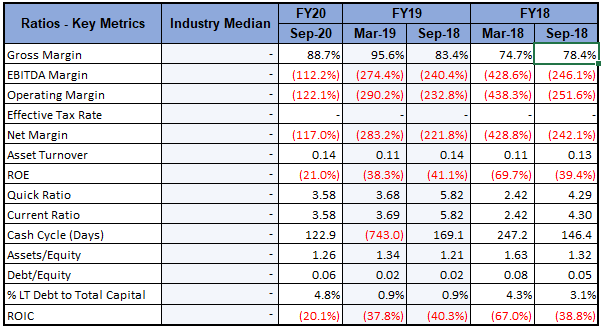

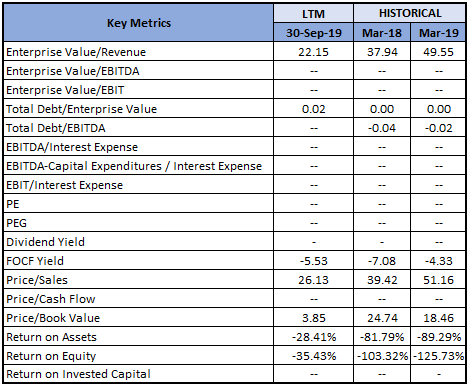

Key Metrics: In 1HFY20, the company had a gross margin of 88.7%, which is higher than 1HFY19 figure of 83.4% and 1HFY18 figure of 78.4%, representing decent fundamentals.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company expects to increase its US sales team along with its APAC & European team with a full suite of products. Further, the company’s product suite has expanded over the last few years, allowing for increased ARPU from new and existing customers. The momentum is expected to continue, going forward. The company is also working towards restraining costs and optimizing work, with the integration of MRS Systems. The company’s efforts for R&D and product improvement will continue to innovate its product suite with the expanded engineering and science teams. Further, the company’s strategy to expand its product portfolio and improve its AI imaging algorithms through the latest technology advancement can additionally improve and enhance patient outcomes on a global basis.

Key Valuation Metrics (Source: Thomson Reuters)

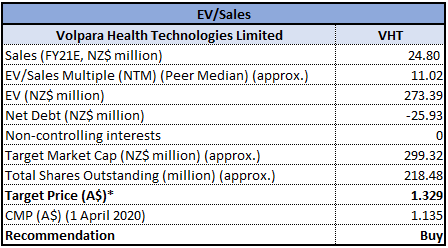

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach

EV/Sales Multiple Based Relative Valuation (Source: Thomson Reuters), *1 NZD = ~0.97 AUD as of 01-04-2020

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week trading range of A$0.79 - A$2.170. The stock has a market cap of ~A$233.77 million. In 1HFY20, the company delivered a decent result, driven by increased investment in new technology as well as improvements in quality and personalised care systems. From the analysis standpoint, the company has recorded revenue CAGR of 82.9% over the last four first halves (1HFY17 – 1HFY20). Considering the above factors, we have valued the stock using EV/Sales multiple based relative valuation approach, and for that purpose, we have considered Pro Medicus Ltd (ASX: PME), Nanosonics Ltd (ASX: NAN) and Telix Pharmaceuticals Ltd (ASX: TLX), as peer group. As a result, we have arrived at a target price of lower double-digit growth (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of A$1.135, up ~6.075% on 1 April 2020.

.png)

VHT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...